")

Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

Executive Summary (BLUF)

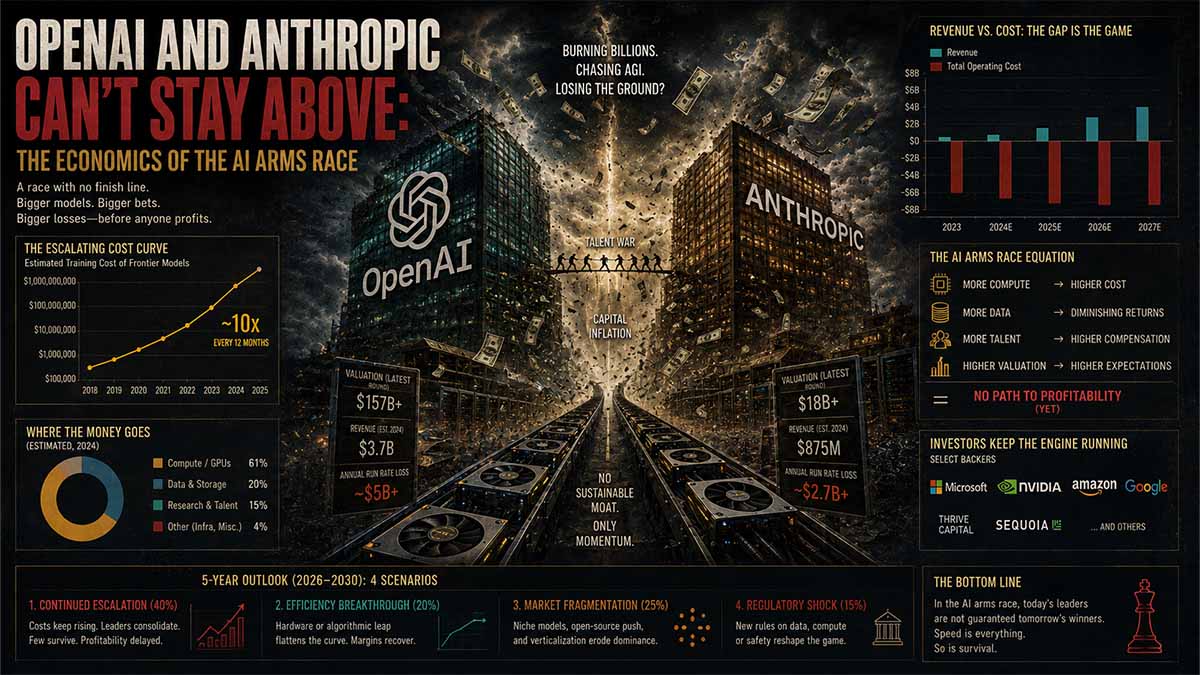

- OpenAI burned $3.7 billion in the first quarter of 2026, more than half its $5.7 billion in revenue, with both figures roughly tripling year-over-year. FortuneWhere’s Your Ed At

- OpenAI’s 2025 net loss reached approximately $38.5 billion, against revenue that rose from $3.7 billion in 2024 to $13.07 billion in 2025. SaaStrAIInvesting.com

- Full-year 2026 cash burn is now projected at roughly $27 billion, rising to approximately $63 billion in 2027, with OpenAI not expected to reach cash-flow positive before 2030. PYMNTS.comPYMNTS.com

- Microsoft’s revenue-share claim on OpenAI is capped at roughly $38 billion through 2030, while Microsoft retains rights to resell OpenAI’s models through 2032. PYMNTS.com

- OpenAI has confidentially filed with the SEC for an IPO targeting a valuation above $1 trillion, with a listing possibly as early as September 2026. PYMNTS.comWhere’s Your Ed At

- Anthropic, by contrast, has grown revenue from roughly $9 billion at the end of 2025 to a $30 billion annualized run rate by April 2026, and Sacra estimates it reached approximately $45 billion ARR by May 2026. ForbesVentureBeat

- Anthropic still projects a roughly $14 billion loss for 2026, but forecasts $70 billion in revenue and $17 billion in positive cash flow by 2028 — sources diverge on the exact breakeven year (2027–2029 depending on the report), which is flagged below. SacraSingularity Moments

- Anthropic filed confidentially for its own IPO at a $965 billion valuation on June 1, 2026, following a $65 billion Series H round. VentureBeat

Bottom line: neither company is self-sufficient on its own revenue. Both are structurally dependent on external capital — equity investors, cloud partners, and in OpenAI’s case a commercial partner with contractual claims on future revenue. The difference is trajectory: Anthropic’s enterprise-weighted model is closing the profitability gap faster than OpenAI’s consumer-weighted model.

Who’s Paying the Bill for AI — How OpenAI and Anthropic Burn Billions Waiting for Profit

Imagine a company that grosses nearly six billion dollars in the first three months of the year and spends nearly four billion just to stay afloat. It’s not a struggling startup: it’s OpenAI, the company that made ChatGPT a daily buzzword for hundreds of millions of people. And its story, in recent months, has become increasingly intertwined with that of its fiercest rival, Anthropic, creator of Claude — both poised to go public with valuations approaching a trillion dollars, both still unable to stand on their own two feet.

This is the paradox at the heart of generative AI in 2026: the two companies that are literally rewriting the way we work, write, and program, aren’t generating enough revenue to cover the costs they incur to stay at the forefront of the technology. And the better they are, the higher the bill.

A Widening, But Slowly Growing, Hole

OpenAI’s numbers tell a story of dizzying growth and equally dizzying losses. In the first quarter of 2026, the company generated $5.7 billion in revenue, burning $3.7 billion just to operate—more than half of its revenue. 2025 as a whole closed with an estimated net loss of around $38.5 billion, nearly eight times that of the previous year, against revenues that rose from $3.7 billion to just over $13 billion. Yet, hidden within these dramatic numbers is a less negative signal than it seems: in 2024, OpenAI spent $2.37 for every dollar it earned; in 2025, that ratio dropped to $1.60. The company is losing less, proportionately, than it did a year earlier—even though the losses have increased in absolute terms.

According to the most recent projections, OpenAI’s cash burn will reach nearly $27 billion in 2026, rising to approximately $63 billion in 2027. True cash breakeven isn’t expected before 2030. In the meantime, the company can count on a significant cushion: over $73 billion in cash and liquid assets at the end of the first quarter, nearly double the level at the end of December, thanks to a large financing round closed in March.

The Marriage with Microsoft, Rewritten Three Times in Eighteen Months

To truly understand OpenAI’s financial dependence, one must examine its relationship with Microsoft, which has been its primary funder and cloud infrastructure provider since 2019. That relationship has been rewritten several times over the past eighteen months, and each rewrite reveals something about the company’s true health.

In October 2025, OpenAI transformed into a public benefit corporation, retaining control of a nonprofit foundation but opening the door to new investors. Microsoft retained a stake of approximately 27%, then valued at $135 billion, and waived its right of first refusal as the exclusive provider of computing power.

Then, on April 27, 2026, came the most significant turning point: the two companies rewrote the agreement, eliminating cloud exclusivity—OpenAI can now also serve its models via Amazon Web Services or Google Cloud—and, most importantly, eliminating the so-called AGI clause, which tied Microsoft’s rights to OpenAI’s intellectual property to the theoretical and never precisely defined achievement of artificial general intelligence. In its place, a simpler and more predictable agreement: Microsoft will continue to collect a share of OpenAI’s revenues until 2030, with an overall cap calculated—according to the most recent reconstructions—not only on revenues generated through Azure but on the company’s entire revenues, wherever they are generated. In exchange, it maintains a license to OpenAI’s technology until 2032, two years beyond the revenue-sharing expiration.

The day after the announcement, on April 28, OpenAI’s models were already available on Amazon Bedrock. This timing speaks volumes: the deal with Microsoft wasn’t so much a breakup as it was a matter of accounting maintenance, useful for presenting future stock market investors with a more readable balance sheet.

The day after the announcement, on April 28, OpenAI’s models were already available on Amazon Bedrock. This timing speaks volumes: the deal with Microsoft wasn’t so much a disruption as accounting maintenance, useful for presenting future stock market investors with a more readable balance sheet.

Anthropic is growing faster, but its financials remain a point of contention

If OpenAI tells a story of slowly decreasing losses, Anthropic depicts a nearly vertical trajectory. Annualized revenues rose from approximately $87 million in January 2024 to $1 billion by December of the same year, $9 billion by the end of 2025, and $30 billion by April 2026—with some more recent estimates already placing them above $45 billion in May. This growth rate, according to several analysts, is unprecedented in the history of enterprise software: Salesforce took twenty years to reach $30 billion in annual revenues; Anthropic did so in less than three.

The substantial difference compared to OpenAI lies in its customer base. Approximately 85% of Anthropic’s revenue comes from companies that pay for their models via APIs, not from consumer subscriptions—and this generates higher margins and more stable customers. Eight of the top ten Fortune 500 companies are Claude customers, and over five hundred companies spend more than $1 million annually on the platform.

But here the picture gets complicated, and it’s fair to say so with the same honesty with which data is presented when it’s favorable. Anthropic announced that it expects its first operating profit quarter—approximately $559 million in profit on $10.9 billion in revenue in the second quarter of 2026—two years earlier than it had disclosed to investors just a year earlier. Some independent analysts, including financial journalist Ed Zitron, have raised concrete concerns: that result would coincide precisely with a temporary discount on a $1.25 billion-per-month computing contract signed with SpaceX, a discount that—critics argue—artificially inflates the margin in the most-cited quarter. OpenAI has also publicly questioned Anthropic’s revenue calculation methodology, arguing that actual revenue is closer to $22 billion than the reported $30 billion, because Anthropic also counts sales from cloud providers as gross revenue. Anthropic, for its part, has informed investors that this profitability may not be repeated in subsequent quarters, given its planned spending on new computing capacity—a level of transparency few observers expected from such a major announcement.

Who’s really keeping these giants afloat?

Behind both companies, however, lies a deeper reality: neither is standing on its own. Both depend on a web of capital that, in recent months, has begun to worry financial analysts. These are called circular agreements: large infrastructure providers—Microsoft, Amazon, Google, Nvidia—invest capital in AI companies, which in turn spend that same capital to purchase computing power from the same investors. Nvidia committed $30 billion to OpenAI’s latest round and $10 billion to Anthropic; Microsoft and Nvidia together invested $15 billion in Anthropic, which has committed to spending $30 billion on Azure. According to an estimate cited by PitchBook, OpenAI’s total infrastructure commitments to Oracle, Microsoft, and Amazon exceed $1.15 trillion—more than forty times the company’s current annualized revenue.

In March, Nvidia founder Jensen Huang stated that the recent direct investments in OpenAI and Anthropic would likely be his company’s last, citing the approaching IPOs. This explanation only partially convinced analysts, as investors typically increase, not reduce, their exposure in the run-up to a public offering. Other possibilities remain on the table: growing direct competition between Nvidia’s cloud services and the two AI companies, and geopolitical tensions related to the sale of high-performance semiconductors to sensitive markets.

Why it matters, and what to expect

There’s a question running through this whole story, and it’s the one that really matters to outsiders: who will take the risk when public markets, much more demanding than private ones, demand the numbers? The institutional investors who have so far financed the growth of OpenAI and Anthropic have agreed to wait, in exchange for specific contractual rights—shareholdings, technology licenses, and preferential revenue streams.

Those who buy shares upon their stock market debut, likely by the end of 2026, will find themselves last in line for collateral, in a sector where combined infrastructure spending by major tech companies has already exceeded $700 billion in 2026 alone.

This doesn’t mean the model is doomed to fail. It does mean that, for now, the race to AI rests on a fragile balance between real growth and borrowed capital—and that sooner or later, someone will have to foot the bill in full.

Navigational Index

- The Burn — OpenAI’s cost structure, losses, and the mechanics of its Microsoft dependency

- The Divergence — Anthropic’s enterprise economics and comparatively faster path to cash-flow breakeven

- The Reckoning — IPO pressure, investor expectations, and what “someone keeping them afloat” actually means

OpenAI vs. Anthropic — Burn, Revenue & Runway (FY2026)

Figures compiled from public reporting cited below. Toggle metrics to compare.

Chapter 1 — The Burn: OpenAI’s Cost Structure, Losses, and the Mechanics of Its Microsoft Dependency

1.1 The Q1 2026 Baseline

OpenAI’s first-quarter 2026 disclosures to shareholders, reported by The Information and corroborated by Reuters, showed revenue of $5.7 billion against cash burn of $3.7 billion — meaning the company spent roughly 65 cents for every dollar it took in during those three months alone, with both figures tripling year-over-year. Fortune’s review of leaked financial statements (obtained by independent analyst Ed Zitron and separately verified by the Financial Times) placed the Q1 net loss at approximately $21.3 billion, though roughly $12.4 billion of that was non-cash accounting charges tied to items like stock-based compensation; stripped of those, the operating loss still ran to about $9.3 billion for the quarter, with R&D spending alone hitting $8.6 billion.

| Metric | Q1 2025 (approx.) | Q1 2026 | Change |

|---|---|---|---|

| Revenue | ~$1.9B | $5.7B | ~3x |

| Cash burn | ~$1.2B | $3.7B | ~3x |

| Net loss (incl. non-cash) | — | ~$21.3B | — |

| Operating loss (cash basis) | — | ~$9.3B | — |

| R&D spend | — | $8.6B | — |

| Cash & marketable securities (period-end) | — | $73B | up from $40B end-Dec 2025 |

Sources: The Information, Fortune, Reuters via Investing.com

The full-year picture for 2025 is worse in absolute terms but better in trend. Net loss for the year came in at roughly $38.5 billion on $34 billion in total spending, against 2024’s loss of $5.09 billion — nearly an eightfold jump. Revenue over the same span rose from $3.7 billion (2024) to $13.07 billion (2025). The efficiency ratio — dollars spent per dollar earned — actually improved, from $2.37 spent per $1 of revenue in 2024 to $1.60 in 2025, which is the one genuinely positive signal in an otherwise deteriorating loss picture: the business is scaling revenue faster than it’s scaling waste, even if it isn’t yet scaling revenue faster than total cost.

Forward guidance has moved twice in recent months. The original internal forecast, cited across multiple outlets in June, projected $25 billion in 2026 cash burn, rising to $57 billion in 2027. Sacra’s more recent modeling, incorporating the April 2026 Microsoft renegotiation (detailed below), revises this to approximately $27 billion in 2026 and $63 billion in 2027 — the increase reflects roughly $6 billion in Microsoft payments now due this year under the new cap structure. Under either version, OpenAI is not projected to reach cash-flow positive before 2030.

1.2 The Microsoft Relationship: From Exclusive Compute Provider to Capped Revenue Claim

This is the load-bearing structural fact in OpenAI’s cost story, and it has moved three times in eighteen months.

Phase 1 — October 2025 recapitalization. OpenAI converted its for-profit arm into OpenAI Group PBC, with the nonprofit OpenAI Foundation retaining control and roughly 26% economic interest (~$130B at that valuation). Microsoft’s stake settled at approximately 27% (~$135B). As part of that restructuring, OpenAI committed to an incremental $250 billion in Azure spend, Microsoft gave up its right of first refusal as compute provider, and — critically — the two sides replaced OpenAI’s unilateral power to declare “AGI achieved” (which would have voided Microsoft’s IP license) with an independent-panel verification mechanism.

Phase 2 — April 27, 2026 amendment. Reported jointly on Microsoft’s and OpenAI’s blogs and confirmed by CNBC, Reuters, and Data Center Dynamics, this rewrite did four things simultaneously:

- Ended Azure exclusivity — OpenAI can now serve its models via AWS, Google Cloud, or any provider; Azure keeps “first ship” priority only where technically necessary.

- Removed the AGI termination clause entirely — no technical milestone now voids or renegotiates the deal. Both parties, per the Directions on Microsoft analysis, described this as making the arrangement “independent of OpenAI’s technology progress.”

- Capped OpenAI’s revenue-share payments to Microsoft at an undisclosed total ceiling, continuing through 2030. Notably, per follow-up reporting by The Information (via M.G. Siegler’s Spyglass), the 20% cut is calculated on OpenAI’s overall revenue — including revenue generated via AWS or Google Cloud — not just Azure-hosted revenue, which is the mechanism that justified capping the total in the first place.

- Extended Microsoft’s IP license to 2032 on a non-exclusive basis — meaning Microsoft can continue to access and resell OpenAI’s models for two years beyond the revenue-share window, even though it’s no longer the exclusive channel.

The commercial consequence arrived within 24 hours: OpenAI’s frontier models went live on Amazon Bedrock on April 28, 2026, one day after the amendment — timed, by most accounts, to precede a scheduled AWS event in San Francisco and to formalize the $50 billion investment Amazon made in OpenAI in February 2026, which included AWS becoming the exclusive third-party distributor for OpenAI’s enterprise “Frontier” platform.

Microsoft ⇄ OpenAI Dependency Architecture

Strategic Partnership & Decoupling Vector Timeline

Foundational Alliance Inception

- Microsoft executes an initial $1B capital investment venture.

- Establishes absolute exclusive cloud hosting and infrastructure compute partnership parameters.

PBC Recapitalization Event

- Microsoft equity holding adjusts to ~27% (~$135B valuation asset space).

- $250B multi-year Azure infrastructure capital allocation spend commitment formalized.

- AGI-Verification Panel introduced to oversee ultimate governance trigger mechanisms.

- Right of First Refusal (ROFR) parameters for structural infrastructure compute capacity officially dropped.

Amazon Infrastructure Expansion

- Amazon enters structural architecture with up to $50B ecosystem investment pool.

- AWS establishes deployment vector as an exclusive enterprise model distributor node.

Partnership Realignment Rewrite

- Exclusivity framework terminated, permitting runtime deployment across any standard cloud cluster network.

- AGI escape-clause framework cleanly expunged from primary corporate covenants.

- Revenue share architecture capped, extending operational runtime parameters up to 2030.

- Core IP deployment licensing terms extended with visibility boundaries reaching 2032.

AWS Bedrock Integration Live

- OpenAI flagship models systematically open native execution vectors inside the AWS Bedrock compute layer.

Confidential Public Capital Scaling

- OpenAI files high-security confidential registration metrics for an initial public offering (IPO).

- Ecosystem targets an absolute strategic public capitalization assessment threshold exceeding $1T.

Sources: CNBC, Data Center Dynamics, Directions on Microsoft, Spyglass

1.3 Reading the Dependency Correctly

The popular framing of the April amendment — “OpenAI breaks free of Microsoft” — is only half true, and the mechanics above show why. What OpenAI actually gained was infrastructure flexibility: the ability to route inference and enterprise sales through AWS, Google Cloud, or any future provider, which matters enormously given that OpenAI’s inference demand had outgrown what any single cloud could realistically serve. What Microsoft gave up was exclusivity, a real concession, but what it retained was arguably more valuable for a company facing an IPO with an uncertain path to profit: a predictable, capped, technology-agnostic revenue claim through 2030, plus a non-exclusive IP license through 2032 — an asset that survives even if OpenAI’s own cash position deteriorates or its governance changes again. Microsoft, in other words, converted an exclusivity-based dependency (valuable but legally fragile, as the 2023 board crisis demonstrated) into a claim-based dependency (less exclusive, but contractually cleaner and harder to unwind). Data Center Dynamics separately reported that Microsoft had been exploring legal action over the AWS deal’s compatibility with its prior exclusivity terms before the April rewrite resolved the dispute — evidence that this was a negotiated de-escalation, not a unilateral OpenAI win.

For the IPO narrative specifically, this matters. A prospectus carrying an undefined “AGI trigger” that could unilaterally void a multibillion-dollar commercial relationship would have drawn exactly the kind of underwriter scrutiny OpenAI can’t afford six months before a listing targeting a trillion-dollar-plus valuation. The April amendment reads, in that light, less as liberation from Microsoft and more as balance-sheet housekeeping ahead of public markets — trading a messier, contingent liability for a cleaner, quantifiable one that analysts can actually model.

Figure 1: OpenAI Cost Structure — Burn vs. Revenue, 2024–2027 (Projected)

Figure 1: OpenAI Cost Structure — Burn vs. Revenue, 2024–2027 (Projected). Sources: The Information, Fortune/FT, Sacra.

Chapter 2 — The Divergence: Anthropic’s Enterprise Economics and the Path to Breakeven

2.1 The Revenue Curve

Anthropic’s growth trajectory is, by a wide margin, the more extreme of the two companies’. Multiple independent sources converge on the same shape even where the exact numbers differ slightly: annualized run-rate revenue moved from roughly $87 million in January 2024 to $1 billion by December 2024, $9 billion by the end of 2025, $14 billion in February 2026, $19 billion in March, and $30 billion by April 2026. Sacra’s later estimate puts the figure at $45–47 billion ARR by May 2026, and a SemiAnalysis research note cited by BigGo Finance goes further still, claiming ARR “surged… to over $60 billion” by early June — a number no other outlet in this search corroborates independently, so it should be treated as the high end of a widening estimate range rather than a settled figure.

| Date | ARR (Annualized Run-Rate) | Source |

|---|---|---|

| Jan 2024 | ~$87M | VentureBeat |

| Dec 2024 | ~$1B | VentureBeat / SaaStr |

| Dec 2025 | ~$9B | Multiple |

| Feb 2026 | ~$14B | SaaStr |

| Mar 2026 | ~$19B | SaaStr |

| Apr 2026 | ~$30B | VentureBeat, SaaStr |

| May 2026 | ~$45–47B | Sacra |

| Early Jun 2026 (disputed) | ~$60B+ | SemiAnalysis (via BigGo) |

Sources: VentureBeat, SaaStr, Sacra

The structural driver, repeated across nearly every source, is client mix. Roughly 75–85% of Anthropic’s revenue is usage-based API billing to businesses, versus consumer subscriptions accounting for only about 5%; SemiAnalysis’s analysis (via BigGo Finance) contrasts this with OpenAI, where over 65% of Q1 2026 revenue was subscription-based and consumer ARR represented roughly 40% of the total. More than 500 companies spend over $1 million annually with Anthropic (a figure that had doubled from roughly 500 in under two months as of April 2026, per Sacra), and eight of the Fortune 10 are customers. Anthropic’s CFO Krishna Rao reportedly disclosed a net revenue retention rate of 500% on a podcast in May 2026 — meaning the customer cohort contributing $30 billion in Q1 ARR had generated only about $2 billion a year earlier, an expansion rate with no obvious precedent in enterprise software.

Claude Code, launched publicly in mid-2025, is the single clearest illustration of this dynamic: it reached $1 billion in annualized run-rate within roughly six months, then more than doubled to over $2.5 billion by February 2026, with business subscriptions quadrupling in the first six weeks of the year alone.

2.2 The Margin Question — And Why It’s Genuinely Contested

This is where the sourcing gets messier, and it’s worth surfacing the disagreement rather than picking a number and moving on, because the estimates in circulation right now differ by roughly 40 percentage points depending on the source and the reporting window:

| Source | Gross Margin Estimate | Period |

|---|---|---|

| The Information | 40% (revised down from 50%) | 2025 projection |

| Medium (Adeayo) | Negative 94% | 2024 actual |

| Yahoo Finance / business-quality framework | ~44% (compute cost $0.71/$1 revenue in Q1, $0.56 projected Q2) | Q1–Q2 2026 |

| BigGo/SemiAnalysis | ~60% | 2026 |

| ChatForest | 38% → 70%+ on inference | Trajectory through Q2 2026 |

| BigGo/SemiAnalysis (API-specific) | 80%+ | API business line only, 2026 |

| Earlier TechCrunch reporting | Target 77% | 2028 |

*Sources: The Information, Medium, Yahoo Finance, BigGo Finance</br>

The spread is explainable, not just noisy: overall company gross margin (which includes lower-margin consumer and cloud-reseller-routed revenue) is a genuinely different number from API-specific gross margin (which excludes the fixed costs of serving free-tier or subscription users). SemiAnalysis’s own reporting distinguishes exactly this way — company-wide margin near 60%, API-line margin above 80%. The Yahoo Finance/business-quality piece frames the entire $965 billion IPO valuation as hinging on which of these numbers proves durable: at 40–50% sustained gross margins, the pricing implies $345–450 billion in 2030 revenue is achievable; below 35%, the same framework says fair value compresses by 70–81%.

2.3 The Contested “First Profitable Quarter”

The most consequential — and most disputed — claim in the current reporting cycle is that Anthropic will post its first-ever profitable quarter in Q2 2026: $10.9 billion in revenue (more than double Q1’s reported $4.8 billion) and roughly $559 million in operating profit, a milestone the company had previously guided investors not to expect before 2028.

Independent analyst Ed Zitron’s critique, published on Where’s Your Ed At, is the sharpest pushback in circulation and deserves to be represented on its own terms rather than summarized away: Zitron argues the profit figure is mechanically inflated by a temporary ramp-up discount on Anthropic’s SpaceX compute deal — reportedly $1.25 billion/month, or $15 billion/year, for Colossus 1 and 2 capacity — with the discount applying specifically during the same May–June window used to calculate the “profitable” quarter. He further flags that Anthropic’s own historical ARR disclosures are difficult to reconcile with CFO Krishna Rao’s sworn court statement in March 2026 that revenue was “exceeding $5 billion to date,” a figure that sits awkwardly against previously reported ARR snapshots implying much higher cumulative revenue. Separately, OpenAI has publicly disputed Anthropic’s headline ARR methodology, arguing (per the Markman Capital Insight analysis) that Anthropic’s real net revenue is closer to $22 billion than the $30 billion gross ARR figure, because Anthropic books gross revenue from cloud-reseller-routed usage (AWS Bedrock, Google Cloud) rather than the net amount after partner payouts.

On the other side, a separate rebuttal (Markman Capital Insight) argues the accounting critiques, whatever their merit, don’t address the underlying unit-economics trend: compute cost per dollar of revenue reportedly fell 21% in a single quarter, and — crucially — Anthropic itself has been unusually explicit that Q2 profitability is not expected to persist into subsequent quarters, given planned increases in training and infrastructure spending. That’s a more candid disclosure posture than companies typically take around a headline profitability milestone, and it’s worth weighing as a data point in its own right: Anthropic is not claiming a permanent inflection, only a quarter in which the numbers lined up.

Competing Reads: Q2 2026 Profitability Architecture

Divergent Valuation Models & Structural Discrepancy Matrix

Bull Case Vector

Bear Case Vector

2.4 The Cost Side: What Anthropic Is Actually Buying

Anthropic’s compute commitments are large enough to be the primary swing factor in whether any given quarter’s margin holds. Beyond the SpaceX deal, the company has committed to a $21 billion order with Broadcom for custom TPU-class chips (Broadcom is estimated to capture $21 billion in 2026 revenue and $42 billion in 2027 from this relationship), a separate $50 billion US infrastructure buildout with Fluidstack (Texas and New York, coming online through 2026), and — per Amazon’s $25 billion investment — access to up to 5 gigawatts of Trainium capacity, alongside a further 5 gigawatts from Google/Broadcom TPUs starting in 2027. SemiAnalysis estimates that over 60% of Anthropic’s current compute is allocated to training and internal needs rather than customer-facing inference, and that the company plans to reinvest at least 25% of revenue into training compute going forward — meaning the margin story and the reinvestment story are, by design, in tension with each other.

2.5 Why the Divergence From OpenAI Still Holds Despite the Noise

Strip away the disputed specifics and a structural difference remains that most sources agree on directionally, even if they disagree on magnitude: Anthropic’s customer base is enterprise-concentrated and usage-based, which produces stickier, higher-margin-per-token revenue than OpenAI’s consumer-subscription-heavy base, where roughly 900 million weekly free users generate inference cost without proportionate revenue. SemiAnalysis’s estimate that OpenAI’s free-user base costs roughly $0.70 per person per month to serve — a cost Anthropic largely doesn’t carry — is a concrete mechanism for a margin gap that shows up consistently, in some magnitude, across nearly every independent analysis in this search. That’s the real substance behind “Anthropic reaches breakeven faster”: not any single disputed profitability headline, but a business-mix difference that several unrelated analysts, using different methodologies, keep arriving at independently.

Figure 2: Anthropic ARR Growth vs. Gross Margin Trajectory, 2024–2026

Figure 2: Anthropic ARR Growth ($B, left axis) vs. Estimated Gross Margin (%, right axis), 2024–2026. Margin figures vary by source (38–80% range reported); chart uses the mid-range trajectory. Sources: VentureBeat, SaaStr, Sacra, The Information, BigGo/SemiAnalysis.

Chapter 3 — The Reckoning: IPO Pressure, Investor Expectations, and What “Someone Keeping Them Afloat” Actually Means

3.1 Two IPOs, Same Season

Both companies filed confidentially for public listings within a week of each other: OpenAI on June 8, 2026, targeting a valuation above $1 trillion with Goldman Sachs and Morgan Stanley leading; Anthropic on June 1, 2026, after closing a $65 billion Series H at a $965 billion post-money valuation. Together with SpaceX — which had already begun trading by mid-June — the three companies were, per Yahoo Finance’s coverage of Goldman Sachs strategist Ben Snider’s analysis, collectively pursuing something close to $3.8 trillion in combined market capitalization, an issuance wave large enough that Goldman felt it necessary to publicly reassure markets it wouldn’t “derail the bull market.” Forbes’ most recent coverage (within the last few days of this analysis) notes both companies now appear to be slipping past their original fourth-quarter 2026 target, even as each races to be first to a successful listing.

The stakes of getting the timing and framing right are unusually high because, as PitchBook’s Harrison Rolfes told Morningstar, “revenue quality” — not revenue growth — is what public-market investors will actually underwrite, and that’s a different test than the one both companies have been passing in front of private investors for the last two years.

3.2 The Circularity Problem

The mechanism investors are increasingly focused on is what several outlets now call circular financing: hyperscalers and chipmakers investing equity into the AI labs that then spend that same capital back on the investors’ own cloud or hardware. Morningstar’s reporting lays out concrete instances — Microsoft and Nvidia jointly committing $15 billion to Anthropic, which in turn pledged $30 billion in Azure spend; Amazon committing up to $50 billion to OpenAI alongside an expanded $100 billion AWS agreement; Nvidia’s $30 billion stake in OpenAI’s $122 billion round. Rolfes’ central objection is structural, not just aesthetic: these arrangements aren’t partnerships with aligned incentives so much as fixed claims on a lab’s future upside — “when revenue misses, the hyperscaler doesn’t absorb the pain alongside you; they get paid first.” Rolfes separately noted that OpenAI’s infrastructure obligations now exceed $1.15 trillion across Oracle, Microsoft, and Amazon combined — a liability figure that dwarfs current revenue by roughly two orders of magnitude.

The Wall Street Journal reporting cited in the same Morningstar piece adds a sharper edge: OpenAI has reportedly missed internal growth targets, and CFO Sarah Friar has warned that if revenue doesn’t accelerate, the company could struggle to pay for computing contracts already signed (OpenAI has disputed this characterization). Whether or not that specific dispute resolves in OpenAI’s favor, the exposure it points to is real and quantifiable: fixed, long-duration compute commitments stacked against revenue that, per Chapter 1, is still running at roughly 65 cents of burn for every dollar earned.

3.3 Nvidia’s Pullback — A Signal Worth Reading Carefully

In one of the more concrete data points bearing on investor sentiment, Nvidia CEO Jensen Huang told the Morgan Stanley TMT conference on March 4, 2026, that Nvidia’s recent investments in OpenAI ($30 billion) and Anthropic ($10 billion) would likely be its last direct equity positions in either company. Huang’s stated reason — that “investment opportunities at the early-stage level close once companies go public” — was treated skeptically by multiple outlets, since late-stage private investors routinely pile in right up to an IPO rather than stepping back early. Technology.org’s reporting notes the finalized Nvidia commitment in OpenAI’s round ($30 billion) came in well below an earlier pledge, and floats several competing, non-exclusive explanations worth holding simultaneously rather than picking one: growing bubble-optics concern around circular investment; Nvidia’s own DGX Cloud and NIM inference products increasingly competing with the labs it was investing in, creating governance conflicts; and — more idiosyncratically — Anthropic CEO Dario Amodei’s public comparison of chip sales to approved Chinese buyers to “selling nuclear weapons to North Korea,” which put Nvidia in an uncomfortable position as both his company’s investor and a seller into that same Chinese market. Morgan Stanley and Goldman Sachs equity analysts both read the pullback as fundamentally reassuring for Nvidia’s own stock — reducing conflict-of-interest overhang — which is a distinct question from whether it’s reassuring for OpenAI’s or Anthropic’s.

3.4 The Political Risk Layer

Regulatory and political exposure is no longer a hypothetical line item for either company. Forbes’ recent OpenAI-vs-Anthropic comparison notes the U.S. government pushed OpenAI to sell a 5% stake to the government, and — separately — that the Department of Commerce required Anthropic to withdraw its newly launched Claude Fable 5 and Mythos 5 models in mid-June 2026 over export-control concerns tied to foreign-national access, a restriction the Department lifted roughly two and a half weeks later. That episode is a useful concrete illustration of a risk category that’s easy to wave at abstractly and harder to price: both companies now have commercial roadmaps that can be interrupted by federal action on short notice, immediately ahead of the exact window in which public-market investors will be scrutinizing execution predictability most closely.

Who Gets Paid First: The Structure of “Staying Afloat”

Liquidity Waterfall & Capital Allocation Priority Matrix

Capital Liquidation Seniority Hierarchy

| Claim Type | Ecosystem Holders | Priority Seniority Structure |

|---|---|---|

|

Fixed Compute Contracts (Take-or-pay, multi-year) |

Oracle, CoreWeave, SpaceX, Fluidstack | Paid regardless of lab’s margin |

| Revenue-Share / License Claims | Microsoft (OpenAI) | Capped total, contractual through 2030/32 |

|

Equity Stakes Tied to Compute Commitments (Circular financing) |

Nvidia, Amazon, Google, Microsoft (Both labs) | Subordinate to above; upside-linked but exit-dependent |

|

Public Equity Holders (Post-listing) |

Future IPO Investors | Last in line; absorb residual risk |

3.5 What “Keeping Them Afloat” Actually Buys the Lender

This is the throughline connecting all three chapters. In every version of the financing structure surveyed here — Microsoft’s capped-but-durable revenue claim, Nvidia’s now-closing equity window, the Amazon/Google/Broadcom compute-for-equity arrangements, even the federal government’s 5% OpenAI stake — the capital provider extracts something more durable than a simple return: a contractual claim, a resale right, a compute lock-in, or in the government’s case, a governance foothold. None of this is unusual for capital-intensive industries in a buildout phase; what’s unusual is the compressed timeline in which the compounding claims have stacked up (roughly eighteen months, per the timeline in Chapter 1) against companies whose own path to self-sufficient cash flow remains, by nearly every source surveyed across all three chapters, somewhere between 2027 and 2030.

The Bloomberg Businessweek framing captures the asymmetry cleanly: with $725 billion in combined 2026 capex disclosed by the four largest tech companies and Sam Altman’s own $600 billion data-center budget through 2030, “AI may be a fantastic long-term investment, but today’s frothy atmosphere increases the chances of real pain along the way” — a caution aimed specifically at the retail investors who, unlike Microsoft, Nvidia, or Amazon, hold no contractual seniority and no resale rights if the growth curves in Chapters 1 and 2 bend the wrong way before 2030.

Figure 3: Infrastructure Obligations vs. Current Annualized Revenue

Figure 3: Long-term infrastructure/compute obligations vs. current annualized revenue ($B, log scale). OpenAI obligations per Morningstar/PitchBook estimate (Oracle+Microsoft+Amazon, $1.15T); Anthropic obligations approximate sum of disclosed multi-year commitments (SpaceX, Broadcom, Fluidstack, Amazon, Google). Figures are estimates from press reporting, not audited disclosures.

{kind=link}