Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

What are Blockchain digital assets ?

Blockchain digital assets are a type of digital asset or cryptocurrency, and sometimes represent stakes in a particular project or company. Others are intended solely as currencies, Bitcoin for example, and do not represent a stake in a particular organization. However, unlike traditional assets, blockchain assets are digital, owned solely by you, and are immediately transferable, at any time, to any person.

In order to understand the value proposition of blockchain, it’s important to understand how the internet has evolved from the perspective of the consumer.

At first, the internet was a giant source of information.

Aptly dubbed the “information superhighway,” instead of driving to a library, picking up a newspaper, or flying to a museum, people could just “go online” and read about it.

With more information at their fingertips, more people got involved. Individuals started adding opinion pieces like blogs and social media to the mix, thereby expanding and adding more and more information to the network.

The next iteration of the internet was applying “not having to go to a library” to not having to visit a store—leading to the birth of the e-commerce site.

Instead of driving to the supermarket or clothing store, consumers could order items from the comfort of their own home (and later smartphone/IoT devices).

Although transactions through e-commerce or financial platforms are done online, in terms or services bought, sold, or transferred are digital representations of something physical.

A person could go to his or her bank, withdraw $50K in cash, and drop it off at the car dealer for their car- or could send a wire transfer through his or her online banking portal. The same goes for stocks, groceries, movies/TV shows, or anything else purchased online.

In 1999, economist Milton Friedman posited a new idea with regard to the evolution of the internet.

Freidman spoke about how the growth of the internet would allow for more deregulation and less government oversight, but there was still one thing missing.

“The one thing that’s missing, but will soon be developed, is a reliable e-cash, a method whereby on the Internet you can transfer funds from A to B, without A knowing B or B knowing A.”[1]

In other words, Friedman suggested the next phase of the internet would evolve from a digital representation of something physical, to a digital store of value that exists exclusively on the internet, like an eCoin.

Roadblocks: Trust and Scarcity

Though Friedman suggested the creation of an eCoin in 1999, there still roadblocks that had to be navigated before a viable digital currency could be released.

When creating a store of value, there are two main challenges. In normal transactions, a central party (bank, credit card, etc.) serves as the guarantor for the transaction.

This is known as a centralized network and can be seen in the image below.

But the internet isn’t a central system, rather it’s decentralized.

There isn’t a single overseer of the internet, it’s instead a collection of server hubs storing and exchanging data. In a decentralized system, there is no central party, so the issue of trust needs to be resolved.

Figure 1: Graphic Representation of Networks[2]

Another hindrance is creating scarcity, or a limited supply.

If a product has the potential for an infinite supply, then the item becomes hyperinflated and loses most or all of its value. Also known as “double spending,” a buyer has no way to authenticate that they are the exclusive owner of a digital asset or if that eCoin has been sent to someone else.

Bitcoin: The Genesis of Blockchain

Nearly a decade after Friedman’s prediction, the anonymous Satoshi Nakamoto published his solution to solving digital scarcity and trust in the whitepaper “Bitcoin:

A Peer-to-Peer Electronic Cash System.”[3]

The theory behind Nakamoto’s solution is simple yet elegant.

He describes the creation of a public record of transactions similar to an accounting ledger.

When all transactions are public, then there’s a record to see if a fraudster has transferred their eCoin to someone else already.

In Nakamoto’s words:

“…transactions must be publicly announced, and we need a system for participants to agree on a single history of the order in which they were received.

The payee needs proof that at the time of each transaction, the majority of nodes agreed it was the first received.”[4]

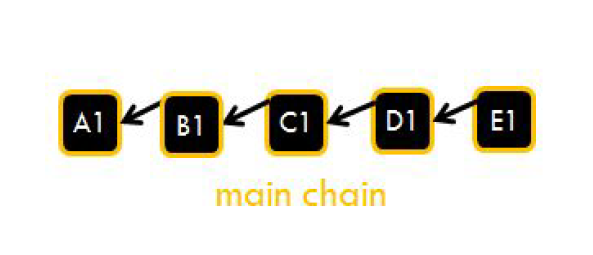

Figure 2: Simple View of Blockchain Block Order

Nakamoto dubbed the public record described as a blockchain.

A blockchain is a digital concept to store data.

This data comes in blocks, so imagine blocks of digital data.

These blocks are chained together, and this makes the data immutable.

When a block of data is chained to the other blocks, its data can never be changed again.

It will be publicly available to anyone who wants to see it ever again, in exactly the way it was once added to the blockchain.

That is quite revolutionary, because it allows us to keep track records of pretty much anything we can think of (to name some: property rights, identities, money balances, medical records), without being at risk of someone tampering with those records.

If I buy a house right now and add a photo of the property rights to a blockchain, I will always and forever be able to prove that I owned those rights at that point. Nobody can change that information if it is put on the blockchain.

So, it is a way to save data and make it immutable.

Simply, when A wants to transfer an eCoin to B, A sends, or broadcasts, the transaction to the blockchain network.

The blockchain network is made up of nodes, or people controlling servers that have a full history of all transaction on that blockchain, in this case the eCoin blockchain.

These nodes are able to authenticate that funds have not been sent to someone else and are in fact controlled by A (thereby solving the trust issue).

The nodes can, if they would like, also authenticate the transaction sent from A to B, affirming funds were in A’s possession are now controlled by B. There people are referred to as miners.

Miners take the transaction A sent to B and combine them with other transactions to form a set of transactions, known as a block.

A miner places the block of transactions after the previous block, thereby creating a chain.

The process of a miner authenticating transactions is known as proof of work, or PoW.

A simplified view of the process can be seen in Figure 1.

Block A comes first, with miners attaching subsequent blocks (B through E) to it as time goes on and more transactions are created.

This chain of transactions (which each node has on record) is known as a blockchain.

As a reward for authenticating transactions, miners receive a payout of whatever the native currency is or a fee paid out by individuals wishing to send a transaction.

It’s important to note that anyone can be a node or a miner, making the system distributed, as seen for the image above.

This is why blockchain is known as a distributed ledger– all nodes have equal weight and are interconnected.

Another way to understand the process is to compare proof of work to how Visa works. Visa is a centralized network, so anytime a credit card is swiped, Visa has all the information about the buyer in their database.

This includes their credit line, payment history, personal information, and more, and allows Visa to give an answer as to whether or not the transaction should be processed or rejected.

In a blockchain, an individual sends a transaction to the network, and instead of a central party validating and processing it, any miner can.

The miner automatically at the record of transactions stored on its server to see if funds have been double spent. If everything checks out, the miner authenticates the transaction, which stays pending until a pre-specified time elapses.

The distributed network layout also provides increased security.

A centralized network like Visa has a single node which authenticates and holds all transactions.

All a hacker or fraudster would have to do is attack the single node and the network would be compromised.

With distributed or decentralized networks, there are multiple nodes holding information and authenticating transactions.

A fraudster would have to “fight” against the authenticating process, or all the honest nodes in the system to get transactions through.

The fraudster would “win” if he/she has a majority of nodes being fraudulent, known as a 51% attack.

That sounds great, but the big question of course is: How does that work?

Step 1 — Transaction data

Alright, let’s start off with an example: the Bitcoin blockchain.

The Bitcoin blockchain is the oldest blockchain in existence.

The blocks on the Bitcoin blockchain are 1 MB of data each.

At the time of writing it counts about 525,000 blocks, meaning roughly a total of 525,000 MB has been stored on this blockchain.

The data on the Bitcoin blockchain however, only exists out of transaction data in regard to Bitcoin transactions.

It is a giant track record of all the Bitcoin transactions that have ever occurred, all the way back to the very first Bitcoin transaction.

This article refers to a blockchain that stores transaction data.

Step 2 — Chaining the blocks

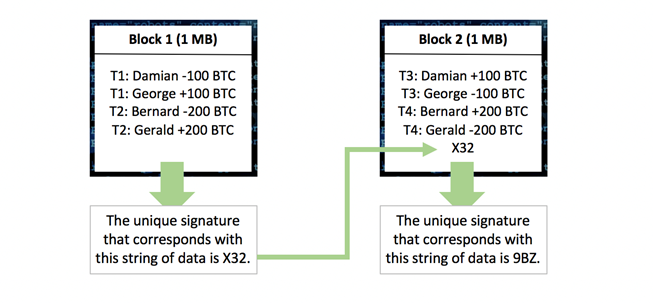

Imagine a bunch of blocks of transaction data (image 1).

Not really special yet, you can compare it to some stand-alone word documents.

Document 1 would then chronologically describe the first transactions that have occurred up to 1 MB, where after the next transactions would be described in document 2 up to another MB, and so on.

These documents are the blocks of data.

These blocks are now being linked (aka chained) together.

To do this, every block gets a unique (digital) signature that corresponds to exactly the string of data in that block.

If anything inside a block changes, even just a single digit change, the block will get a new signature.

This happens through hashing and will be thoroughly explained in step 3.

Let’s say block 1 registers two transactions, transaction 1 and transaction 2.

Imagine that these transactions make up a total of 1 MB (in reality this would be much more transactions).

This block of data now gets a signature for this specific string of data.

Let’s say the signature is ‘X32’. Here is what this looks like:

Remember, a single digit change to the data in block 1 would now cause it to get a different signature!

The data in block 1 is now linked to block 2 by adding the signature of block 1 to the data of block 2.

The signature of block 2 is now partially based on the signature of block 1, because it is included in the string of data in block 2.

Here is what this looks like:

The signatures link the blocks together, making them a chain of blocks.

Let’s picture adding another block to this chain of blocks; block 3. Here is what this looks like:

Now imagine if the data in block 1 is altered.

Let’s say that the transaction between Damian and George is altered and Damian now supposedly sent 500 Bitcoin to George instead of 100 Bitcoin.

The string of data in block 1 is now different, meaning the block also gets a new signature.

The signature that corresponds with this new set of data is no longer X32.

Let’s say it is now ‘W10’ instead. Here is what happens now:

The signature W10 does not match the signature that was previously added to block 2 anymore.

Block 1 and 2 are now no longer chained to each other.

This indicates to other users of this blockchain that some data in block 1 has been altered, and because the blockchain should be immutable, they reject this change by shifting back to a previous record of the blockchain where all the blocks are still chained together.

The only way that an alteration can stay undetected, is if all the blocks stay chained together.

This means for the alteration to go undetected, the new signature of block 1 must replace the old one in the data of block 2.

But if the data of block 2 changes, this will cause block 2 to have a different signature as well.

Let’s say the signature of block 2 is now ‘PP4’ instead of 9BZ.

Now block 2 and 3 are no longer chained together!

The blocks on a blockchain are publicly available to anyone.

So, if an alteration is supposed to stay undetected on a blockchain, all the blocks need to stay properly chained together (otherwise people can tell that certain blocks don’t properly link to each other).

This means that altering a single block requires a new signature for every other block that comes after it all the way to the end of the chain.

This is considered to be impossible.

In order to understand why, you will need to understand how the signatures are created.

Step 3 — How the signature is created

So, let’s picture a block again; block 1. Block 1 is a record of only one transaction.

Thomas sends 100 Bitcoin to David.

This specific string of data now requires a signature.

In blockchain, this signature is created by a cryptographic hash function.

A cryptographic hash function is a very complicated formula that takes any string of input and turns it into a unique 64-digit string of output.

You could for example insert the word ‘Jinglebells’ into this hash function, and you will see that the output for this specific string of data is:

761A7DD9CAFE34C7CDE6C1270E17F773025A61E511A56F700D415F0D3E199868

If a single digit of the input changes, including a space, changing a capital letter or adding a period for example, the output will be totally different.

If you add a period to this word and make it ‘Jinglebells.’ instead, you will see that the output for this specific string of data is:

B9B324E2F987CDE8819C051327966DD4071ED72D998E0019981040958FEC291B

If we now remove the period again, we will get the same output as before:

761A7DD9CAFE34C7CDE6C1270E17F773025A61E511A56F700D415F0D3E199868

A cryptographic hash function always gives the same output for the same input, but always a different output for different input.

This cryptographic hash function is used by the Bitcoin blockchain to give the blocks their signatures.

The input of the cryptographic hash function in this case is the data in the block, and the output is the signature that relates to that.

Let’s have a look at block 1 again.

Thomas sends 100 Bitcoin to David.

Now imagine that the string of data from this block looks like this:

Block 1 Thomas -100 David +100

If this string of data is inserted in the hashing algorithm, the output (signature) will be this:

BAB5924FC47BBA57F4615230DDBC5675A81AB29E2E0FF85D0C0AD1C1ACA05BFF

This signature is now added to the data of block 2.

Let’s say that David now transfers 100 Bitcoin to Jimi.

The blockchain now looks like this:

The string of data of block 2 now looks like:

Block 2 David -100 Jimi +100 BAB5924FC47BBA57F4615230DDBC5675A81AB29E2E0FF85D0C0AD1C1ACA05BFF

If this string of data is inserted in the hashing algorithm, the output (signature) will be this:

25D8BE2650D7BC095D3712B14136608E096F060E32CEC7322D22E82EA526A3E5

And so, this is the signature of block 2.

The cryptographic hash function is used to create the digital signature for each unique block.

There is a large variety of hash functions, but the hashing function that is used by the Bitcoin blockchain is the SHA-256 hashing algorithm.

But how do the signatures stop someone from simply inserting a new signature for each block after altering one (a change goes undetected if all blocks are properly linked, people won’t be able to tell there was a change)?

The answer is that only hashes (signatures) that meet certain requirements are accepted on the blockchain.

This is the mining process and is explained in step 4.

Step 4 — When does the signature qualify, and who signs a block?

A signature doesn’t always qualify.

A block will only be accepted on the blockchain if its digital signature starts with a consecutive number of zeroes.

For example; only blocks with a signature starting with at least ten consecutive zeroes qualify to be added to the blockchain.

However, as explained in chapter 3, every string of data has only one unique hash bound to it. What if the signature (hash) of a block doesn’t start with ten zeroes?

Well, in order to give the block a signature that meets the requirements, the string of data of a block needs to be changed repeatedly until a specific string of data is found that leads to a signature starting with ten zeroes.

Because the transaction data and metadata (block number, timestamp, et cetera) need to stay the way they are, a small specific piece of data is added to every block that has no purpose except for being changed repeatedly in order to find an eligible signature.

This piece of data is called the nonce of a block.

The nonce is completely random and could literally form any set of digits, ranging from spaces to question marks to numbers, periods, capital letters and other digits.

To summarize, a block now contains;

1) transaction data,

2) the signature of the previous block, and

3) a nonce.

The process of repeatedly changing the nonce to find an eligible signature is called mining and is what miners do.

Miners spend electricity in the form of computational power in order to constantly try different nonces.

The more computational power they have, the faster they can insert random nonces and the more likely they are to find an eligible signature faster.

It is a form of trial and error. You can picture it like this:

Any user on a blockchain network can participate in this process by downloading and starting the according mining software for that specific blockchain.

When a user does this, they will simply put their computational power to work in order to try to solve the nonce for a block.

Here is an example of a block of transactions that was recently added to the Bitcoin blockchain, block 521,477:

As you can see, the hash (signature) of this block and the hash of the previous block both start with a number of zeroes.

Finding a hash like that is not easy, it requires a lot of computational power and time, or a lot of luck.

Yes, it sometimes occurs that a miner gets incredibly lucky and finds a matching signature with very little computational power in a matter of minutes.

An extremely rare example recently occurred on block 523,034.

A very small miner with only very little computational power found an eligible signature real fast, while all other miners combined had 7 trillion times as much computational power.

In comparison, the chances of winning the powerball lottery jackpot are one in 292 million, meaning it is 24,000 times easier to win the powerball lottery jackpot than it was for this miner to win the competition versus the rest of the network.

Talk about a number of zeroes. Anyway, important to understand from this chapter is that finding an eligible signature is hard.

Step 5 — How does this make the blockchain immutable?

As discussed previously in step 3, altering a block will unchain it from the subsequent blocks.

In order for an altered block to be accepted by the rest of the network, it needs to be chained to the subsequent blocks again.

See where this is going?

It was previously explained that this requires every block that comes after it to get a new signature.

Giving all of these blocks a new signature will be very costly and time-consuming but doesn’t seem impossible.

It is considered impossible though, and here is the reason why:

Let’s say a corrupt miner has altered a block of transactions and is now trying to calculate new signatures for the subsequent blocks in order to have the rest of the network accept his change.

The problem for him is, the rest of the network is also calculating new signatures for new blocks.

The corrupt miner will have to calculate new signatures for these blocks too as they are being added to the end of the chain.

After all, he needs to keep all of the blocks linked, including the new ones constantly being added.

Unless the miner has more computational power than the rest of the network combined, he will never catch up with the rest of the network finding signatures.

Millions of users are mining on the Bitcoin blockchain, and therefore it can be assumed that a single bad actor or entity on the network will never have more computational power than the rest of the network combined, meaning the network will never accept any changes on the blockchain, making the blockchain immutable.

Once data has been added to the blockchain, it can never be changed again.

There is an exception though.

What if a bad actor hasmore computational power than the rest of the network combined?

Theoretically yes, this is possible.

It is called a 51% attack and has occurred on various blockchains in the past.

In reality though, a 51% attack on the Bitcoin blockchain would be far more costly to execute than it would yield in return.

It would not just require an immense amount of hardware, cooling equipment and storage space for the computational power, but also involves the risk of prosecution and, more importantly, would dramatically harm the ecosystem of the according blockchain itself, rendering the potential returns in Bitcoin to drop significantly in value.

Attempting a 51% attack is practically trying to fight all the other users on a blockchain just by yourself.

This is also the reason that the more users participate in the mining process, the more secure a blockchain becomes.

Congratulations if you are still here, you now (hopefully) understand why a large blockchain is considered immutable. A

n important question arises now though.

How are miners stopped from adding corrupt data to the blockchain (like falsified transaction data)? That is simply impossible!

Step 6 — How is the blockchain governed? Who determines the rules?

The Bitcoin blockchain follows a governance model of democracy, and therefore updates its’ record of transactions (and thus the Bitcoin balances) according to what the majority of its’ users say is the truth.

The blockchain protocol does this automatically by always following the record of the longest blockchain that it has, because it assumes that this chain is represented by the majority.

After all, it requires the majority of the computational power to create the longest version of the blockchain.

This is also how an altered block is automatically rejected by the majority of the network.

The majority of the network rejects an altered block automatically because it is no longer chained to the longest chain.

On the Bitcoin blockchain, all transaction history and wallet balances are public (blockchain.info).

Anyone can look up any wallet or transaction that has ever occurred all the way back to the first transaction that was ever made (on January 3rd, 2009).

Although wallet balances can be checked by anyone publicly, the owners of those wallets remain largely unknown.

It was last used in April 2015, only to show no activity ever since.

Final step, step 7 — Where does this leave cryptocurrencies?

Cryptocurrencies are basically an altered form of Bitcoin.

Most cryptocurrencies are built upon their own blockchain protocol that may have different rules from the Bitcoin blockchain

. Bitcoin is supposed to be a currency, meaning it is explicitly supposed to function as money.

Monero is a cryptocurrency with the same function, but its blockchain protocol has implemented some extra rules that make it a more private currency (transactions are much harder to trace).

Cryptocurrencies can however be given any kind of value, depending on their issuer.

They could be referred to as ‘tokens’.

These tokens can give the owners the right to ‘something’, varying from a gaming license or access to social media to downright electricity or water, you name it.

Any sort of value can be attached to a ‘cryptocurrency’ token.

All these cryptocurrency transactions are registered on various blockchains and can be exchanged online through cryptocurrency exchanges such as Binance.

It is the new money of the internet.

A good example of an industry that might be disrupted soon is the stock market industry.

There is a good chance that company shares and other property rights will be registered as tokens on a blockchain in the near future.

But blockchains are not just limited to registering materialistic value in the form of tokens.

Blockchains also have the potential to safely register data in the form of medical records, identities, history records, tax records and much, much more.

This is why the technology is so huge, and I haven’t even mentioned decentralization yet (another huge aspect of blockchain)!

*-*-*-*-*-*-

51% attack

A 51% attack or double-spend attack is a miner or group of miners on a blockchain trying to spend their crypto’s on that blockchain twice.

They try to ‘double spend’ them, hence the name.

The goal of this isn’t always to double spend crypto’s, but more often to cast discredit over a certain crypto or blockchain by affecting its integrity.

Here is a brief example: let’s say I spend 10 Bitcoin on a luxurious car.

The car is delivered a few days later, and my Bitcoins are transferred from me to the car company.

By performing a 51% attack on the Bitcoin blockchain, I can now try to reverse this Bitcoin transfer.

If I succeed, I will possess both the luxurious car and my Bitcoins, allowing me to spend those Bitcoins again.

The concept of a 51% attack may seem obvious in perspective of a democratic blockchain, but there is a common misconception about how it works

How a 51% attack works

When a Bitcoin owner signs off on a transaction, it is put into a pool of unconfirmed transactions. Miners select transactions from these pools to form a block of transactions.

In order to add this block of transactions to the blockchain, they need to find a solution to a very difficult mathematical problem.

They try to find this solution using computational power.

The more computational power a miner has, the better their chances are to find a solution before other miners find theirs.

When a miner finds a solution, it will be broadcasted to the other miners and they will only verify it if all transactions inside that block are valid according to the existing record of transactions on the blockchain.

Note that even a corrupted miner can never create a transaction for someone else because they would need thedigital signature of that person in order to do that (their private key). Sending Bitcoin from someone else’s account is therefore simply impossible without access to the corresponding private key.

Stealth mining — creating an offspring of the blockchain

Now pay attention.

A malicious miner can however, try to reverse existingtransactions. When a miner finds a solution, they usually broadcast it to all other miners so that they can verify it whereafter the block is added to the blockchain (the miners reach consensus).

However, a corrupt miner can createan offspring of the blockchain by not broadcasting the solutions of his blocks to the rest of the network.

There are now two versions of the blockchain.

One version that is being followed by the uncorrupted miners, and one that is being followed by the corrupted miner.

The corrupted miner is now working on his own version of that blockchain and is not broadcasting it to the rest of the network.

The rest of the network doesn’t pick up on this chain, because after all, it hasn’t been broadcasted. It is isolated to the rest of the network.

The corrupted miner can now spend all his Bitcoins on the truthful version of the blockchain, the one that all the other miners are working on.

Let’s say he spends it on a Lamborghini for example. On the truthful blockchain, his Bitcoins are now spent.

Meanwhile, he does not include these transactions on his isolated version of the blockchain. On his isolated version of the blockchain, he still has those Bitcoins.

Meanwhile, he is still picking up blocks and he verifies them all by himself on his isolated version of the blockchain.

This is where the trouble starts… The blockchain is programmed to follow a model of democratic governance, aka the majority.

The blockchain does this by always following the longest chain, after all, the majority of the miners add blocks to their version of the blockchain faster than the rest of the network.

This is how the blockchain determines which version of its chain is the truth, and in turn what all balances of wallets are based on.

A race has now started. Whoever has the most hashing power will add blocks to their version of the chain faster.

A race — reversing existing transactions by broadcasting a new chain

The corrupted miner will now try to add blocks to his isolated blockchain faster than the other miners add blocks to their blockchain (the truthful one).

As soon as the corrupted miner creates a longer blockchain, he suddenly broadcasts this version of the blockchain to the rest of the network.

The rest of the network will now detect that this (corrupt) version of the blockchain is actually longer than the one they were working on, and they are forced to switch to this chain.

The corrupted blockchain is now considered the truthful blockchain, and all transactions that are not included on this chain will be reversed immediately.

The attacker has spent his Bitcoins on a Lamborghini before, but is now once again in control of those Bitcoins. He is able to spend them again.

This is a double-spend attack. It is commonly referred to as a 51% attack because the malicious miner will require more hashing power than the rest of the network combined (thus 51% of the hashing power) in order to add blocks to his version of the blockchain faster, eventually allowing him to build a longer chain.

So how is Bitcoin secured against this?

In reality these attacks are extremely hard to perform. Like mentioned before, a miner will need more hashing power than the rest of the network combined to achieve this.

Considering the fact that there are millions of miners on the Bitcoin blockchain, a malicious miner would have to spend enormous amounts of money on mining hardware to compete with the rest of the network.

Even the strongest computers on earth are not directly competitive with the total computational power on this network.

And there are countless other arguments against performing a 51% attack.

For example the risk of getting caught and prosecuted, but also electricity costs, renting space and storage for all the mining hardware, covering your tracks and laundering the money.

An operation like this is simply put way too much effort for what it will give the attacker in return, at least in case of the Bitcoin blockchain.

Are other blockchains vulnerable?

Another interesting story is though, regardless of how hard it should be to perform such an attack, that numerous 51% attacks have actually occurred in the past.

In fact, an attack was performed quite recently (april 2018) on the Verge (XVG) blockchain (source).

In this specific case, the attacker found a bug in the code of the verge blockchain protocol that allowed him to produce new blocks at an extremely high pace, enabling him to create a longer version of the Verge blockchain in a short period of time.

As you can see from this case, there are other ways in which a 51% attack can occur, although they are quite rare and often thanks to a bug in the protocol code.

A good team of blockchain developers will most likely detect a bug like this and prevent it from being abused.

A pure look at the security of the Proof of Work algorithm, which is basically the mining principle, tells us that blockchains with a lot of active hashing power become relatively hard to compromise.

However, smaller blockchains with a Proof of Work system, an altcoin for example, may be much more vulnerable to such attacks considering there is way less computational power to compete with for the attacker.

This is why 51% attacks usually occur on small blockchains if they occur at all.

The Bitcoin blockchain has never been compromised by a 51% attack before.

Ghash.io

The mining pool ghash.io briefly exceeding 50% of the bitcoin network’s computing power in July 2014, leading the pool to voluntarily commit to reducing its share of the network. It said in a statement that it would not reach 40% of the total mining power in the future.

Krypton and Shift

Krypton and Shift, two blockchains based on ethereum, suffered 51% attacks in August 2016.

Bitcoin Gold

In May of 2018, Bitcoin Gold, at the time the 26th-largest cryptocurrency, suffered a 51% attack. The malicious actor or actors controlled a vast amount of Bitcoin Gold’s hash power such that even with Bitcoin Gold repeatedly attempting to raise the exchange thresholds, the attackers were able to double-spend for several days, eventually stealing more than $18 million worth of Bitcoin Gold.

*-*-*-*-*-*-*-*

Now… we can continue with ……. Nakamoto…

In the case of some of the largest public blockchains, can have above 10K[5] and even 20K[6] nodes, making a 51% attack extremely difficult.

Nakamoto decided to create an experimental store of value using his blockchain invention and created a digital currency, or cryptocurrency, called Bitcoin.

He distributed funds to anyone who wanted to experiment using the technology.

He also wrote into the computer code behind Bitcoin a limited supply of coins that could be created, thereby creating digital scarcity.

Although Nakamoto’s initial application dealt strictly with a cryptocurrency, anything of value can be transferred via a blockchain.

For example, music, video, or image files can be stored on a blockchain and bought, sold, or transferred, with all transactions public.

The same can be applied to stocks or any other digital asset, whether it exists in the physical or digital world.

Ethereum: A Decentralized Platform

Five years after Nakamoto published the Bitcoin white paper, a miner by the name of Vitalik Buterin published his vision of blockchain. Entitled “Ethereum:

The Ultimate Smart Contract and Decentralized Application Platform,”[7] Buterin builds on top of Nakamoto to create something entirely new. In Buterin’s words:

“The intent of Ethereum is to create an alternative protocol for building decentralized applications, providing a different set of tradeoffs that we believe will be very useful for a large class of decentralized applications…

Ethereum does this by building what is essentially the ultimate abstract foundational layer:

a blockchain with a built-in Turing-complete programming language, allowing anyone to write smart contracts and decentralized applications where they can create their own arbitrary rules for ownership, transaction formats, and state transition functions.”[8]

Ethereum, in essence, allows for the creation of smart contracts on top of a blockchain.

A simple way to understand smart contracts is the sale of a home via an escrow account.

A wants to buy a house from B, but he wants the funds to sit in an escrow account until he’s done a title check, inspected the home, and any other precursor to taking full ownership.

A sends funds to a smart contract account, and B sends the house deed to the same smart contract account.

The smart contract automatically observes the terms specified (the conditions described above in our case) have been met or not.

If at any point the smart contract is breached, funds go back to their respective parties. If all requirements are fulfilled, then the exchange is automatically executed, and A takes ownership of the home.[9]

Ethereum allows anyone to build a smart contract based application, known as distributed apps or dApps, on its blockchain.

These dApps can be anything, from casinos to purchasing cloud storage, from real estate transactions described above to buying computing power- the possibilities are endless.

A comparison can be made between the evolution of cell phones, an example Buterin himself uses.

Cell phones started as a mobile way to communicate with one another.

This is akin to sending Bitcoin payment transactions over a blockchain.

Then the smartphone came out, which includes internet access, text messaging, and an infinite number of apps.

The smartphone is like Ethereum, where functions other than sending payments (like reserving cloud storage, taking part in an auction, creating an organization, etc.) are available on top of the platform.

Ethereum created a cryptocurrency for its platform, known as ether, but the functionality is different than that of Bitcoin. Ethereum serves as a store of value in the same way Bitcoin does but also serves as a way of triggering smart contacts.

Ether is used as gas the same way a car uses gas, a means of triggering an event. So, when interacting with any smart contract built upon Ethereum, a little bit of ether needs to be sent along with other digital assets.

The impact of blockchains on the digital world

Digging further, the fact that blockchains are a step forward towards a better understanding of the IoT is undeniable, blockchains are the state of the art technology that has benefited in the development of the digital world in many ways, some of them will be discussed below:

- Eliminating Risk: Two parties are able to partake in a transaction without the fear of fraud, as third parties are not involved in the process whatsoever. This greatly removes any financial risks regarding a basic transaction and promotes welfare.

- Empowerment of the users: Users are in control of their individual profile and hold credit over the services they have provided by mining to gain access to blocks and in return earn significant bitcoins. This sense of control promotes further transactions as the user profile is made private for each user.

- Superior data: Blockchains provide complete data, with no room left for further interpretation, eliminating the chances of error. The data provided by blockchains is complete, accurate and timely, making the digital world absolute.

- Faster Transactions: In the traditional terms, processing of transactions can be time-consuming, at least in comparison with online transactions. Blockchain transactions are not bound to office hours and no physical presence at the bank is required in order for the transaction to take place.

- Immutability: Blockchains can be freely viewed by the public. They are transparent, any change can be viewed. However, the transactions being made are immutable, which means they cannot be altered or deleted once they have taken place.

Reliability and Longevity: As stated multiple times above, blockchains are decentralized. The less the concentration, the less are the chances of an attack from any malicious programs, making blockchains highly reliable and longevity. Adding further into the perks of using digital platforms.

-*-*-*-*-*-*-*-*-*-*

[1] Full video: https://www.youtube.com/watch?v=leqjwiQidlk, https://www.coindesk.com/economist-milton-friedman-predicted-bitcoin/

[2] https://blog.synereo.com/2017/03/20/epiphytian-decentralization-a-new-business-model-for-ugc-publishing/

[3] https://bitcoin.org/bitcoin.pdf

[4] Ibid, p. 2

[6] https://www.ethernodes.org/network/1

[7] https://github.com/ethereum/wiki/wiki/Ethereum-White-Paper

[8] ibid

[9] It should be noted that although smart contacts are called “smart,” they are only as effective as the terms placed on them. If an individual enters into a smart contract without understanding terms is the same as someone who signs a contract without reading it.

{kind=link}