Competitive Coexistence: Post-War Strategic Outlook")

Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

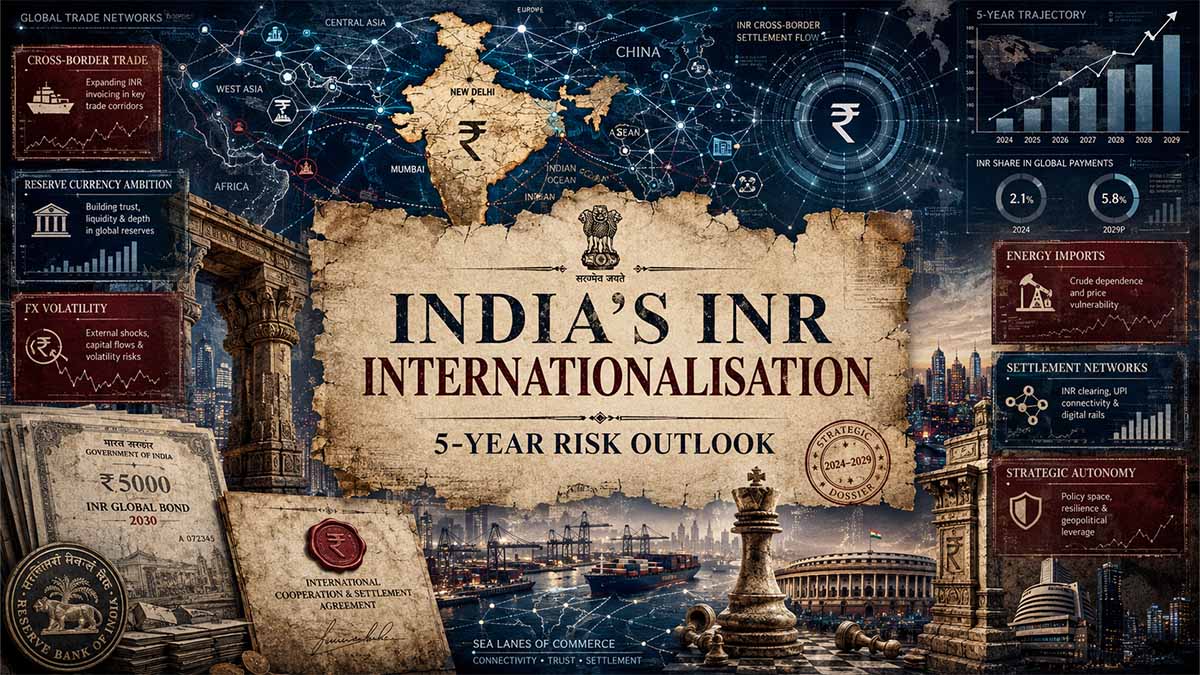

Executive Summary

BLUF: India’s rupee internationalisation is no longer symbolic monetary diplomacy; it is a controlled, state-led attempt to expand INR use in trade settlement, cross-border finance, reserve-adjacent liquidity, and strategic autonomy.

The operational base is already visible through Special Rupee Vostro Accounts, rupee invoicing, market-determined exchange-rate settlement, and wider use of rupee accounts for non-resident trade and investment flows — International Trade Settlement in Indian Rupees – Reserve Bank of India – April 2026; Ministry of Finance Year Ender 2025 – Government of India – January 2026.

The 2026–2031 outlook is not “rupee replacing the dollar”; it is selective currency weapon-resilience, where India reduces exposure to external payment chokepoints while avoiding destabilising full capital-account liberalisation.

The main upside scenario is a deeper INR trade-settlement corridor across energy, commodities, services, remittances, and South–South commerce.

The main downside scenario is a shallow internationalisation trap: foreign counterparties accept INR only when they can recycle it into Indian assets, exports, or regulated investment channels.

Bayesian baseline: moderate-probability, high-impact gradualisation; not a currency revolution, but a durable institutional thickening of rupee-denominated settlement infrastructure.

Navigational Index

- Settlement Architecture and Monetary Sovereignty — how rupee invoicing, SRVAs, SNRR accounts, CBDC experimentation, and bilateral settlement channels reduce transaction friction and strategic exposure.

- Liquidity, Convertibility, and Market-Depth Constraints — why India’s growth scale supports INR expansion but capital-account management, hedging depth, bond-market absorption, and external-balance volatility remain limiting variables.

- Geopolitical Shock Channels and 5-Year Scenarios — how Russia, the UAE, Africa, EU trade exposure, China’s RMB playbook, sanctions risk, energy pricing, and payment-network fragmentation shape the INR’s international perimeter.

INR Internationalisation Clarity Schema

Interactive synthesis dashboard converting the full analytical report into five structured layers: core concepts, bottlenecks, strengths, projections, and metric anchors. The design is optimized for WordPress, high-density OSINT reading, and visual strategic prioritization.

• Rupee Invoicing

Trade contracts can be priced and settled in Indian rupees instead of forcing every transaction through a third currency such as the USD. This reduces conversion friction and gives India more monetary room during external shocks.

• Special Rupee Vostro Accounts

Foreign banks can hold rupee accounts with Indian authorised dealer banks. This creates the operational rail for import and export settlement, but it works only if foreign holders can reuse rupee balances productively.

• Non-Resident Rupee Interface

Special Non-Resident Rupee accounts provide a controlled way for non-residents to use rupees for permitted trade, investment, borrowing, and related transactions without opening the capital account completely.

• Digital Rupee Experimentation

CBDC and tokenisation testing can reduce settlement delay, improve programmability, and support future cross-border payment models, but it remains a testing layer rather than full-scale global production infrastructure.

• Bilateral Settlement Channels

Russia, the UAE, Africa, and selected payment corridors create demand for alternatives to dollar-heavy settlement. The benefit is resilience; the risk is trapped balances, sanctions exposure, and uneven counterparty liquidity.

• Liquidity and Hedging

International currency use requires deep markets, reliable hedging, investable bonds, and predictable exit routes. India’s growth supports adoption, but market usability determines whether rupee settlement becomes durable.

Rupee Balance Recycling

Root cause → Foreign exporters may accumulate INR faster than they can reuse it. Current impact → Settlement adoption can stall if balances cannot be deployed into Indian goods, securities, investments, or further trade.

Hedging Depth

Root cause → Firms and investors need liquid forwards, swaps, and derivatives to manage rupee risk. Current impact → High hedging cost increases pricing risk and limits willingness to invoice or invest in INR.

Capital-Account Caution

Root cause → India protects domestic stability through controlled convertibility. Current impact → This lowers crisis risk but slows foreign users who need flexible entry, exit, and reinvestment routes.

Energy Pricing Dollar Gravity

Root cause → Oil, LNG, insurance, shipping, and commodity finance remain heavily dollar-linked. Current impact → INR can expand in negotiated corridors, but global energy pricing still limits broad displacement.

Sanctions and Compliance Risk

Root cause → Russia-linked trade and payment-network fragmentation raise due-diligence burdens. Current impact → Banks may slow, refuse, or reprice transactions if secondary-sanctions or correspondent-bank exposure increases.

Bond-Market Absorption

Root cause → Foreign rupee balances require safe, liquid, scalable rupee assets. Current impact → Government securities help, but foreign-flow shocks can amplify yield and FX volatility if market depth is insufficient.

• India’s Growth Scale

India’s large and fast-growing economy gives counterparties a reason to hold or reuse INR. Scale drives value because currency acceptance rises when the issuing economy offers trade, consumption, investment, and asset opportunities.

• RBI Settlement Framework

SRVAs and rupee invoicing create a bank-based mechanism for settlement. This increases resilience because India does not need full capital-account liberalisation to build practical transactional use.

• UAE Corridor

The INR–AED channel benefits from energy trade, gold flows, remittances, and regional liquidity. It is one of the most practical corridors because it joins payment utility with real trade density.

• UPI and CBDC Capability

India’s digital payment infrastructure supports faster cross-border experiments. This improves transaction speed and cost, even if it does not automatically create deep rupee asset demand.

• Payment Redundancy

National-currency settlement reduces forced dependence on a single external settlement network. It strengthens resilience during sanctions shocks, dollar funding stress, or payment-infrastructure disruption.

• Controlled Convertibility

India’s cautious capital-account posture lowers sudden-stop risk. It slows internationalisation, but it prevents rupee expansion from becoming a destabilising external balance-sheet shock.

[Short-term 0–6 mo]

IF banks expand SRVA operations and firms receive clearer settlement guidance → THEN INR use rises first in selected bilateral trade, not broad global invoicing.

[Mid-term 6–18 mo]

IF hedging depth and rupee asset access improve → THEN foreign counterparties become more willing to hold INR balances instead of treating rupee settlement as temporary accounting.

[Long-term >18 mo]

IF UAE, Africa, EU payment links, and strategic corridors scale together → THEN INR becomes a selective regional settlement currency, not a full reserve substitute.

| Metric / Indicator | Current Value | Trend / Status | Strategic Relevance |

|---|---|---|---|

| India FY26 growth | 7.6% | [Verified] Strong growth base | Supports foreign willingness to hold or reuse INR. |

| FY27 projected growth | 6.6% | [Verified] Moderating but strong | Maintains macro gravity behind INR settlement expansion. |

| India-UAE trade | USD 84 billion | [Verified] High-density corridor | Provides operational foundation for INR-AED settlement. |

| India-Africa trade | USD 81.99 billion | [Verified] Strategic corridor | Supports local-currency and lower-cost payment experiments. |

| EU-India goods trade | EUR 118 billion | [Verified] Large but compliance-heavy | Payment interoperability may grow faster than INR invoicing. |

| India crude import projection | 5.8 mb/d by 2030 | [Verified] Energy exposure rising | Energy payments make settlement sovereignty strategically important. |

| Scenario baseline | 50–55% | [Estimated] Controlled expansion | Most likely path: corridor growth without reserve-currency breakout. |

| Stress-reversal scenario | 5% | [Estimated] Low probability, high impact | Oil, dollar, or capital-flow shock could slow internationalisation. |

Data-quality tags reflect the source basis used in the analytical report: verified values are taken from official institutional sources; scenario percentages are analytical estimates derived from the risk model and are not official statistical series.

Master Abstract

India’s rupee internationalisation should be analysed as a sequenced sovereignty project rather than a linear reserve-currency campaign: the immediate objective is not to displace the USD, but to widen the transactional domain in which Indian firms, banks, importers, exporters, remittance channels, and partner-country institutions can settle value without forced intermediation through a dominant third currency. The verified policy architecture already contains three critical building blocks: first, the RBI framework for international trade settlement in INR, where authorised dealer banks operate Special Rupee Vostro Accounts and exchange rates are market-determined; second, the Government of India’s approval pathway for allowing surplus rupee balances in SRVAs to be used more flexibly; third, the wider non-resident rupee-account ecosystem, including SNRR account usage for specified trade, foreign investment, external commercial borrowing, and related transactions — International Trade Settlement in Indian Rupees – Reserve Bank of India – April 2026; Special Non-Resident Rupee Accounts – Reserve Bank of India – January 2025; Ministry of Finance Year Ender 2025 – Government of India – January 2026. In structural analytic terms, this creates an incremental H₁ sovereignty corridor: India lowers dollar-conversion dependency for selected transactions, but does not yet remove the hard constraint that external counterparties must want to hold, spend, hedge, or invest rupees. The 5-year Bayesian prior is therefore not “rapid reserve-currency emergence” but “managed transactional internationalisation,” with probability mass concentrated around a scenario in which INR invoicing expands fastest in partner networks where India has import leverage, export complementarity, diaspora-linked flows, or strategic balancing incentives. The strongest macro support is India’s growth base: the World Bank reported that India remained among the fastest-growing major economies, with FY26 growth accelerating to 7.6 percent and FY27 growth projected at 6.6 percent despite external headwinds — India Development Update – World Bank – April 2026. The strongest macro constraint is that currency internationalisation normally requires deep, liquid, open, and trusted financial markets; BIS-published central-bank analysis explicitly ties rupee internationalisation to macro-financial stability, deep markets, and convertibility conditions, while also noting that the rupee has historically traded more offshore than onshore and that India has pursued local-currency settlement arrangements across Asia and the Middle East — Future Readying India’s Monetary Policy – Bank for International Settlements – July 2024; Foreign Exchange Market and Cross-Border Cooperation – Bank for International Settlements – June 2016. The competing hypotheses are therefore: ACH₁, controlled settlement deepening succeeds without destabilising convertibility; ACH₂, counterparties accumulate unwanted INR balances and usage plateaus; ACH₃, geopolitical fragmentation accelerates rupee demand in sanctions-sensitive corridors; ACH₄, dollar liquidity preference dominates under crisis conditions; ACH₅, India’s own capital controls and market-depth limits slow foreign institutional recycling of rupees. The posterior estimate after current evidence is weighted toward ACH₁ plus ACH₂: India is building credible pipes, but pipes alone do not create global currency preference unless liquidity, asset access, hedging instruments, and trade-balance recycling mature together.

The 2026–2031 outlook is best understood through a Monte Carlo-style scenario envelope rather than a single forecast. In the baseline path, assigned here a 55 percent analytic probability, India expands rupee settlement through SRVAs, bilateral national-currency arrangements, selected CBDC cross-border pilots, and greater rupee invoicing in trade corridors where Indian import demand gives New Delhi negotiating leverage; the practical effect is reduced transaction cost, lower dollar-conversion exposure, and a stronger payments fallback during geopolitical disruption, but not full reserve-currency status. In the accelerated sovereignty path, assigned 25 percent, external shock frequency rises: sanctions spillovers, energy-market volatility, payment-network fragmentation, and partner-country reserve diversification raise the value of non-dollar settlement options, allowing India to expand INR settlement in energy, defence-adjacent procurement, pharmaceuticals, food, services, and infrastructure-linked trade. Russia–India official language already points in this direction: the 2025 joint statement said both sides would continue developing bilateral settlement systems using national currencies — Joint Statement following the 23rd Russia-India Annual Summit – Kremlin – December 2025. The Russia channel matters because it is not only commercial; it is a laboratory for transaction continuity under sanctions pressure, discount-energy flows, and payment-system segmentation. In the stagnation path, assigned 15 percent, INR use expands in headline agreements but remains thin in real liquidity because exporters, banks, and foreign counterparties cannot efficiently hedge rupee risk or recycle balances into attractive Indian assets. In the stress-reversal path, assigned 5 percent, India faces a balance-of-payments or capital-flow shock severe enough that policymakers prioritise domestic exchange-rate stability over external rupee ambition, slowing liberalisation and forcing internationalisation back into a narrow trade-settlement lane. The EU and China comparison sharpens the model: the EU’s India economic footprint shows high trade and investment density, but not necessarily rupee-denominated settlement preference, while China’s official investment guide frames RMB internationalisation as part of orderly opening and institutional depth, underscoring that currency expansion follows market architecture, not diplomatic slogan — EU Economic Footprint in India – European External Action Service – June 2026; Foreign Investment Guide of the People’s Republic of China 2024 – Government of China – 2024. The shadow dimensions are decisive: mercenary and defence-linked procurement networks increase demand for resilient settlement channels; cyber-norm fragmentation raises demand for payment redundancy; liquidity flows determine whether INR balances become useful assets or trapped accounting claims; and commodity trade determines whether rupee corridors can scale beyond symbolic bilateralism.

Five-Year Rupee Sovereignty Matrix

Adjust the structural variables to simulate whether India’s rupee internationalisation remains a narrow trade-settlement mechanism, becomes a scalable South–South liquidity corridor, or stalls because counterparties cannot recycle INR balances efficiently.

SRVA Corridor

Trade invoicing and settlement through rupee vostro rails.

Asset Recycling

Foreign holders need usable Indian instruments and hedges.

Energy Vector

Commodity imports create leverage but also imbalance risk.

CBDC Bridge

Digital rupee pilots may compress settlement latency.

Shock Exposure

Sanctions, cyber disruption, and liquidity stress test credibility.

Settlement Architecture and Monetary Sovereignty: INR Internationalisation 2026–2031

India’s settlement architecture for rupee internationalisation is best understood as a layered monetary-sovereignty system, not as a premature attempt to make the INR a reserve currency equivalent to the USD, EUR, or RMB. The core mechanism is administrative-financial rather than rhetorical: authorised dealer banks can settle international trade in rupees through Special Rupee Vostro Accounts held by correspondent banks of partner countries, with invoicing, exchange-rate determination, settlement, and surplus-balance use routed through a regulated banking framework; the Reserve Bank of India states that international trade settlement in Indian rupees uses SRVAs, permits invoicing in rupees, and requires the exchange rate between partner currencies to be market-determined — International Trade Settlement in Indian Rupees – Reserve Bank of India – January 2025. This matters because the sovereignty gain does not arise from declaring the rupee “international,” but from reducing the number of obligatory conversion points between Indian importers, exporters, foreign banks, and payment rails that are denominated or cleared through external currencies. SRVAs create the operational bridge; SNRR accounts create a wider non-resident rupee-account logic; digital public infrastructure and CBDC experimentation create a future settlement-speed layer; and bilateral national-currency channels create geopolitical insulation when partner states face dollar liquidity constraints, sanctions exposure, or trade-finance frictions. The RBI separately states that Special Non-Resident Rupee Accounts may be used for specified transactions in trade, foreign investment, external commercial borrowing, and related activities, which means the account architecture is not only a trade-payment tool but also a controlled interface between non-resident capital activity and India’s rupee-denominated financial system — Special Non-Resident Rupee Accounts – Reserve Bank of India – January 2025. In Bayesian terms, these verified design features update the hypothesis H₁ from “symbolic de-dollarisation rhetoric” toward “regulated transactional internationalisation”; the posterior probability of a narrow but durable rupee-settlement expansion is materially higher than the probability of a sudden reserve-currency leap because the infrastructure supports settlement continuity before it supports deep international asset preference.

| Layer | Verified institutional mechanism | Monetary-sovereignty function | 5-year bottleneck |

|---|---|---|---|

| Rupee invoicing | INR invoicing under RBI trade-settlement framework | Reduces mandatory third-currency invoicing | Counterparty acceptance and pricing confidence |

| SRVA | Foreign bank vostro account with Indian authorised dealer bank | Creates rupee settlement rail for imports and exports | Surplus rupee recycling into goods, securities, or investments |

| SNRR | Non-resident rupee account for specified transactions | Links trade, investment, and borrowing interfaces | Regulatory caution and permissible-use boundaries |

| CBDC / tokenisation sandbox | RBI digital-rupee and asset-tokenisation testing environment | Tests programmable, interoperable settlement models | Cross-border legal finality and interoperability |

| Bilateral national-currency channel | India–partner settlement arrangements | Reduces strategic exposure to external payment chokepoints | Liquidity asymmetry and sanctions spillover risk |

The first analytic pillar is rupee invoicing, because invoice currency determines who absorbs exchange-rate risk, which banking rails intermediate the transaction, and whether trade finance depends on access to third-currency liquidity. In standard dollar-dominant trade, an Indian importer buying energy or commodities from a non-dollar partner often faces a chain of conversion, correspondent banking, liquidity provisioning, and settlement messaging that increases cost and exposes the transaction to foreign monetary conditions. Under the RBI rupee-settlement framework, the exporter and importer can denominate the invoice in INR, while authorised dealer banks settle through SRVAs; this reduces currency-conversion layers even when the partner’s domestic currency remains relevant for internal accounting. The sovereignty effect is therefore friction compression plus policy optionality: India can preserve foreign-exchange reserves for genuinely external needs, reduce the pass-through from dollar funding stress into routine bilateral commerce, and offer partner states a route into Indian goods, securities, or investment opportunities without first acquiring dollars. The strongest official macro support for this strategy is India’s scale and growth persistence: the World Bank states that India remained the fastest-growing major economy in FY26, with growth accelerating to 7.6 percent, a current-account deficit of 1 percent of GDP, and FY27 growth projected at 6.6 percent despite external headwinds — India Development Update – World Bank Group – April 2026. This supports rupee internationalisation because counterparties are more likely to hold, spend, or invest a currency when the issuing economy supplies growth, trade depth, and asset absorption capacity. But the same evidence does not prove a reserve-currency transition; it proves a stronger transactional foundation. The Bayesian update is therefore asymmetric: strong growth raises H₁, “settlement expansion,” but only moderately raises H₂, “deep currency internationalisation,” because the latter requires liquid, open, hedgeable financial markets and broad foreign confidence in rupee asset convertibility.

INR Local Currency Settlement System

Architectural schematic of Special Rupee Vostro Account operations, trade clearing pipelines, and sovereign surplus liquidity recycling vectors.

Indian Importer / Exporter

FUNCTIONAL DESCRIPTION

The domestic trading base executing bilateral trade cross-border contracts. Initiates goods and services transactions without relying on legacy hard-currency intermediate conversions.

INR Invoice Agreement

EXCHANGE RISK MITIGATION

Invoicing is mutually locked in INR with the foreign counterparty. Eliminates reliance on third-party baseline clearing metrics (e.g., USD, EUR) and shields the domestic enterprise from spot-market volatility.

Authorised Dealer Bank

OPERATIONAL MANDATE

Domestic banking node licensed by the Reserve Bank of India. Manages regulatory compliance reporting, verifies underlying trade documentation, and interfaces with global partner systems.

Special Rupee Vostro Account

CLEARING INFRASTRUCTURE

An account held by a domestic AD bank on behalf of a foreign partner bank. Functions as a local liquidity reservoir where bilateral trade balances are maintained directly in INR.

Bilateral Settlement Channels

INR is credited directly into the SRVA upon verified cargo receipt.

INR is debited directly from the account to pay domestic exporters.

SYSTEM FLOW METRIC

Real-time balancing engine operating across cross-border banking rails without third-party correspondent dependencies.

Surplus INR Balance Investment

Indian Export Scaling: Settlement of trade back into the Indian export ecosystem.

Government Securities: Reinvestment into liquid sovereign treasury bonds ($G\text{-Secs}$).

Permitted FDI Inflow: Direct investment into approved corporate equity and projects.

Future Payment Rails: Programmable settlement integration via CBDC ($e\text{Rupee}$) layers.

The second pillar is SRVA balance recycling, because the success of rupee settlement depends less on opening accounts and more on what foreign counterparties can do with accumulated rupees after settlement. A partner bank accepting INR for exports to India must be able to recycle rupees into imports from India, investment in permitted Indian instruments, repatriation where allowed, or further trade settlement; otherwise the system produces trapped balances and discourages repeat usage. The RBI framework addresses this by permitting the use of surplus rupee balances for eligible current and capital-account transactions subject to regulatory conditions, while SNRR accounts create a broader non-resident rupee interface for specified transactions — International Trade Settlement in Indian Rupees – Reserve Bank of India – January 2025; Special Non-Resident Rupee Accounts – Reserve Bank of India – January 2025. The Analysis of Competing Hypotheses gives five plausible frameworks: H₁, rupee settlement deepens because India’s growth and import demand create natural liquidity; H₂, rupee usage plateaus because partner countries cannot recycle balances efficiently; H₃, geopolitical fragmentation accelerates use in sanctions-sensitive corridors; H₄, dollar liquidity preference dominates whenever global stress rises; H₅, India’s own regulatory caution preserves stability but slows international scale. Current evidence favours a blended H₁–H₂ baseline: India has credible pipes, but pipes are not liquidity. The IMF reports that India’s financial and corporate sectors remained resilient, supported by adequate capital buffers and low non-performing assets, and that the current-account deficit was contained with support from service exports — India: 2025 Article IV Consultation – International Monetary Fund – November 2025. That macro-financial resilience supports foreign acceptance of rupee claims, but the leap from acceptance to preference remains conditional on hedging liquidity, capital-market depth, operational simplicity, and confidence that rupee balances can be converted into useful Indian economic exposure rather than stranded bilateral accounting entries.

| ACH framework | Core proposition | Evidence weight | 2026–2031 implication |

|---|---|---|---|

| H₁: Controlled deepening | INR settlement expands through regulated trade and investment rails | High | Most likely baseline |

| H₂: Recycling bottleneck | Foreign counterparties resist holding excess INR | High | Main operational constraint |

| H₃: Geopolitical acceleration | Sanctions and payment fragmentation raise demand for non-dollar settlement | Medium-high | Strong in Russia-linked and multipolar corridors |

| H₄: Dollar stress reversion | Crisis periods increase preference for USD liquidity | Medium | Limits rupee use during global risk-off shocks |

| H₅: Regulatory self-limitation | India preserves stability through cautious convertibility | High | Slower but safer internationalisation |

The third pillar is the SNRR account layer, which should be treated as the connective tissue between trade settlement and controlled capital mobility. SNRR accounts matter because a purely trade-based rupee settlement system can reduce friction in specific import-export flows, but cannot by itself create a wider rupee ecosystem unless non-residents can use rupees for permitted commercial, investment, borrowing, and ancillary transactions. The RBI states that SNRR accounts may be used for specified transactions in trade, foreign investments, external commercial borrowings, and related purposes, and this provides a crucial architecture for turning bilateral rupee balances into a more generalised non-resident rupee interface — Special Non-Resident Rupee Accounts – Reserve Bank of India – January 2025. The monetary-sovereignty gain is precise: India can widen rupee use while preserving capital-account management, rather than copying the Chinese or euro-area model wholesale. The Chinese comparison is instructive because official Chinese sources present RMB internationalisation as inseparable from cross-border payment use, investment and financing, bond-market access, and macroprudential management; China’s State Council reported that the People’s Bank of China would promote RMB use in cross-border payments, pricing, investment, and financing, while a government-published 2024 foreign investment guide states that PBOC and SAFE administer cross-border RMB and foreign-exchange activity — China’s Central Bank to Promote Cross-Border RMB Use – State Council of the People’s Republic of China – February 2025; Foreign Investment Guide of the People’s Republic of China 2024 – State Council of the People’s Republic of China – 2024. India’s pathway is likely to remain more conservative: less open than a fully liberal capital account, less state-exported than China’s RMB corridor model, but increasingly functional for partners that trade heavily with India, need payment redundancy, or can recycle rupees into Indian demand.

Bilateral Trade ACH Dependency Map

Cross-impact mapping of geopolitical hypotheses, core operational dependencies, and macro-financial trigger vectors.

Controlled INR Deepening

CRITICAL DEPENDENCIES

STRATEGIC VECTOR ASSESSMENT

Requires a stable increase in non-oil trade pipelines and direct authorization pathways to sustain long-term cross-border liquidity without generating persistent offshore structural market imbalances.

Recycling Bottleneck

TRIGGER VECTOR PARAMS

STRATEGIC VECTOR ASSESSMENT

Triggered when asymmetric export dynamics block foreign partner central banks from converting surplus INR positions, stranding currency inside non-convertible local capital frameworks.

Geopolitical Acceleration

TRIGGER VECTOR PARAMS

STRATEGIC VECTOR ASSESSMENT

Accelerates real-world adoption of alternative settlement methods as nations seek to bypass traditional Western clearings to secure essential energy corridors and supply chain access chains.

Dollar Stress Reversion

TRIGGER VECTOR PARAMS

STRATEGIC VECTOR ASSESSMENT

A powerful structural constraint where severe global liquidity crises trigger a flight-to-safety, causing central banks to re-allocate capital back to deep, liquid US Dollar assets.

Regulatory Self-Limitation

TRIGGER VECTOR PARAMS

STRATEGIC VECTOR ASSESSMENT

Occurs when domestic central banking authorities choose to limit internationalization pacing to preserve domestic monetary autonomy, manage inflation targets, and control exchange rate boundaries.

The fourth pillar is CBDC experimentation and payment-system interoperability, because India’s settlement-sovereignty strategy is not limited to bank-account structures; it also involves technological attempts to make cross-border value transfer faster, cheaper, more programmable, and less dependent on legacy correspondent banking. The RBI describes its Digital Rupee architecture and, more specifically, its CBDC and Asset Tokenisation Sandbox as a non-live testing environment for innovation in payments, settlements, cross-border use cases, interoperability, programmability, and asset-tokenisation models — Digital Rupee FAQs – Reserve Bank of India – 2026. This is not yet proof of a production-grade cross-border rupee CBDC corridor, but it is evidence of institutional experimentation in the exact domain that could compress settlement latency and reduce reconciliation risk over the next five years. The BIS provides the global context: Project Nexus is designed to connect domestic instant-payment systems to improve cross-border payment speed, cost, transparency, and access, and the BIS announced in July 2024 that Nexus had completed a blueprint for connecting domestic instant payment systems globally — Project Nexus: Enabling Instant Cross-Border Payments – Bank for International Settlements – July 2024; Project Nexus Completes Comprehensive Blueprint – Bank for International Settlements – July 2024. The European side is also relevant: the European Central Bank stated in November 2025 that the Eurosystem was moving forward on exploratory work to connect TIPS with UPI, noting that UPI is regulated by the RBI and that India is among the top ten recipients of euro-area remittances — Eurosystem Moves Forward on Work to Connect TIPS with UPI – European Central Bank – November 2025. For India, this creates a future settlement stack in which SRVAs handle bank-based rupee settlement, SNRR accounts handle non-resident rupee positioning, UPI-linked corridors reduce small-value payment friction, and CBDC/tokenised settlement pilots test programmable value transfer for wholesale or cross-border use.

| Payment architecture vector | Officially verified status | Strategic exposure reduced | Residual risk |

|---|---|---|---|

| SRVA | RBI-enabled rupee trade-settlement account | Third-currency settlement dependence | Liquidity recycling |

| SNRR | RBI-recognised non-resident rupee account for specified transactions | Fragmented non-resident rupee access | Regulatory scope limits |

| UPI cross-border linkage | ECB exploratory work on TIPS–UPI connection | Remittance friction and payment latency | Legal interoperability |

| CBDC sandbox | RBI non-live testing for payments, cross-border and tokenisation use cases | Settlement finality and programmable settlement friction | Production scalability |

| Nexus-style interoperability | BIS blueprint for linking instant payment systems | Correspondent-banking dependency in small-value payments | Governance and participant onboarding |

The fifth pillar is bilateral and minilateral settlement diplomacy, where India’s rupee architecture intersects with geopolitical fragmentation. The Russia vector is the clearest official test case because Moscow and New Delhi have repeatedly endorsed national-currency settlement in official statements. The Kremlin’s published joint statement after the 2024 India–Russia annual summit states that the two sides agreed to continue working together to promote a bilateral settlement system using national currencies — Joint Statement Following the 22nd India–Russia Annual Summit – Kremlin – July 2024. This does not mean every Russia–India transaction is smoothly or fully settled in rupees; it means both states view national-currency settlement as a strategic channel for reducing external payment vulnerability. In monetary-sovereignty terms, Russia-linked settlement is simultaneously an opportunity and a stress test: opportunity, because sanctions pressure and disrupted payment access increase partner willingness to use alternatives; stress test, because imbalanced trade flows can produce rupee surpluses that are difficult for the exporting partner to recycle if Indian export supply, asset access, or conversion pathways are insufficient. The Kremlin also published language in the 2021 bilateral statement that mutual settlement in national currencies would help reduce cost and risk exposure, reinforcing that this is a long-running policy direction rather than a single-cycle reaction — Partnership for Peace, Progress and Prosperity: India–Russia Joint Statement – Kremlin – December 2021. The five-year outlook therefore assigns high importance to the I₁ liquidity-recycling variable: if partner-country exporters can use INR to buy Indian goods, invest in permitted securities, fund Indian operations, or participate in authorised projects, rupee settlement becomes self-reinforcing; if not, it becomes a politically useful but economically constrained workaround. The sovereignty effect is real, but it is not free: every gain in payment autonomy must be matched by balance-sheet usability.

The sixth pillar is India’s relationship with large, highly regulated trade partners such as the European Union, because rupee internationalisation cannot be evaluated only through sanctions-sensitive or Global South corridors. The European Commission states that the EU is India’s third-largest trading partner, with goods trade worth €118 billion in 2025, representing 11.1 percent of India’s total trade, and that goods trade between the EU and India increased by 83.7 percent over the previous decade — EU Trade Relations with India – European Commission – 2026. The EEAS separately published an economic-footprint report assessing EU firms in India from 2014 to March 2024, covering trade, investment, employment, turnover, and regional patterns — Economic Footprint of EU Businesses in India – European External Action Service – April 2026. These official EU sources create a different analytic signal from the Russia channel. For Europe, the central question is not sanctions avoidance but settlement efficiency, compliance predictability, remittance cost, trade facilitation, and whether rupee-denominated instruments become attractive enough for firms operating inside India’s production ecosystem. A future TIPS–UPI linkage could reduce retail and remittance friction, but it does not automatically produce INR invoicing in EU–India goods trade, where euro and dollar habits, treasury-management standards, hedging practices, and corporate risk policies remain powerful. The five-year forecast therefore separates payment interoperability from invoice-currency substitution: India can plausibly make payment rails faster and cheaper with Europe before it meaningfully shifts invoice denomination toward INR at scale. This distinction is critical because many superficial de-dollarisation narratives confuse the ability to move money with the willingness to price contracts in a specific currency.

| Corridor type | Likely INR adoption driver | Counterparty incentive | Main limiting factor |

|---|---|---|---|

| Russia-linked strategic trade | Payment resilience under sanctions pressure | Continuity of energy, defence, commodities, and strategic flows | Rupee surplus recycling |

| Gulf and commodity corridors | India’s import demand and diaspora/remittance channels | Reduced conversion cost and faster settlement | Commodity pricing still often dollar-based |

| EU corridor | Trade scale, remittances, and payment interoperability | Lower payment friction and predictable access to Indian market | Corporate treasury preference for EUR/USD |

| China comparison | Lessons from RMB internationalisation | Demonstrates need for asset access and payment infrastructure | India’s more cautious capital-account posture |

| Global South corridors | South–South trade and payment redundancy | Reduced dependency on scarce hard currency | Shallow hedging and bank connectivity |

The seventh pillar is risk modelling, because settlement architecture produces sovereignty only when it survives adverse states of the world. A Monte Carlo-style 2026–2031 scenario model should treat four variables as dominant: T₁ trade-settlement adoption, L₂ rupee-liquidity recycling, C₃ capital-market and hedging depth, and G₄ geopolitical-fragmentation pressure. Under the baseline scenario, weighted here at 55 percent, India expands rupee settlement incrementally through SRVAs, SNRR accounts, selected national-currency corridors, and payment interoperability, but does not achieve broad international reserve-currency status. Under the acceleration scenario, weighted at 25 percent, geopolitical fragmentation and partner demand for payment redundancy increase rupee use in strategic imports, remittances, and bilateral trade, especially where India can offer market access or investment outlets. Under the bottleneck scenario, weighted at 15 percent, operational accounts exist but foreign counterparties resist large rupee accumulation because hedging, conversion, and recycling options remain insufficient. Under the stress-reversal scenario, weighted at 5 percent, a major external shock forces India to prioritise exchange-rate stability and domestic liquidity over internationalisation speed. The structural warning comes from the BIS and IMF macro-financial logic: payment innovation is useful, but currency internationalisation requires deep market confidence, financial-sector resilience, and cross-border liquidity mechanisms; the BIS speech by Michael Debabrata Patra frames India as a fast-growing major economy and discusses the need to future-ready monetary policy, while the IMF notes India’s resilience but also places the economy within external-headwind and financial-sector monitoring conditions — Future Readying India’s Monetary Policy – Bank for International Settlements – July 2024; India: 2025 Article IV Consultation – International Monetary Fund – November 2025. The crucial intelligence judgment is that India’s monetary sovereignty will increase even if the rupee does not become a major reserve currency, because sovereignty here means reducing compulsory exposure to external settlement chokepoints, not eliminating global currency hierarchy.

| Scenario | Probability estimate | Required enabling conditions | Early-warning indicators |

|---|---|---|---|

| Baseline controlled expansion | 55% | More SRVAs, broader permitted rupee recycling, moderate macro stability | Gradual increase in rupee invoicing, more bank-level operational guidance |

| Accelerated sovereignty corridor | 25% | Higher geopolitical fragmentation, commodity partners accept rupees, deeper Indian asset access | More national-currency statements, rupee use in energy and strategic imports |

| Recycling bottleneck | 15% | Trade imbalances generate unwanted rupee balances | Partner complaints, reduced repeat use, preference for dirham/euro/dollar netting |

| Stress-reversal | 5% | External shock pressures rupee and reserves | tighter capital controls, slower liberalisation, stronger intervention priority |

The eighth pillar is the shadow dimension, where formal account rules interact with mercenary dynamics, cyber-norm fragmentation, liquidity flows, and coercive financial infrastructure. In a narrow banking-law reading, SRVAs and SNRR accounts are technical devices; in an OSINT risk model, they are also resilience nodes in a fractured global settlement environment. Mercenary and defence-adjacent procurement networks matter because strategic goods often require payment continuity even when normal correspondent banking becomes politically risky; cyber-norm fragmentation matters because payment rails become critical infrastructure and require redundancy; liquidity flows matter because the real international role of a currency is measured by whether holders can deploy balances under stress; and sanctions risk matters because states and firms increasingly evaluate not only transaction cost but also transaction survivability. The Chinese official data point is relevant as a benchmark, not as a model to copy: China’s State Council reported that cross-border RMB payments and receipts in goods trade accounted for 26.5 percent of China’s total goods-trade settlement in local and foreign currencies in the first eight months of 2024, while services RMB use rose 22.3 percent year on year; this demonstrates that currency internationalisation requires repeated use across trade, services, commodities, investment, and bond holding, not merely bilateral declarations — Cross-Border RMB Use Up Over 20 Percent – State Council of the People’s Republic of China – October 2024. India’s five-year target should therefore be judged by corridor density, not headline count: more meaningful than the number of countries willing to discuss rupee settlement is the share of recurring invoices, the volume of surplus rupees productively recycled, the spread between onshore and offshore hedging costs, the number of banks operationally comfortable with SRVA compliance, and the degree to which CBDC, UPI, and conventional banking layers can interoperate without creating settlement-finality ambiguity. The intelligence conclusion is sober but strategically significant: India can obtain measurable monetary-sovereignty gains by 2031 without achieving full currency internationalisation, provided it turns rupee settlement from a diplomatic option into a repeatable liquidity circuit.

Figure 1: 5-Year INR Settlement Sovereignty Projection

Scenario-weighted analytical projection for India’s rupee settlement architecture, calibrated to verified institutional mechanisms: SRVA, SNRR, CBDC sandbox experimentation, bilateral national-currency channels, and payment-system interoperability.

Liquidity, Convertibility, and Market-Depth Constraints: INR Internationalisation 2026–2031

India’s growth scale materially improves the strategic case for INR expansion, but it does not remove the binding monetary constraints that separate transactional internationalisation from durable international currency status. The strongest support variable is macroeconomic scale: India is now large enough, trade-connected enough, and financially deep enough to make rupee settlement useful to foreign banks, exporters, commodity suppliers, portfolio investors, remittance intermediaries, and regional payment corridors. The IMF states that India’s financial and corporate sectors remained resilient, supported by adequate capital buffers and multi-year low non-performing assets, while the current-account deficit remained contained and services exports supported external resilience — India: 2025 Article IV Consultation – International Monetary Fund – November 2025 — India: 2025 Article IV Consultation. That evidence raises the Bayesian probability of H₁, controlled INR transactional deepening, because foreign counterparties are more likely to accept a currency issued by an economy with durable growth, banking stability, and external buffers. However, the same evidence does not validate H₂, rapid reserve-currency substitution, because the international use of a currency depends on the liquidity of the issuer’s financial markets, the convertibility of its capital account, the availability of hedging instruments, and the ability of foreign holders to recycle balances into deep, safe, tradeable assets. The Reserve Bank of India defines international trade settlement in INR as an additional arrangement that reduces dependence on hard currency but operates alongside existing freely convertible-currency systems, which means India’s current architecture is a complement to dollar/euro settlement, not a replacement for global hard-currency liquidity — International Trade Settlement in Indian Rupees – Reserve Bank of India – April 2026 — International Trade Settlement in Indian Rupees. The strategic conclusion is therefore precise: India’s growth gives the INR transactional gravity, but liquidity, convertibility, hedging depth, bond absorption, and external-balance volatility determine whether that gravity becomes an investable currency ecosystem or remains a controlled settlement corridor.

| Constraint layer | Why it matters for INR expansion | Current support factor | Binding risk variable | 2026–2031 intelligence judgment |

|---|---|---|---|---|

| Liquidity depth | Foreign users must enter and exit rupee positions without large price impact | Larger economy, wider banking system, expanding payment rails | Shallow stress-period liquidity and fragmented market depth | Gradual improvement, not full global liquidity parity |

| Capital-account management | Foreign holders need usable pathways into assets and outflows | Controlled liberalisation limits crisis vulnerability | Excess openness can amplify volatile flows | Policy will remain cautious by design |

| Hedging depth | Investors and traders need forwards, swaps, and derivatives to manage INR risk | Onshore/offshore markets are evolving | Hedging cost and availability constrain adoption | Central bottleneck for international scale |

| Bond-market absorption | Foreign rupee balances require safe, liquid rupee assets | G-sec market benefits from index inclusion and domestic base | Foreign outflow sensitivity and duration risk | Stronger by 2031 but stress-tested by global risk cycles |

| External-balance volatility | Current-account and capital-flow shocks affect currency confidence | Reserves and services exports provide buffers | Oil prices, global dollar cycle, portfolio reversals | Manageable, but not irrelevant |

The first hard constraint is liquidity, because an internationalising currency is not defined merely by legal permission to invoice or settle in that currency; it is defined by whether the currency can be bought, sold, hedged, invested, and liquidated at scale without destabilising spreads, yields, or exchange rates. In a settlement corridor, liquidity means banks can process trade payments; in an international currency ecosystem, liquidity means foreign asset managers, commodity suppliers, central banks, non-bank financial institutions, corporates, and trade-finance desks can hold rupee exposures without fearing trapped balances or disorderly exits. The BIS shows why this distinction matters for emerging-market debt markets: it states that the investor base and the size of hedging markets affect liquidity and resilience in emerging-market government debt markets, that domestic banks can stabilise liquidity during stress, and that deeper hedging markets help markets withstand shocks — Towards Liquid and Resilient Government Debt Markets in EMEs – Bank for International Settlements – March 2024 — Towards liquid and resilient government debt markets in EMEs. This directly applies to India because the INR can expand only if counterparties can recycle rupees into reliable instruments and manage mark-to-market risk. A large domestic investor base is a stabiliser, but an excessive dependence on domestic absorption can also limit foreign confidence if international users believe the market is deep only under normal conditions. The Bayesian update here is mixed: India’s banking depth and domestic savings base raise the probability of a resilient rupee market, while the structural evidence from the BIS lowers the probability of rapid international liquidity expansion unless hedging markets mature in parallel. The key intelligence dependency is L₂, the rupee liquidity-recycling variable: if foreign holders can use rupees to buy Indian exports, invest in government securities, hedge exchange-rate exposure, finance Indian operations, or settle with third parties, the rupee becomes functional; if those options remain narrow, INR acceptance remains tactical.

INR Liquidity-Recycling Chain

Bilateral transaction telemetry mapping the capital pathways, structural recycling feedback loops, and secondary fallback risk vectors of local currency invoicing.

Foreign Exporter Receives INR

OPERATIONAL CONDITION

Bilateral trade settlements successfully clear through the foreign partner bank’s Special Rupee Vostro Account (SRVA), leaving the non-resident counterparty with a long position in onshore Indian Rupees.

Active Recycling Engine

PERMITTED CAPITAL ROUTING

MACROECONOMIC TRANSCRIPTION

Efficient redeployment creates an active domestic velocity model. This reduces overall capital-account conversion volatility and locks in multi-cycle preference for local invoicing structures.

Weak Recycling Bottlenecks

Trapped Balances: Liquidity accumulates inside locked, non-convertible offshore clearing frameworks.

Wider Risk Premium: Counterparties demand asymmetric pricing adjustments to offset conversion friction.

Lower Invoicing Preference: Active market participants systematically reduce operational exposure to INR terms.

Exogenous Currency Reversion

SYSTEMIC RETRACTION BASES

STRATEGIC TRAJECTORY ANALYSIS

If asset deployment paths remain constrained, trade structures automatically fall back to traditional sovereign networks or liquid regional reserve variants, interrupting internationalization plans.

The second constraint is capital-account management, because India’s internationalisation strategy is intentionally not a full convertibility shock. A fully open capital account could increase foreign demand for rupee assets in the short term, but it could also import global risk aversion, dollar-cycle pressure, sudden stops, non-bank leverage, and exchange-rate overshooting into the domestic system. The BIS 2026 EME capital-flow volume states that emerging-market economies face an evolving global financial landscape shaped by structural changes in capital-flow and exchange-rate dynamics, resident outflows, local-currency financing, and the growing role of non-bank financial institutions in gross portfolio inflows and outflows — Capital Flows, Exchange Rates and Financial Conditions in EMEs in an Evolving International Monetary System – Bank for International Settlements – May 2026 — Capital flows, exchange rates and financial conditions in EMEs. This matters because India’s policy problem is not whether international rupee use is desirable in abstract terms; it is whether the marginal sovereignty gained from foreign rupee use exceeds the marginal instability created by more mobile capital. The RBI framework for SNRR accounts shows the same philosophy in operational form: non-resident rupee accounts are permitted for specified transactions in trade, foreign investment, external commercial borrowing, and related uses, while authorised dealer banks must identify counterparties and comply with regulated procedures — Special Non-Resident Rupee Accounts – Reserve Bank of India – January 2025 — Special Non-Resident Rupee Accounts. The architecture is therefore a controlled membrane, not an open floodgate. In ACH terms, H₁ says controlled liberalisation lets India internationalise safely; H₂ says controlled liberalisation slows foreign adoption; H₃ says full openness would deepen markets; H₄ says full openness would raise crisis probability; H₅ says selective corridor-based openness creates the best risk-adjusted path. The posterior favours H₅: India’s optimal strategy over 2026–2031 is not maximal convertibility but calibrated convertibility, with more account functionality, wider investment access, and better hedging infrastructure, while avoiding a destabilising external balance-sheet shock.

| ACH framework | Convertibility proposition | Probability weight | Evidence signal | Policy implication |

|---|---|---|---|---|

| H₁ controlled liberalisation succeeds | India deepens rupee use without exposing the system to uncontrolled flows | 40% | SNRR, SRVA, bond-index inflows, resilient banking | Most likely path |

| H₂ regulation suppresses adoption | Foreign users prefer more convertible currencies | 20% | Counterparties need flexible exit routes | Requires wider asset recycling |

| H₃ full openness accelerates internationalisation | Foreign demand rises if restrictions fall quickly | 10% | Theoretical liquidity benefit | High instability cost |

| H₄ full openness amplifies shocks | Global risk cycles transmit faster into India | 20% | BIS EME capital-flow evidence | Supports caution |

| H₅ corridor-based openness dominates | India opens where trade/payment gains exceed volatility costs | 10% | Consistent with RBI architecture | Expand selectively |

The third constraint is hedging depth, which is the most underestimated technical variable in popular discussions of rupee internationalisation. A foreign company may accept rupee invoicing for political, commercial, or cost reasons, but if it cannot hedge rupee exposure at acceptable cost and tenor, it will embed a risk premium into pricing or avoid the currency entirely. Likewise, a foreign portfolio investor may buy rupee government securities after global bond-index inclusion, but if the investor cannot hedge currency and duration risk efficiently, the investment remains vulnerable to global dollar cycles and redemption shocks. The BIS finds that the US dollar has a powerful role in driving local-currency bond and equity flows to emerging markets, and that a stronger dollar reduces foreign investment in local-currency assets through investor balance-sheet and risk-appetite channels — The US Dollar and Capital Flows to EMEs – Bank for International Settlements – September 2024 — The US dollar and capital flows to EMEs. This is decisive for India because the INR cannot be assessed only against India’s domestic fundamentals; it must also be assessed against the global dollar cycle, volatility regimes, fund-flow mandates, and treasury-risk models. Hedging depth affects three layers at once: trade settlement, because exporters need to lock exchange values; bond-market absorption, because foreign investors need to manage currency risk; and financial-centre credibility, because offshore/onshore basis spreads signal whether the rupee is operationally convenient. A five-year Monte Carlo model should therefore treat H₃ hedging capacity as a multiplier rather than a standalone variable: when hedging depth improves, the same level of trade and bond demand produces more durable INR use; when hedging is shallow or expensive, even strong growth fails to create full currency preference. The shadow dimension is liquidity under stress: a market can appear deep in peacetime, but the decisive test is whether bid-ask spreads, forward premia, swap availability, and counterparty balance sheets remain functional during global risk-off shocks, energy-price spikes, or sudden portfolio withdrawals.

| Hedging channel | Role in INR internationalisation | Failure mode | 5-year monitoring indicator |

|---|---|---|---|

| FX forwards | Allows exporters/importers to lock exchange values | High cost or limited tenor discourages rupee invoicing | Forward premia, tenor availability, corporate usage |

| Currency swaps | Supports institutional balance-sheet management | Counterparty limits during stress | Swap-market depth and basis volatility |

| Interest-rate derivatives | Helps manage bond duration risk | Weak liquidity limits foreign bond appetite | IRS volumes, bid-ask spreads, benchmark reliability |

| Onshore/offshore arbitrage | Aligns global rupee pricing | Persistent basis gaps signal fragmentation | NDF/onshore spread behaviour |

| Bank balance-sheet capacity | Enables market-making | Stress-period retreat widens spreads | Dealer inventories and liquidity provision |

The fourth constraint is bond-market absorption, because rupee internationalisation requires a safe, scalable rupee asset pool into which foreign holders can place balances. In practice, that means Indian government securities, high-grade corporate bonds, money-market instruments, and eventually more sophisticated repo and derivatives markets. India has a large sovereign securities market, and official evidence shows it is becoming more connected to global portfolios. The Department of Economic Affairs reported that during FY26 the Indian G-sec market was shaped by an accommodative monetary-policy environment and the positive effects of India’s inclusion in global bond indices, while lower inflation, liquidity injections, and periodic foreign portfolio inflows helped influence market conditions — Monthly Economic Review – Department of Economic Affairs, Government of India – May 2026 — Monthly Economic Review May 2026. The Department of Economic Affairs also reported that net market borrowings through dated securities stood at ₹11,80,458 crore in FY2023–24, compared with ₹11,08,260 crore in FY2022–23, confirming that India’s sovereign market has meaningful issuance scale — Status Paper on Government Debt for 2023–24 – Department of Economic Affairs, Government of India – November 2025 — Status Paper on Government Debt for 2023–24. Yet issuance scale is not the same as international absorption capacity. The BIS stresses that foreign investor participation can increase market liquidity and depth, but also exposes markets to global risk factors and adverse spillovers if the domestic investor base cannot absorb foreign sales during stress — Towards Liquid and Resilient Government Debt Markets in EMEs – Bank for International Settlements – March 2024 — Towards liquid and resilient government debt markets in EMEs. India’s bond-market path therefore has a dual character: global index inclusion and larger foreign participation can help transform rupee balances into investable assets, but the same mechanism introduces a new sensitivity to dollar strength, benchmark rebalancing, passive-flow mechanics, and global duration shocks.

INR Trade Execution Chokepoints

Stochastic breakdown of transactional structural drag, bilateral pricing asymmetries, and liquidity velocity constraints within local currency settlement mechanisms.

Regulatory & AD Compliance Drag

IDENTIFIED STRUCTURAL BLOCKAGES

OPERATIONAL ANALYSIS

Authorised Dealer Banks experience processing bottlenecks due to fragmented data layers and strict Reserve Bank compliance mandates. This increases transaction clear times compared to automated SWIFT alternatives.

Bilateral FX Pricing Asymmetry

IDENTIFIED STRUCTURAL BLOCKAGES

OPERATIONAL ANALYSIS

Because direct non-USD exchange pairs lack market depth, banks route conversions through synthetic intermediate paths. This creates pricing anomalies and forces non-resident exporters to absorb wide bid-ask spreads.

Velocity & Secondary Liquidity Constraints

IDENTIFIED STRUCTURAL BLOCKAGES

OPERATIONAL ANALYSIS

Bilateral balances are trapped inside separate Vostro accounts without an integrated domestic or international interbank market. This division limits capital velocity and blocks cross-account settlement optimization.

Capital Reinvestment Limits

IDENTIFIED STRUCTURAL BLOCKAGES

OPERATIONAL ANALYSIS

Foreign partner banks faces limits on short-term liquid instruments. When surplus balances cannot find high-yield onshore placement paths, they linger as idle cash, lowering long-term system utility.

The fifth constraint is external-balance volatility, because the international appeal of the rupee depends not only on India’s growth rate but on the perceived stability of its balance of payments, reserves, oil-import exposure, services-export durability, remittance flows, and capital-flow composition. India’s external buffer is substantial: the Economic Survey reported that foreign-exchange reserves stood at USD 640.3 billion at the end of December 2024, covering approximately 90 percent of external debt of USD 711.8 billion as of September 2024, and that import cover stood at 10.9 months, far above the IMF three-month rule-of-thumb threshold cited in the same official chapter — External Sector: Getting FDI Right – Government of India Economic Survey 2024–25 – January 2025 — External Sector: Getting FDI Right. The 2025–26 Economic Survey defines the balance of payments as a consolidated record of India’s transactions with the rest of the world, capturing current-account and capital-account developments, which is analytically important because rupee internationalisation operates across both sides of that ledger: trade invoicing affects the current account’s settlement currency, while portfolio inflows and non-resident rupee holdings affect the capital account — External Sector: Playing the Long Game – Government of India Economic Survey 2025–26 – January 2026 — External Sector: Playing the Long Game. Strong reserves reduce crisis probability, but they do not eliminate volatility. India remains exposed to commodity-import bills, global shipping and insurance costs, dollar-cycle liquidity, risk-off portfolio reversals, and geopolitical shocks that can move oil, gold, and capital flows simultaneously. The analytical trap is to treat reserves as proof that internationalisation can accelerate without cost. In reality, reserves are a buffer that allows controlled internationalisation, not a license for uncontrolled convertibility. Bayesian updating gives high confidence to H₁, resilience-backed gradualisation, but only moderate confidence to H₂, broad foreign balance-sheet preference, because foreign holders still ask whether rupee exposure remains liquid and hedgeable when external conditions deteriorate.

The sixth constraint is geopolitical comparison, especially against RMB, EUR, and Russia-linked national-currency settlement. China’s official account shows that RMB internationalisation is treated as a full financial-architecture project, not merely an invoicing campaign: the People’s Bank of China said it would promote RMB use in cross-border payments, pricing, investment, and financing, develop offshore RMB markets, use currency swaps and clearing banks, and reinforce Shanghai and Hong Kong’s financial-centre roles — China’s Central Bank to Promote Cross-Border RMB Use – State Council of the People’s Republic of China – February 2025 — China’s central bank to promote cross-border RMB use. That source is critical for India because it demonstrates the institutional sequence required for currency internationalisation: payment use must be paired with offshore liquidity, asset-market access, swaps, clearing-bank capacity, and financial-centre depth. The EU comparison highlights another constraint: the European Commission states that the EU is India’s third-largest trading partner, with goods trade worth €118 billion in 2025, 11.1 percent of India’s total trade, services trade of €67 billion in 2024, and EU FDI stock in India of €132.8 billion in 2024 — EU Trade Relations with India – European Commission – 2026 — EU trade relations with India. Large trade scale supports the possibility of more rupee usage, but European corporate treasury systems, euro-zone settlement habits, and global USD/EUR liquidity still limit near-term rupee invoicing. The Russian vector provides a different stress case: the Kremlin’s official 2024 India–Russia joint statement said the two sides agreed to continue working together to promote a bilateral settlement system using national currencies — Joint Statement Following the 22nd India–Russia Annual Summit – Kremlin – July 2024 — Joint Statement following the 22nd India-Russia Annual Summit. That official signal supports the geopolitical logic of non-dollar settlement, but it also exposes the balance-recycling problem: national-currency settlement becomes durable only when both sides can reuse accumulated balances at scale.

| External corridor | Supports INR expansion through | Limits INR expansion through | Strategic reading |

|---|---|---|---|

| China / RMB benchmark | Demonstrates full-stack currency internationalisation logic | Shows how hard offshore liquidity and asset depth are to build | India needs architecture, not slogans |

| EU / EUR corridor | Large trade, investment, remittance, and payment-system interface | Treasury preference for EUR/USD, compliance complexity | Payment interoperability may precede INR invoicing |

| Russia / national-currency corridor | Strategic pressure to avoid hard-currency chokepoints | Imbalanced trade and surplus-recycling constraints | Useful stress laboratory, not universal model |

| BIS EME framework | Confirms need for deep investor and hedging base | Warns of foreign-flow shock transmission | Supports calibrated liberalisation |

| IMF India macro frame | Confirms resilience and contained external deficit | External headwinds still relevant | Supports gradualism over forced acceleration |

The seventh constraint is the distinction between payment interoperability and market-depth internationalisation. India can make cross-border payments faster without making the rupee a deeply held international asset; it can expand UPI corridors without forcing foreign reserve managers into INR; it can test CBDC and tokenised settlement without proving that offshore investors will hold rupee bonds through a dollar shock. The European Central Bank stated that the Eurosystem decided to advance work to interlink TIPS with India’s UPI, begin the realisation phase while completing legal and technical implementation, and continue exploring a potential connection to Nexus Global Payments; the same ECB release states that UPI is regulated by the RBI and that India is among the top ten recipients of euro-area remittances — Eurosystem Moves Forward on Work to Connect TIPS with India’s Unified Payments Interface and with Nexus Global Payments – European Central Bank – November 2025 — Eurosystem moves forward on work to connect TIPS with India’s UPI and Nexus. This is a major payment-architecture signal, but the analytical interpretation must stay disciplined: faster retail and remittance rails reduce transaction friction, improve transparency, and increase India’s infrastructural relevance, yet they do not automatically deepen the government bond market, lower hedging costs, or liberalise the capital account. The 2026–2031 forecast should therefore separate P₁ payment reach from M₂ market depth. P₁ is likely to improve quickly because digital payment interoperability can be negotiated corridor by corridor. M₂ will improve more slowly because it requires legal certainty, accounting familiarity, derivatives liquidity, repo-market depth, foreign investor onboarding, custodial reliability, benchmark inclusion, domestic absorption, and central-bank comfort with volatility. The intelligence judgment is that India’s rupee internationalisation will look technologically advanced before it looks financially deep: the payments layer may globalise faster than the asset layer, creating visible progress but also the risk of exaggerated narratives.

Payments Versus Market Depth

A comparative structural assessment of retail layer connectivity versus capital-account macroeconomic liquidity thresholds.

Payment Linkage Internationalisation

INTEGRATED INTERFACES & RAILS

SYSTEMIC IMPACTS

Drives immediate operational efficiencies by lowering retail remittance fees and small-value transaction friction. Expands cross-border retail processing access nodes rapidly across allied regional targets.

The Structural Disparity Break

Core Strategic Dissonance: Seamless digital interface connectivity at the consumer level does not automatically establish or scale wholesale global institutional trust, deep asset holdings, or sovereign reserves.

MACRO ARCHITECTURAL WARNING

Payment infrastructure internationalisation can run far ahead of genuine sovereign currency internationalisation, masking fundamental vulnerabilities in underlying bond market architecture and macroeconomic capital mobility.

Sovereign Macro Currency Depth

CORE INSTITUTIONAL FOUNDATIONS

SYSTEMIC IMPACTS

Forms the foundation for long-term global reserve allocation. Provides foreign central banks and institutional funds with the depth required to absorb heavy balance-of-payments shocks without triggering domestic asset price drops.

The five-year scenario model therefore assigns the highest probability to controlled market-deepening rather than full convertibility. In the baseline path, probability 55 percent, India’s growth, reserves, bond-index integration, payment-linkage expansion, and controlled account architecture support greater INR use in settlement, portfolio allocation, and regional payment corridors, but capital-account management remains restrictive enough to prevent a sudden open-market transformation. In the acceleration path, probability 20 percent, global fragmentation, dollar volatility, and strategic trade pressures increase foreign willingness to hold rupees, while India expands rupee asset access and hedging markets faster than expected. In the bottleneck path, probability 20 percent, rupee settlement grows legally but remains shallow economically because foreign counterparties cannot recycle balances, hedge cheaply, or absorb duration and currency risk. In the stress path, probability 5 percent, an oil-price shock, dollar surge, or portfolio outflow cycle forces India to defend stability, slowing convertibility steps and prioritising reserve management. The Bayesian posterior after official-source review is clear: India’s growth scale is sufficient to justify INR expansion, but not sufficient to guarantee it. The necessary condition is growth; the sufficient condition is a liquidity complex composed of deep government securities, reliable hedging, controlled but useful convertibility, resilient domestic absorption, and external-balance credibility. The policy problem is not “internationalise or do not internationalise”; it is how to sequence internationalisation so that every additional rupee held abroad has somewhere safe, liquid, compliant, and economically useful to go. India’s strongest strategy is therefore calibrated thickening: expand SRVA and SNRR functionality, deepen bond and derivatives markets, preserve reserve buffers, build payment corridors, and let foreign adoption follow market usability rather than forcing premature convertibility.

Figure 1: 5-Year INR Market-Depth Constraint Projection

Scenario-weighted projection of the limiting variables shaping INR internationalisation: liquidity recycling, convertibility caution, hedging depth, bond-market absorption, and external-balance volatility. Values are analytical indices, not official statistical series.

Geopolitical Shock Channels and 5-Year Scenarios: INR Internationalisation 2026–2031

India’s INR internationalisation perimeter will be shaped less by abstract “de-dollarisation” ideology than by concrete shock channels: sanctions pressure around Russia-linked trade, the UAE as a high-liquidity settlement and energy-remittance hub, Africa’s search for cheaper cross-border payment infrastructure, Europe’s large trade exposure but high compliance discipline, China’s full-stack RMB internationalisation playbook, oil-price volatility, and the fragmentation of global payment networks into interoperable, partially sovereign, and politically screened rails. The analytical baseline is that India’s rupee will not become a global reserve substitute by 2031, but it can become a more important corridor currency where counterparties face dollar scarcity, sanction-contingency planning, remittance friction, high energy-import volumes, or strategic interest in India’s domestic demand. The official evidence supports this controlled-perimeter interpretation: India and Russia agreed to continue work on a bilateral settlement system using national currencies — Joint Statement Following the 22nd India–Russia Annual Summit – Kremlin – July 2024 — Joint Statement following the 22nd India-Russia Annual Summit; India and the UAE established a Local Currency Settlement mechanism to promote INR–AED cross-border transactions, with India’s Ministry of External Affairs reporting that trade transactions in gold, crude oil, and food products had already occurred in local currencies — India-UAE Bilateral Relations – Ministry of External Affairs, Government of India – March 2025 — India-UAE Bilateral Relations; and the BIS describes Project Nexus as a model for connecting instant payment systems so that cross-border payments can occur within 60 seconds in most cases — Project Nexus: Enabling Instant Cross-Border Payments – Bank for International Settlements – August 2025 — Project Nexus. These three verified pillars define India’s perimeter: national-currency settlement in strategic trade, Gulf-linked liquidity and remittance utility, and interoperable payment infrastructure that can reduce transaction friction without requiring full capital-account convertibility.

| Geopolitical channel | INR internationalisation effect | Official-source signal | Five-year constraint |

|---|---|---|---|

| Russia | Raises demand for non-dollar settlement under sanctions pressure | India–Russia national-currency settlement language | Rupee surplus recycling and secondary-sanctions sensitivity |

| UAE | Provides INR–AED liquidity bridge, energy trade, gold, diaspora remittances | LCS MoU and local-currency transactions reported by India | Commodity pricing habits and compliance risk |

| Africa | Creates demand for cheaper cross-border settlement and local-currency payment models | India–Africa trade scale and PAPSS payment-infrastructure logic | Fragmented currencies, shallow FX markets, bank connectivity |

| EU | High trade and investment exposure but stricter compliance environment | EU–India goods/services trade and FDI data | Corporate treasury preference for EUR/USD |

| China / RMB | Offers institutional playbook for currency internationalisation | PBOC cross-border RMB agenda | India will not copy China’s capital-control/offshore-market model exactly |

| Energy pricing | Makes settlement sovereignty strategically valuable | India’s crude-import dependency and Russian crude-source shock | Oil remains globally dollar-referenced |

| Payment fragmentation | Makes alternative rails valuable | FSB/BIS cross-border payment roadmap and interoperability agenda | Fragmented standards can raise costs if not harmonised |