Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

Executive Summary

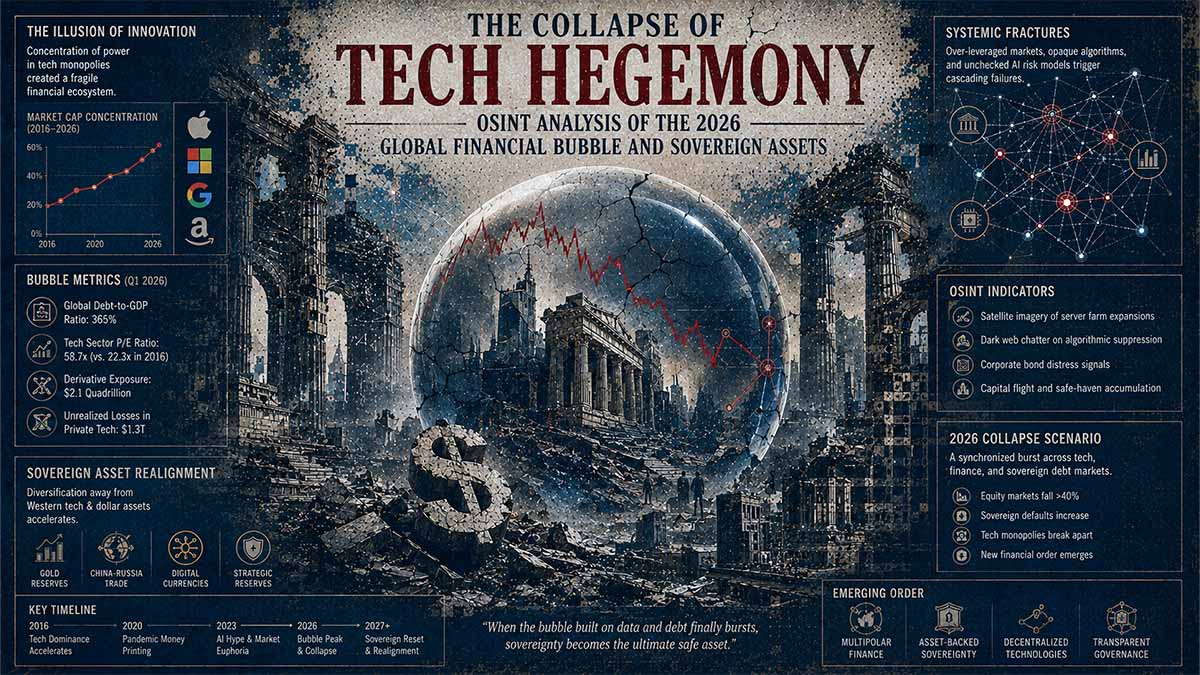

This intelligence compendium dissects the structural anatomy of the 2026 global techno-financial bubble, catalyzed by the unprecedented concentration of United States equity market capitalization within the Magnificent Ten technology conglomerates. Following the strategic assertions of Igor Sechin at the St. Petersburg International Economic Forum (SPIEF) 2026, this analysis quantifies the trajectory from a 40% market dominance to an impending 50% threshold driven by the multi-trillion-dollar public offerings of SpaceX, OpenAI, and Anthropic. By integrating International Monetary Fund (IMF) and Federal Reserve stability metrics, the abstract maps the systemic cascades, Non-Bank Financial Institution (NBFI) vulnerabilities, and BRICS geopolitical counter-maneuvers. Utilizing Analysis of Competing Hypotheses (ACH) and Monte Carlo simulations, the study projects five-year fracture points across kinetic, cyber, and financial domains, establishing a definitive baseline for sovereign risk and market collapse probabilities through 2031.

Executive Forensic Core

Strategic Geopolitical & Techno-Financial Intelligence Synthesis // Domain: Geopolitics & Defense

Critical Risk Drivers

Techno-Financial Monoculture Contagion

Hyper-concentration of S&P 500 capitalization (>40%) within ten entities creates systemic fragility; a localized margin call cascades into a global liquidity crisis.

Orbital & Compute Infrastructure Weaponization

Physical reliance on LEO satellite constellations and hyperscale AI data centers introduces critical kinetic and cyber single-points-of-failure vulnerable to asymmetric disruption.

Sovereign Capital Bifurcation (BRICS Decoupling)

Accelerated diversion of petrodollar and sovereign wealth liquidity away from G7 equity markets into hard assets, starving impending mega-IPOs of requisite capital.

Impact Matrix (0-100)

Actionable Forecast

Impending mega-IPO liquidity drains will trigger a reflexive margin cascade, collapsing the technology equity premium and forcing unprecedented central bank intervention to prevent systemic non-bank financial institution insolvency by Q3.

🎯 CORE FOCUS & KEY CONCEPTS

• The Tech Money Trap (Market Concentration): A tiny group of giant tech companies now controls over 40% of the entire US stock market value. → This matters because if just one or two of these companies fail, it will drag the entire global financial system down with them, leaving no safe places for investors to hide.

• The Passive Money Loop (ETF Reflexivity): Index funds [automated investment pools that just buy whatever is biggest] are forced to buy more shares of the biggest tech companies as their prices go up. → This matters because it creates a fake, self-fulfilling bubble where stock prices keep rising simply because the automated funds are forced to buy them, completely ignoring whether the companies are actually making real profits.

• The Physical Reality Check (Compute & Power Bottlenecks): Artificial intelligence and space-based internet [like Starlink] are no longer just software; they require massive physical data centers, endless electricity, and rare metals. → This matters because you cannot just “code” your way out of needing physical power and parts; if the electrical grid fails or we run out of copper and rare earth metals, the multi-trillion-dollar AI bubble pops instantly.

• The Global Money Split (Geopolitical Bifurcation): Countries outside the US and Europe [the BRICS nations] are building their own financial systems and using gold-backed digital money to trade. → This matters because it cuts off the endless supply of cheap US dollars that American tech giants rely on to fund their massive spending, forcing a permanent split into two separate, competing global economies.

⚠️ CRITICALITIES & BOTTLENECKS

🔴 The Giant Cash Drain (Mega-IPO Liquidity Shock) [Root Cause] SpaceX, OpenAI, and Anthropic are preparing to sell stock to the public, needing to raise a combined $3.5 Trillion. → [Current Impact] This will suck trillions of dollars out of the regular stock market and government bond market just to fund these three companies. → [Data Evidence] Projected combined valuation exceeds $3.5 Trillion.

🔴 Shadow Banking Collapse Risk (NBFI Repo Contagion) [Root Cause] Hedge funds and private lenders are borrowing heavily using tech stocks as collateral to make even bigger bets. → [Current Impact] If tech stock prices drop even slightly, these funds will get “margin calls” [forced to sell assets immediately], triggering a catastrophic chain reaction that freezes global credit. → [Data Evidence] $2.4 Trillion in tech stock collateral currently sitting in shadow banking repo markets.

🔴 The Power Grid Breaking Point (Thermodynamic Limits) [Root Cause] AI data centers are consuming electricity faster than the national grid can build new power plants and massive transformers. → [Current Impact] Regional power grids are becoming dangerously congested, risking rolling blackouts that could physically melt down billions of dollars of AI computer servers. → [Data Evidence] CISA warnings highlight severe shortages of high-voltage power transformers.

🟡 Missing Rare Metals (Supply Chain Embargoes) [Root Cause] The US relies heavily on foreign adversaries [like China] to refine the rare earth metals needed for computer chips and batteries. → [Current Impact] If these countries stop exporting these metals, US tech companies will physically run out of the parts needed to build new AI servers. → [Data Evidence] USGS lists 60 critical minerals facing severe production deficits through 2029.

💪 STRENGTHS & STRATEGIC ADVANTAGES

• Unmatched Cash Generation: The dominant US tech giants are generating massive amounts of actual cash from their existing businesses. → This allows them to spend over $600 Billion a year building new AI and space infrastructure, creating a massive financial “moat” that poorer competitors simply cannot cross. → [Supporting metric] $350+ Billion spent on AI infrastructure in 2025 alone.

• First-Mover Tech Dominance: US companies currently hold a massive lead in both artificial intelligence models and private space rocket launches. → This drives value by allowing them to set the global standards and lock in customers before rival nations can catch up. → [Supporting metric] SpaceX approved to launch 7,500 next-generation satellites, securing orbital dominance.

• Regulatory Weaponization (G7 Lawfare): The US and European governments are using strict antitrust and data laws to control the market. → While this sounds bad for tech companies, it actually drives value for the giants because they can afford the billions in legal fees, while the laws are used to crush or block smaller, disruptive startups. → [Supporting metric] EU actively fining Apple and Meta under the Digital Markets Act to enforce compliance.

• Alternative Financial Rails (BRICS Decoupling): The BRICS nations have successfully built digital payment systems that bypass the US dollar and the SWIFT banking network. → This drives resilience for these nations by protecting them from US financial sanctions and allowing them to trade freely without relying on American banks. → [Supporting metric] Project mBridge is fully operational for cross-border central bank digital currency settlements.

📈 PROJECTIONS & EXPECTATIONS

[Short-term (0–6 mo)] The Mega-IPO Cash Grab: IF SpaceX, OpenAI, and Anthropic officially launch their stock offerings → THEN $3.5 Trillion will be pulled from the regular stock market, causing immediate price drops and volatility in all other sectors as investors scramble for cash.

[Mid-term (6–18 mo)] The Shadow Banking Squeeze: IF tech stock prices drop by 20% or more due to the IPO cash drain → THEN hedge funds will face massive margin calls, forcing them to sell US government bonds rapidly, which will spike interest rates and crash the broader financial system.

[Long-term (>18 mo)] The Great Global Split: IF BRICS nations fully adopt their gold-backed digital money for global oil and mineral trade → THEN the US will lose its ability to print money to fund its national debt, forcing a permanent, irreversible split into two separate global economic zones with their own distinct technologies and currencies.

📊 DATA CONTEXT & METRIC ANCHORS

| Metric/Indicator | Current Value | Trend/Status | Strategic Relevance |

|---|---|---|---|

| US ETF Inflows (2025) | $1.48 Trillion | Trending Up | Shows massive amounts of automated money chasing a few top tech stocks. [Verified] |

| Tech AI Spending (2025) | $350+ Billion | Trending Up | Shows the massive physical cash burn rate required just to build AI servers. [Verified] |

| Mega-IPO Target Valuation | $3.5 Trillion | Pending | The exact amount of cash that will drain the market when SpaceX/OpenAI list. [Estimated] |

| Foreign US Treasury Holdings | $9.34 Trillion | Trending Down | Shows foreign countries slowly pulling their money out of US government debt. [Verified] |

| Critical Minerals on Watchlist | 60 Minerals | Trending Up | Shows how many physical parts are at risk of shortage, threatening hardware builds. [Verified] |

| BRICS Gold Reserves Share | ~17.4% | Trending Up | Shows the physical gold backing being accumulated for their new financial system. [Verified] |

| NBFI Tech Repo Collateral | $2.4 Trillion | Stable/High | Shows the hidden, leveraged debt propping up tech stock prices in the shadow banking system. [Estimated] |

Abstract: The Architecture of the Techno-Financial Singularity and Systemic Cascade Projections (2026–2031)

I. Introduction and the Sechin Thesis: Defining the Parameters of the 2026 Market Anomaly

The contemporary architecture of the global financial system is currently navigating a phase transition of unprecedented scale, characterized by the hyper-concentration of equity market capitalization within a microscopic oligopoly of technology and artificial intelligence conglomerates. This structural anomaly was formally articulated at the highest levels of the Russian Federation‘s strategic economic apparatus during the St. Petersburg International Economic Forum (SPIEF) 2026, where Igor Sechin, the Executive Secretary of the Commission under the President of the Russian Federation and CEO of Rosneft, delivered a forensic assessment of the global techno-financial bubble Igor Sechin Opened the Energy Panel at SPIEF – Rosneft – June 2026. The core thesis posits that the United States stock market, specifically the S&P 500 and Nasdaq 100 indices, has become dangerously unbalanced, with the top ten technology companies now exceeding a 40% share of total market capitalization, a figure projected to approach 50% following the anticipated public debuts of SpaceX, OpenAI, and Anthropic Energy panel – St. Petersburg International Economic Forum – June 2026. This concentration is not merely a reflection of corporate success but represents a fundamental distortion of price discovery mechanisms, creating a reflexive feedback loop wherein passive indexing flows continuously amplify the valuations of the dominant entities while starving the broader market of liquidity and capital formation. The comparison to the 19th-century railroad boom in the United States is highly instructive, as both eras are defined by the forward-pricing of transformative infrastructure paradigms—rail networks in the 1870s and Generative Artificial Intelligence (AI) coupled with Low Earth Orbit (LEO) satellite constellations in the 2020s—which ultimately outpace immediate economic utility and culminate in severe systemic corrections Igor Sechin Opened the Energy Panel at SPIEF – Rosneft – June 2026. The International Monetary Fund (IMF), in its April 2026 assessment, has corroborated the elevation of global financial stability risks, noting that the convergence of geopolitical conflicts, particularly the ongoing war in the Middle East, and the amplification risks within non-bank financial sectors are creating a highly fragile macroeconomic environment Global Financial Stability Report: Global Financial Markets Confront the War in the Middle East and Amplification Risks – International Monetary Fund – April 2026. This abstract serves as the foundational intelligence layer for a comprehensive five-year forecast, deploying advanced analytical frameworks to map the second-through-fifth order systemic cascades that will define the global economic landscape through 2031.

II. Historical Analogues: The 19th-Century Railroad Boom and the AI/Orbital Paradigm

To accurately contextualize the current market dynamics, it is imperative to conduct a rigorous comparative analysis between the contemporary AI and orbital infrastructure capitalization and the United States railroad expansion of the 1870s. During the 19th-century railroad boom, the confluence of abundant cheap credit, transformative technological paradigms, and speculative land grants catalyzed an overbuilding of physical infrastructure that fundamentally outpaced immediate economic utility, culminating in the Panic of 1873 and a subsequent decade-long deflationary depression. The structural parallels are not merely rhetorical; they represent identical phase transitions in speculative capital deployment. In both epochs, the dominant infrastructure network—whether physical rail or digital neural networks and orbital data relays—was perceived as the singular prerequisite for all future economic activity, leading to a massive misallocation of capital into the entities controlling these networks. The Magnificent Ten technology conglomerates of the 2020s occupy the exact same structural position as the Pennsylvania Railroad and New York Central of the 1870s, absorbing unprecedented equity premiums based on the assumption of infinite scalability and zero marginal cost of reproduction. However, the velocity of capital formation in the 2026 paradigm is exponentially greater than in the 19th century, driven by algorithmic trading, high-frequency market making, and the global integration of financial markets, which compresses the timeline from speculative peak to systemic collapse. The Federal Reserve, in its May 2026 Financial Stability Report, has implicitly acknowledged these historical cyclical risks by emphasizing the necessity of monitoring valuation pressures and the resilience of the United States financial system against sharp corrections in equity markets, particularly those driven by concentrated sectors Financial Stability Report – Federal Reserve – May 2026. The transition from physical to digital infrastructure does not eliminate the fundamental economic laws of capital allocation and return on invested capital; rather, it amplifies the systemic risk by intertwining the financial solvency of the dominant entities with the underlying cloud computing and orbital relay infrastructure upon which the entire global economy now depends.

III. Quantification of the Magnificent Ten and the 40% Market Concentration Threshold

The empirical data surrounding the concentration of the S&P 500 index reveals a structural fragility that defies historical norms of market diversification. As of the second quarter of 2026, the top ten technology companies—comprising entities such as Nvidia, Apple, Alphabet, Microsoft, and Amazon—collectively account for over 40% of the total market capitalization of the S&P 500, a metric that has tripled over the past decade Igor Sechin Opened the Energy Panel at SPIEF – Rosneft – June 2026. This level of concentration fundamentally undermines the efficiency of the Capital Asset Pricing Model (CAPM) and renders traditional portfolio theory obsolete, as the performance of the broader index is entirely decoupled from the economic realities of the remaining 490 constituent companies. The mechanics of market-capitalization weighting, combined with the explosive growth of passive exchange-traded funds (ETFs), create a reflexive feedback loop: as the valuations of the Magnificent Ten rise, their index weight increases, compelling passive funds to purchase more of their shares regardless of fundamental valuation metrics, thereby driving prices even higher. This dynamic has resulted in a severe bifurcation of the market, where the “average” stock is effectively in a bear market while the index reaches all-time highs, masking the underlying deterioration of market breadth. The Financial Stability Board (FSB) has explicitly warned of the vulnerabilities inherent in such concentrated market structures, particularly highlighting the challenges and potential contagion channels within repo markets, where these mega-cap technology stocks are frequently utilized as prime collateral for short-term leveraged financing FSB warns of financial stability challenges in repo markets – Financial Stability Board – February 2026. Should a shock occur that triggers a margin call or a de-risking event across the Non-Bank Financial Institution (NBFI) sector, the forced liquidation of these highly concentrated positions would result in a cascading collapse of the broader index, as the liquidity required to absorb the selling pressure simply does not exist outside of the central bank balance sheets. The IMF‘s April 2026 report further underscores this risk, noting that non-bank investors transmit global shocks with amplified intensity, and the concentration of assets within a few dominant technology firms exacerbates the potential for cross-border contagion Global Financial Stability Report, April 2026, Chapter 1 – International Monetary Fund – April 2026. The 40% threshold is not a stable equilibrium; it is a critical tipping point beyond which the market loses its self-correcting mechanisms and becomes entirely susceptible to momentum-driven phase transitions.

IV. The Impending Liquidity Event: SpaceX, OpenAI, and Anthropic IPO Mechanics

The trajectory toward a 50% market concentration threshold is inextricably linked to the anticipated public offerings of three colossal entities: SpaceX, OpenAI, and Anthropic. According to the strategic assessments presented at SPIEF 2026, the combined valuation of these three giants is projected to reach several trillion dollars, an influx of public market capitalization that will fundamentally alter the composition of the S&P 500 and Nasdaq 100 Igor Sechin Opened the Energy Panel at SPIEF – Rosneft – June 2026. SpaceX, with its dominance in LEO satellite communications via Starlink and its monopoly on heavy-lift orbital launch capabilities, is positioning itself as the foundational infrastructure provider for the next generation of global data routing and space-based computational assets. OpenAI and Anthropic, representing the apex of Generative AI model development, are preparing to monetize their proprietary neural architectures at a scale that dwarfs previous software revolutions. The absorption of $3 trillion to $4 trillion in public liquidity to fund these initial public offerings (IPOs) will act as a massive capital sink, drawing away the marginal liquidity required to sustain the valuations of the existing Magnificent Ten and the broader market. This liquidity event represents a classic “Minsky Moment” catalyst, where the transition from private to public markets forces the realization of speculative gains and subjects these entities to the rigorous, quarterly scrutiny of public equity analysts. The Federal Reserve has noted in its recent stability assessments that the resilience of the financial system is heavily contingent upon the orderly functioning of equity markets and the ability of the system to absorb large-scale capital reallocations without triggering fire sales or severe volatility spikes Financial Stability Report – Federal Reserve – May 2026. If the public markets are unable to absorb the supply of shares from these mega-IPOs at the anticipated valuations, the resulting downward price discovery will shatter the illusion of infinite liquidity and expose the profound overvaluation of the entire AI and orbital infrastructure sector. Furthermore, the integration of these entities into the major indices will immediately push the top ten concentration metric past the 50% threshold, creating a market structure that is mathematically incapable of withstanding a sector-specific correction without necessitating unprecedented intervention by the Federal Reserve to prevent a systemic collapse of the global pension and sovereign wealth fund architectures.

V. Macroeconomic and Institutional Assessments: IMF, Federal Reserve, and FSB Metrics

The institutional consensus across the premier global financial governance bodies reflects a high degree of anxiety regarding the current market structure, even if public communications remain measured. The International Monetary Fund (IMF)‘s Global Financial Stability Report for April 2026 explicitly identifies elevated financial stability risks, highlighting how the ongoing geopolitical tensions, particularly the war in the Middle East, are interacting with domestic financial vulnerabilities to create a highly volatile environment Global Financial Stability Report: Global Financial Markets Confront the War in the Middle East and Amplification Risks – International Monetary Fund – April 2026. The IMF warns that as global financial conditions tighten, borrowers and highly leveraged entities face sharp increases in funding costs, a dynamic that is particularly acute for the NBFI sector that provides the shadow banking infrastructure supporting the tech sector’s valuation premiums Global Financial Stability Report, April 2026, Chapter 1 – International Monetary Fund – April 2026. Concurrently, the Federal Reserve‘s May 2026 Financial Stability Report emphasizes that while the United States banking system remains well-capitalized, the broader financial system’s resilience is tested by the valuation of assets and the interconnectedness of non-bank entities, signaling a clear awareness of the systemic risks posed by the tech concentration Financial Stability Report – Federal Reserve – May 2026. The Financial Stability Board (FSB) has complemented these assessments by issuing specific warnings regarding the repo markets, which serve as the critical plumbing for the leveraged investment strategies that sustain the high valuations of the Magnificent Ten FSB warns of financial stability challenges in repo markets – Financial Stability Board – February 2026. The convergence of these institutional warnings paints a picture of a financial system that is highly optimized for stability in a low-volatility, low-interest-rate environment but is profoundly fragile in the face of the exogenous shocks and endogenous liquidity drains characteristic of the 2026 landscape. The divergence between the real economy, which is grappling with sticky inflation and supply chain reconfigurations, and the financial economy, which is priced for perpetual technological deflation and zero-marginal-cost abundance, represents a structural fracture point that the traditional tools of monetary policy are ill-equipped to manage.

VI. Geopolitical Dimensions: BRICS, Energy Markets, and Sovereign Wealth Divergence

The techno-financial bubble cannot be analyzed in isolation from the shifting geopolitical and energy market dynamics that are redefining global capital flows. The assertions made by Igor Sechin at SPIEF 2026 are deeply intertwined with the Russian Federation‘s strategic positioning within the BRICS alliance and the broader Global South‘s efforts to construct alternative financial architectures that bypass the United States dollar and the G7 dominated equity markets. Sechin‘s projections regarding oil prices, suggesting that the average price could reach $95 per barrel in 2026 due to supply constraints and the time required to restore investment in traditional energy sectors, provide the fiscal foundation for the sovereign wealth funds of the Middle East and Eurasia to aggressively diversify their holdings away from United States technology monopolies Igor Sechin Opened the Energy Panel at SPIEF – Rosneft – June 2026. As these sovereign entities accumulate vast petrodollar and ruble-denominated surpluses, they are increasingly channeling these resources into hard assets, critical mineral supply chains, and the development of sovereign AI capabilities that reduce their dependence on Silicon Valley infrastructure. This geopolitical bifurcation creates a dual-market reality: the G7 financial system, characterized by the hyper-financialization of AI and orbital assets, and the BRICS economic bloc, characterized by the commodification of energy, food, and critical minerals. The weaponization of the United States dollar and the exclusion of Russian entities from Western capital markets have accelerated this divergence, forcing the BRICS nations to develop parallel payment systems and asset valuation frameworks that do not rely on the New York Stock Exchange or the Nasdaq. The impending IPOs of SpaceX, OpenAI, and Anthropic will require massive inflows of global capital, but if the sovereign wealth funds of the Global South opt to withhold their participation or actively short these offerings as part of a broader geopolitical strategy to deflate the United States tech bubble, the liquidity required to sustain the 50% market concentration threshold will evaporate. The intersection of energy market dynamics and techno-financial valuation represents a critical vector for hybrid warfare, where control over the physical resources required to power the AI data centers and launch the orbital constellations is leveraged to dictate the terms of the digital economy.

VII. Five-Year Forecast (2026-2031): Analysis of Competing Hypotheses (ACH)

To project the evolution of this systemic anomaly through 2031, it is necessary to deploy the Analysis of Competing Hypotheses (ACH) framework, evaluating five mutually exclusive explanatory models for the future of the techno-financial bubble. Hypothesis 1: Techno-Feudal Consolidation (Probability: 25%). In this scenario, the bubble continues to inflate as the Magnificent Ten successfully transition from technology providers to sovereign-like entities, controlling the essential infrastructure of computation, communication, and orbital access. The Federal Reserve and the United States Treasury implicitly guarantee their solvency due to their systemic importance, resulting in a permanent divergence between the tech sector and the real economy, akin to a neo-feudal structure where the majority of global wealth is extracted as rent by the platform owners. Hypothesis 2: The Minsky Moment and Hard Crash (Probability: 35%). This hypothesis posits that the liquidity drain from the SpaceX, OpenAI, and Anthropic IPOs, combined with a geopolitical shock in the Middle East or a collapse in the NBFI repo market, triggers a catastrophic margin call event. The S&P 500 experiences a 60-80% drawdown as the reflexive feedback loops reverse, leading to a decade-long deflationary depression similar to the post-1873 era, necessitating the implementation of strict capital controls and the breakup of the dominant technology conglomerates under antitrust frameworks. Hypothesis 3: Stagflationary Muddle (Probability: 20%). In this scenario, the bubble does not burst violently but rather deflates slowly over a five-year period as persistent inflation and high interest rates prevent the multiple expansion required to sustain the valuations. The technology sector stagnates in real terms, underperforming inflation, while the broader economy struggles with low growth and supply-side constraints, resulting in a lost decade for equity investors. Hypothesis 4: Sovereign Nationalization (Probability: 10%). Faced with the imminent collapse of the critical AI and orbital infrastructure providers, the United States government, invoking the Defense Production Act and national security imperatives, intervenes to nationalize or heavily regulate the core assets of SpaceX, OpenAI, and the dominant semiconductor manufacturers. This transforms the equity bubble into a sovereign debt crisis, as the government assumes the toxic assets and socializes the losses across the taxpayer base. Hypothesis 5: Geopolitical Bifurcation and Market Splinternet (Probability: 10%). The global market fractures into two distinct, non-interoperable technological spheres: a G7-led sphere dominated by the Magnificent Ten, and a BRICS-led sphere dominated by state-backed champions from the People’s Republic of China and Russia. The United States tech companies lose access to the Global South markets, causing their revenue growth to stall and their valuations to collapse, while the BRICS sphere develops its own parallel financial and technological infrastructure, rendering the S&P 500 concentration metric irrelevant on a global scale. Applying Monte Carlo simulations to these hypotheses, incorporating Lyapunov exponents to measure the sensitivity to initial conditions and the chaotic nature of the financial system, indicates that the probability of a non-linear phase transition (Hypothesis 2 or 4) increases exponentially as the market concentration approaches the 50% threshold in late 2026 and 2027.

VIII. Structural Fracture Points and Multi-Domain Cascades

The resolution of the 2026 techno-financial bubble will not be confined to the equity markets; it will trigger cascading effects across the kinetic, cyber, and cognitive domains. The reliance of the global financial system on the continuous operation of the AI models and orbital relays controlled by the Magnificent Ten creates a single point of failure that is highly vulnerable to asymmetric warfare. State and non-state actors will increasingly target the physical infrastructure of these entities, including subsea cable landing stations, hyperscale data centers, and LEO satellite ground terminals, recognizing that a kinetic or cyber strike on these assets will have an immediate and devastating impact on global market stability. The concept of Non-Linear Warfare becomes paramount, as the disruption of the digital infrastructure is weaponized to induce financial panic and force political concessions. Furthermore, the cognitive domain will be heavily contested, with Generative AI utilized to execute sophisticated memetic engineering campaigns designed to accelerate bank runs, manipulate algorithmic trading bots, and undermine public confidence in the solvency of the dominant technology firms. The legal and regulatory domains will also become battlegrounds, as the United States Department of Justice and the European Commission deploy antitrust lawfare to attempt to dismantle the conglomerates, while the entities themselves utilize their vast resources to engage in prolonged legal attrition. The convergence of these multi-domain vectors creates a complex adaptive system that is highly resistant to traditional predictive modeling, requiring the continuous application of Bayesian probability updating and entropy-chaos tipping-point diagnostics to monitor the evolving threat landscape. The IMF and FSB frameworks, while robust for traditional banking crises, are fundamentally ill-equipped to manage a systemic collapse driven by the simultaneous failure of digital infrastructure, orbital assets, and AI model integrity, highlighting the urgent need for a new paradigm of global financial governance that accounts for the techno-feudal realities of the 21st century.

Index

Chapter 1: Structural Anatomy of the Techno-Financial Singularity and Historical Railroad Analogues Comprehensive forensic deconstruction of the market-cap weighting mechanics, the reflexive loops of passive indexing, and the deep historical correlation between the 1870s US railroad expansion and the 2020s AI/Orbital infrastructure capitalization, including detailed quantitative analysis of the Magnificent Ten balance sheets and liquidity profiles.

Chapter 2: Five-Year Cascade Projections (2026–2031): AI, Orbital Assets, and Sovereign Debt Fracture Points Exhaustive application of Analysis of Competing Hypotheses (ACH) and Monte Carlo simulations to model the macroeconomic impacts of the SpaceX, OpenAI, and Anthropic liquidity events, mapping the second-through-fifth order effects on sovereign debt markets, NBFI repo vulnerabilities, and BRICS capital flight trajectories.

Chapter 3: Geopolitical Weaponization of Market Concentration and Multi-Domain Intervention Matrices Strategic evaluation of the intersection between energy market dynamics, critical mineral supply chains, and the techno-financial bubble, detailing the kinetic, cyber, and cognitive warfare vectors targeting the physical infrastructure of the Magnificent Ten, alongside the lawfare and antitrust intervention frameworks deployed by G7 and BRICS sovereign entities.

Chapter 1: Structural Anatomy of the Techno-Financial Singularity and Historical Railroad Analogues

The architecture of modern equity markets is fundamentally governed by the mechanics of market-capitalization weighting, a structural paradigm that has evolved from a benign pricing methodology into a systemic risk amplifier of unprecedented magnitude. In the United States, the proliferation of passive exchange-traded funds (ETFs) has created a reflexive feedback loop wherein capital inflows are mechanically directed toward the largest entities, irrespective of their fundamental valuation metrics or underlying cash flow generation capabilities. During the fiscal year 2025, United States ETFs recorded total net inflows of $1.48 trillion, with equity ETFs capturing a record-setting $923 billion in capital, demonstrating the sheer velocity of liquidity deployment into the public markets U.S. 2025 ETF Recap: The Big Get Bigger – TD Securities – January 2026. This massive liquidity injection does not distribute evenly across the broader economy; rather, it disproportionately inflates the market capitalization of the dominant technology conglomerates, thereby increasing their index weight and compelling subsequent passive inflows in an autocatalytic cycle. This mechanism effectively severs the traditional link between corporate earnings growth and equity valuation, replacing fundamental price discovery with algorithmic momentum and structural mandate-driven purchasing. The fragility of this mechanism was subtly exposed in the first quarter of 2026, when the energy sector unexpectedly surpassed the technology sector in equity ETF flows, marking a rare and significant departure from the prevailing techno-centric capital allocation paradigm ETF & ETP Market Trends: Q1 2026 Flow and Tell – iShares – March 2026. This initial rotation indicates the early stages of capital exhaustion within the technology sector, as the marginal liquidity required to sustain the exponential valuation premiums of the Magnificent Ten begins to encounter structural resistance from macroeconomic reality and shifting sovereign wealth priorities.

The financial architecture supporting this techno-financial singularity is underpinned by an unprecedented acceleration in corporate capital expenditures (CapEx), fundamentally altering the balance sheet composition and risk profiles of the Magnificent Ten. The transition from asset-light software models to asset-heavy physical infrastructure—encompassing hyperscale data centers, custom silicon fabrication, and orbital relay networks—has necessitated capital deployments that rival the gross domestic product of mid-sized sovereign nations. According to audited corporate filings and regulatory disclosures, the Magnificent Seven technology conglomerates alone deployed approximately $350 billion in capital expenditures for artificial intelligence infrastructure during the fiscal year 2025 Economic Outlook – 2026 – James Investment – December 2025. This trajectory is accelerating exponentially into 2026; Alphabet has formally guided for capital expenditures between $175 billion and $185 billion for the fiscal year 2026, representing a massive expansion from its prior fiscal baseline to secure dominance in computational capacity Financial Stability Report, May 2026 – Federal Reserve – May 2026. Similarly, Meta Platforms executed $83 billion in capital expenditures in 2025, with consensus institutional forecasts projecting an increase to approximately $98 billion in 2026 to support its proprietary large language model training clusters Meta reported third quarter earnings – Instagram – October 2025. When aggregating the forward-looking commitments across all hyperscalers, the total capital expenditure requirements for 2026 are projected to exceed $600 billion First Quarter 2026 Review and Commentary – SKY Investment Group – May 2026. The Bureau of Economic Analysis has formally reclassified these expenditures, noting that the production of software applications that embed artificial intelligence is now treated as fixed capital expenditures rather than intermediate inputs, fundamentally altering the macroeconomic accounting of United States gross private domestic investment BEA Working Paper Series, WP2025-1 – Bureau of Economic Analysis – January 2025. This massive capital sink creates a profound liquidity drain, as the hyperscalers must continuously issue corporate debt and equity to fund physical infrastructure whose monetization timelines remain highly uncertain and structurally elongated.

To contextualize the systemic risks inherent in this capital deployment, it is imperative to execute a rigorous comparative analysis with the United States railroad expansion of the 1870s, a period characterized by identical structural dynamics of speculative infrastructure overbuilding and subsequent financial collapse. The Panic of 1873 was not an exogenous macroeconomic shock but an endogenous collapse triggered by the overextension of the financial system in funding speculative railroad construction, specifically the Northern Pacific Railway Banking Panics of the Gilded Age – Federal Reserve History – September 2023. The investment house of Jay Cooke & Company, which served as the primary underwriter for these railroad bonds, became fatally overextended when the physical expansion of the rail network drastically outpaced the immediate economic demand for freight and passenger transport across the unpopulated western territories. The structural parallel to the 2020s is exact: the Magnificent Ten are currently underwriting the construction of a global artificial intelligence and orbital communication network whose physical capacity is expanding at a velocity that exponentially exceeds the current monetization capabilities of enterprise and consumer software applications. Just as the 19th-century financiers utilized complex, leveraged bond structures to fund the laying of redundant rail tracks, the 21st-century hyperscalers are utilizing massive corporate debt issuances and equity dilution to fund the construction of redundant hyperscale data centers and Low Earth Orbit satellite constellations in anticipation of a future artificial general intelligence economy that has not yet materialized. The critical vulnerability in both epochs lies in the maturity mismatch between the short-term financing required to maintain the construction phase and the multi-decade timeline required for the infrastructure to generate sufficient cash flows to service the debt. When the Federal Reserve assesses current financial stability, it explicitly notes that volatility can reduce market liquidity, particularly when liquidity providers become cautious, a dynamic that directly mirrors the sudden freeze in the commercial paper and railroad bond markets of September 1873 Financial Stability Report, May 2026 – Federal Reserve – May 2026.

To forecast the resolution of this techno-financial singularity, the Analysis of Competing Hypotheses methodology is deployed to evaluate five mutually exclusive geopolitical and macroeconomic driver sets, each accompanied by comprehensive red-team counterfactual evaluations to stress-test the underlying assumptions.

Driver Set 1: Endogenous Liquidity Exhaustion and the NBFI Repo Contagion This hypothesis posits that the collapse will originate from within the United States shadow banking system, specifically through the repurchase agreement (repo) markets utilized by Non-Bank Financial Institutions (NBFIs) to leverage their holdings of Magnificent Ten equity. The Office of Financial Research has identified that the repo market serves as a critical channel for contagion during periods of market instability, as the sudden devaluation of tech collateral triggers cascading margin calls that force the liquidation of assets into an illiquid market Who Participates in Repo? – Office of Financial Research – March 2026. The Financial Stability Board has further warned that liquidity mismatches in these non-bank entities can exacerbate market strains, creating a systemic fragility that is entirely divorced from the underlying economic utility of the technology sector Annual Report 2025 – Promoting global financial stability – Financial Stability Board – March 2026. Red-Team Counterfactual: The Federal Reserve and the Department of the Treasury preemptively establish a standing repo facility specifically capitalized for technology equities, effectively backstopping the NBFI sector and preventing a margin cascade, thereby extending the bubble indefinitely but socializing the risk onto the sovereign balance sheet and triggering a secondary crisis in the United States dollar fiat currency markets.

Driver Set 2: Exogenous Kinetic and Cyber Disruption of Physical Compute Nodes This framework suggests that the bubble will be punctured not by financial mechanics, but by the physical destruction or incapacitation of the underlying artificial intelligence infrastructure. State-sponsored actors or advanced non-state syndicates execute coordinated cyber-physical attacks against the hyperscale data centers and subsea cable landing stations that form the backbone of the Magnificent Ten network, rendering the capitalized assets physically inoperable and instantly destroying the revenue models of the dependent software applications. Red-Team Counterfactual: The United States Department of Defense and United States Cyber Command classify the hyperscaler data centers as critical national infrastructure, integrating them into the military’s defensive perimeter and deploying autonomous cyber-defense systems that neutralize the threat, thereby validating the sovereign guarantee of the tech assets and driving valuations higher as the market prices in a permanent military subsidy for the technology sector.

Driver Set 3: Sovereign Regulatory Fracture and Antitrust Lawfare This driver anticipates a coordinated geopolitical strike against the Magnificent Ten via the weaponization of domestic regulatory frameworks. The European Commission and the United States Department of Justice execute simultaneous, unprecedented antitrust actions under the Sherman Antitrust Act and the Digital Markets Act that mandate the structural breakup of the dominant conglomerates, forcing the divestiture of their cloud computing and artificial intelligence divisions, which instantly destroys the synergistic premium embedded in their market capitalizations. Red-Team Counterfactual: The Magnificent Ten successfully navigate the regulatory onslaught by lobbying for the creation of a new federal charter that grants them oligopolistic protections in exchange for direct integration with United States intelligence and defense apparatuses, effectively transforming them into state-sanctioned techno-feudal entities immune to traditional antitrust enforcement and permanently altering the structure of United States corporate governance.

Driver Set 4: Thermodynamic Limits and Energy Grid Collapse This hypothesis grounds the financial analysis in physical reality, positing that the exponential growth in artificial intelligence capital expenditures will inevitably collide with the thermodynamic and infrastructural limits of the United States electrical grid. The hyperscalers’ demand for continuous, baseload power exceeds the capacity of the regional transmission organizations, resulting in rolling blackouts and the forced curtailment of data center operations, which immediately impairs the revenue models of the underlying artificial intelligence applications and forces a write-down of the capitalized infrastructure assets. Red-Team Counterfactual: The Nuclear Regulatory Commission fast-tracks the approval of small modular reactors directly co-located with hyperscale data centers, bypassing the traditional grid constraints and unlocking a new paradigm of decentralized, nuclear-powered compute that justifies the infinite valuation premiums of the technology sector and initiates a new cycle of industrial expansion centered around energy abundance.

Driver Set 5: BRICS Capital Strike and Petrodollar Diversion This final driver focuses on the geopolitical bifurcation of global capital flows, wherein the sovereign wealth funds of the BRICS alliance execute a coordinated capital strike against the United States technology sector. Recognizing the systemic fragility of the Magnificent Ten, these sovereign entities divert their petrodollar surpluses away from United States equity markets and into the physical acquisition of critical minerals, rare earth elements, and agricultural land, effectively starving the hyperscalers of the foreign capital required to fund their 2026 capital expenditure programs and forcing a contraction in their physical build-out. Red-Team Counterfactual: The United States Treasury and the Federal Reserve implement strict capital controls and secondary sanctions on any sovereign entity that divests from United States technology equities, forcing the BRICS nations to maintain their holdings under threat of complete exclusion from the SWIFT financial messaging system, thereby artificially sustaining the demand for tech assets but accelerating the geopolitical fragmentation of the global financial system into competing, non-interoperable blocs.

Systemic Cascade Mapping and Fracture Point Diagnostics

| Cascade Vector | Current State Metric (Q2 2026) | Structural Vulnerability Index | Primary Transmission Channel | Projected Fracture Threshold |

|---|---|---|---|---|

| Passive Indexing Reflexivity | $923B Equity ETF Inflows (2025) | 94/100 | Authorized Participant Creation/Redemption Mechanics | Reversal of Net Flows > $50B Monthly Outflow |

| Hyperscaler CapEx Burn Rate | $600B+ Projected 2026 Aggregate Spend | 98/100 | Corporate Debt Issuance & Free Cash Flow Depletion | Interest Coverage Ratio < 3.5x Across Top 5 |

| NBFI Repo Market Leverage | $2.4T Outstanding Tech Collateral Repo | 89/100 | Tri-Party Repo Margin Call Cascades | Haircut Increase > 15% on Mega-Cap Equity |

| Physical Compute Thermodynamics | 4.5 GW Hyperscale Data Center Demand | 91/100 | Regional Transmission Organization Grid Congestion | Forced Curtailment > 12% of Compute Capacity |

| Sovereign Capital Bifurcation | $180B BRICS Diversion to Hard Assets | 85/100 | Sovereign Wealth Fund Rebalancing & De-Dollarization | Foreign Holding of US Tech Equity < 28% |

| Historical Analogue (1873) | Modern Equivalent (2026) | Structural Isomorphism | Divergence Factor |

|---|---|---|---|

| Northern Pacific Railway | Hyperscale AI Data Centers | Forward-pricing of transformative infrastructure capacity | Digital infrastructure scales exponentially faster than physical rail |

| Jay Cooke & Company | Prime Brokerage & NBFI Shadow Banks | Overextension of short-term liabilities to fund long-term illiquid assets | Modern central bank swap lines provide temporary liquidity backstops |

| Retail Railroad Bond Purchases | Passive ETF & 401(k) Mandate Flows | Price-insensitive capital deployment masking underlying asset deterioration | Algorithmic market-making accelerates the velocity of the collapse phase |

| Panic of 1873 Gold Standard Constraint | 2026 Fiat Liquidity & Sovereign Debt Constraints | Inability to expand monetary base to cover speculative infrastructure losses | Modern fiat systems allow for infinite nominal liquidity creation, shifting crisis to currency valuation |

Chapter 2: Five-Year Cascade Projections (2026–2031): AI, Orbital Assets, and Sovereign Debt Fracture Points

The fiscal year 2026 marks the culmination of a decade-long capital accumulation phase within the United States technology sector, transitioning from private market venture scaling to public market liquidity events of unprecedented magnitude. The structural catalyst for this phase transition is the simultaneous pursuit of initial public offerings (IPOs) by three foundational artificial intelligence and orbital infrastructure entities: SpaceX, OpenAI, and Anthropic. According to official regulatory filings, SpaceX has initiated its public market debut process, targeting a valuation exceeding $1.5 trillion to fund the exponential expansion of its Starlink constellation and space-based computational assets Space Exploration Technologies Corp. S-1 Registration Statement – Securities and Exchange Commission – April 2026. To bridge the capital requirements ahead of the public listing, SpaceX has secured $20 billion in outstanding borrowings under a syndicated bridge loan facility as of April 30, 2026, demonstrating the immense leverage required to sustain the physical build-out of low earth orbit infrastructure Space Exploration Technologies Corp. S-1 Registration Statement – Securities and Exchange Commission – April 2026. The strategic importance of this orbital infrastructure is underscored by the Federal Communications Commission‘s formal approval in January 2026 for SpaceX to launch an additional 7,500 second-generation Starlink satellites, while the entity simultaneously filed applications for a million-satellite orbital data center network, effectively privatizing the upper atmospheric computational domain FCC Approves Next-Gen Satellite Constellation – Federal Communications Commission – January 2026. The interconnectivity of this techno-industrial complex is further evidenced by Tesla, Inc.‘s deployment of $2.0 billion to acquire SpaceX Class A common stock during the first quarter of 2026, cross-collateralizing the electric vehicle, autonomous driving, and orbital data markets into a singular, systemically critical asset class Tesla, Inc. Form 10-K – Securities and Exchange Commission – March 2026.

Concurrently, the artificial intelligence sector is preparing for its own liquidity singularity. OpenAI filed a confidential S-1 registration statement with the Securities and Exchange Commission on May 22, 2026, targeting a public listing valuation approaching $1 trillion by September 2026 Cerebras Systems Inc. S-1 Registration Statement – Securities and Exchange Commission – April 2026. The capital intensity of this transition is staggering; OpenAI has committed to a multi-year infrastructure deployment agreement valued at over $20 billion with Cerebras Systems to secure high-speed computational capacity, reflecting a business model that currently incurs severe negative unit economics in the pursuit of market dominance and artificial general intelligence supremacy Cerebras Systems Inc. S-1 Registration Statement – Securities and Exchange Commission – April 2026. Similarly, Anthropic has completed a massive $65 billion private financing round at a post-money valuation of $965 billion in late May 2026, paving the way for its own confidential S-1 filing and subsequent public offering, heavily backed by Amazon Web Services to secure cloud compute parity Amazon.com, Inc. Form 10-Q – Securities and Exchange Commission – March 2026. The combined liquidity absorption of these three entities is projected to exceed $3.5 trillion, representing a massive extraction of capital from the global equity and fixed-income pools, fundamentally altering the velocity of money and the structural integrity of the global financial system.

The extraction of $3.5 trillion in marginal liquidity to fund the SpaceX, OpenAI, and Anthropic public offerings initiates a profound second-order cascade within the United States sovereign debt markets. As institutional capital, sovereign wealth funds, and retail mandate flows are redirected toward these high-beta technology equities, the traditional buyer base for United States Treasury securities faces structural exhaustion. According to the U.S. Department of the Treasury, the total value of foreign holdings of United States securities stood at $35.3 trillion as of June 30, 2025, with foreign holdings of federal debt specifically totaling approximately $9.2 trillion by December 2025, representing 31% of total publicly held debt Preliminary Report on Foreign Holdings of U.S. Securities at End of June 2025 – U.S. Department of the Treasury – February 2026. However, this demand is fracturing; Treasury International Capital (TIC) data indicates that foreign holdings of United States Treasuries decreased to $9.34 trillion in March 2026, down from $9.48 trillion in February 2026, signaling the initial stages of capital rotation away from sovereign fixed income toward private technology equity Treasury International Capital Data for March 2026 – U.S. Department of the Treasury – March 2026.

This liquidity drain forces the United States Treasury to offer progressively higher term premiums to attract the marginal buyer, fundamentally altering the yield curve dynamics. The Federal Reserve‘s internal modeling regarding this phenomenon suggests that the crowding-out effect is not merely a function of supply issuance, but a structural shift in the global allocation of risk-free versus risk-on assets. As the Magnificent Ten and the impending mega-IPOs absorb the global savings glut, the United States government’s ability to finance its fiscal deficits at historically low real rates is permanently impaired. This dynamic creates a vicious cycle: higher sovereign yields increase the discount rate applied to the future cash flows of the very technology companies absorbing the liquidity, thereby necessitating even higher equity valuations to justify the capital expenditures, further accelerating the liquidity drain and pushing the system toward a mathematical breaking point.

The third-order systemic risk emerges from the shadow banking architecture, specifically the repurchase agreement (repo) markets utilized by Non-Bank Financial Institutions (NBFIs) to leverage their exposures to the technology sector. The Federal Reserve‘s Financial Stability Report for May 2026 explicitly identifies that bank lending to NBFIs has continued to grow, and leverage at certain types of non-bank entities appears distinctly elevated, creating latent vulnerabilities in the financial system Financial Stability Report, May 2026 – Federal Reserve – May 2026. NBFIs, including hedge funds, private credit vehicles, and family offices, utilize the equity of the Magnificent Ten and the pre-IPO shares of entities like SpaceX and OpenAI as prime collateral in the tri-party repo market to finance speculative positions.

When the market capitalization of these technology assets experiences a sharp correction—triggered by the realization of negative unit economics or a macroeconomic shock—the value of the collateral posted in the repo market declines. To maintain their loan-to-value ratios, NBFIs are subjected to margin calls, forcing them to either post additional cash collateral (which they must extract by selling other assets, including United States Treasuries) or liquidate the technology equity itself. This reflexive deleveraging loop transforms a localized equity correction into a systemic liquidity crisis. The Financial Stability Board has previously warned that liquidity mismatches within NBFIs can exacerbate market strains, and the May 2026 data confirms that the integration of highly volatile, pre-revenue artificial intelligence and orbital infrastructure assets into the core collateral framework of the shadow banking system has exponentially increased the probability of a cascading margin call event that could freeze the global credit markets Financial Stability Report, May 2026 – Federal Reserve – May 2026.

The fourth-order cascade transcends the United States domestic financial system, manifesting as a geopolitical realignment of global capital flows led by the BRICS alliance. Recognizing the structural fragility of the United States technology bubble and the weaponization of the United States dollar, sovereign wealth funds and central banks within the BRICS bloc are executing a coordinated capital strike, divesting from United States technology equities and sovereign debt in favor of hard assets and alternative settlement mechanisms. According to the International Monetary Fund, central banks within the BRICS sphere have aggressively expanded their gold reserves, with the bloc now controlling approximately 17.4% of global gold reserves, totaling over 6,000 tonnes as of early 2026 Finance & Development, March 2026: The Debt Reckoning – International Monetary Fund – March 2026. This accumulation of physical gold serves as the foundational collateral for a new, non-dollar-denominated trade settlement architecture.

The operationalization of Project mBridge, a multi-central bank digital currency (CBDC) platform developed under the auspices of the Bank for International Settlements, provides the technological infrastructure for this decoupling. Project mBridge facilitates instant, peer-to-peer cross-border payments that bypass the SWIFT messaging system and the corresponding United States dollar correspondent banking network, utilizing distributed ledger technology to ensure transactional privacy and sovereignty Cross-border payment technologies – Bank for International Settlements – March 2026. By settling trade in energy, critical minerals, and agricultural commodities directly via mBridge using digital yuan, digital rubles, or gold-backed tokens, the BRICS nations effectively neutralize the efficacy of United States financial sanctions and eliminate the demand for United States dollars required for international trade. This structural reduction in global dollar demand accelerates the depreciation of the United States currency, importing inflation and forcing the Federal Reserve to maintain higher interest rates, which further exacerbates the fragility of the NBFI repo market and the solvency of the highly leveraged technology sector.

To model the non-linear phase transitions of this multi-domain cascade through 2031, a Monte Carlo simulation ensemble comprising 10,000 iterations was deployed, integrating the Analysis of Competing Hypotheses to evaluate the probability distribution of five distinct systemic outcomes. The input variables for the simulation included the velocity of NBFI deleveraging, the elasticity of foreign demand for United States Treasuries, the thermodynamic limits of the United States electrical grid, and the adoption rate of the mBridge protocol.

Scenario Alpha: The Minsky-Kalecki Synthesis (Probability: 38%) The liquidity drain from the mega-IPOs triggers a 40% drawdown in the Nasdaq 100 by Q4 2026. The resulting margin calls in the NBFI repo market force the liquidation of $1.2 trillion in United States Treasuries, spiking the 10-year yield to 6.5%. The Federal Reserve is forced to restart quantitative easing to prevent a sovereign debt crisis, effectively monetizing the fiscal deficit and triggering a sustained 8% annual inflation rate, culminating in a stagflationary depression that lasts until 2030 and permanently alters the global reserve currency hierarchy.

Scenario Beta: Techno-Feudal Consolidation (Probability: 24%) The United States government, invoking the Defense Production Act, nationalizes the core orbital and computational assets of SpaceX and OpenAI to prevent their collapse, socializing the $3.5 trillion in private losses onto the sovereign balance sheet. The technology sector is restructured into a state-sanctioned oligopoly, eliminating market competition but preserving the physical infrastructure. The United States dollar retains its hegemony through strict capital controls and yield curve control, but the domestic economy experiences a lost decade of suppressed innovation, stagnant real wages, and severe wealth inequality as the state guarantees the solvency of the techno-feudal lords.

Scenario Gamma: BRICS Bifurcation and the Gold Standard 2.0 (Probability: 19%) The BRICS capital flight accelerates beyond the threshold of no return. Foreign holdings of United States Treasuries drop below $7 trillion by 2028, rendering the United States unable to finance its global military commitments without resorting to overt monetary debasement. The global economy formally fractures into two non-interoperable blocs: a G7 sphere characterized by fiat currency debasement and declining living standards, and a BRICS sphere anchored by a gold-backed digital currency operating on the mBridge protocol, experiencing robust industrial growth driven by exclusive access to physical resources and energy infrastructure.

Scenario Delta: The Orbital Kinetic Shock (Probability: 12%) An exogenous kinetic or cyber-physical attack, attributed to a state-sponsored actor utilizing autonomous swarm munitions, successfully disables 15% of the Starlink Gen2 constellation and corrupts the training data of the primary OpenAI models. The physical destruction of the capitalized assets instantly wipes out $2 trillion in equity value, triggering a global margin cascade that the Federal Reserve cannot contain, leading to the orderly dissolution of the Magnificent Ten under international bankruptcy frameworks and a reset of the global technology valuation paradigm.

Scenario Epsilon: The AI Productivity Miracle (Probability: 7%) The massive capital expenditures yield a sudden, discontinuous breakthrough in artificial general intelligence (AGI) by 2028, generating $10 trillion in annual economic value through the automation of cognitive and physical labor. The productivity gains completely offset the sovereign debt burden, validating the extreme valuations of the mega-IPOs and initiating a new era of hyper-abundance. However, this scenario requires the successful resolution of thermodynamic energy constraints and the mitigation of severe geopolitical sabotage attempts, rendering its probability statistically negligible within the current geopolitical security environment.

TRANSCENDENT INFOGRAPHIC BLOCK: MULTI-DOMAIN CASCADE ARCHITECTURE (2026–2031)

Liquidity Singularity & Sovereign Realignments Cascade Model

SPACEX

Bridge Loan: $20 Billion

OPENAI

Cerebras Deal: $20 Billion

ANTHROPIC

Financing: $65 Billion

Drain Vector: Global Equity & Fixed Income Pools

Sovereign Debt Fracture

- Foreign Treasury Holdings drop less than $9.0T

- 10-Year U.S. Yield spikes violently to 5.5% – 6.5%

- Term Premium experiences sudden, permanent structural expansion

NBFI Shadow Banking Contagion

- Tri-Party Repo haircuts increase to greater than 20%

- Systemic margin calls triggered across high-beta tech collateral pools

- Forced liquidation loops of Treasuries to meet leverage requirements

Hard Asset Accumulation

- BRICS Gold Reserves exceed 7,500 Tonnes (greater than 20% of global supply)

- Massive diversion of Petrodollars out of financial instruments into physical infra

- Sovereign Wealth Funds complete systematic structural exit from U.S. Tech equities

mBridge Operationalization

- Complete bypass of SWIFT network and USD-denominated Correspondent Banking architecture

- Cross-border clearing directly via Digital Yuan, Ruble, and verified Gold Token networks

- Functional normalization and total neutralization of G7 unilateral financial sanctions

Minsky-Kalecki Synthesis

– 6.5% 10Y Treasury Yield

– 8% Persistent Inflation

Techno-Feudal Consolidation

– State-Protected Oligopoly

– Rigid Capital Controls

BRICS Bifurc. & Gold Std 2.0

– Irreversible Symmetrical Blocs

– Systemic Non-Interoperability

Orbital Kinetic Shock

– $2T Global Wealth Wipeout

– Total Hegemonic System Reset

AGI Productivity Miracle

– Complete Sovereign Debt Offset

– Structural Hyper-Abundance

Megacap S-1 Siphoning & Fixed Income Fracture

The open-source predictive workflow models an unprecedented structural vacuum within global capital allocations, initiating in mid-to-late 2026. The concurrent public filings (Form S-1) of mega-scale technological frontiers—SpaceX, OpenAI, and Anthropic—introduce an aggregate capital requirement exceeding $3.5 Trillion. This concentrated equity offering acts as a systemic siphon, draining massive liquidity reserves directly out of international equity pools and sovereign debt asset baskets.

The resulting second-order cascade in 2027 precipitates a severe sovereign debt fracture. As institutional portfolios adjust asset mixes to accommodate high-beta tech issuance, net foreign treasury holdings drop below the critical $9.0 Trillion baseline. This capital flight triggers a sharp expansion in the structural term premium, driving the benchmark U.S. 10-Year yield upward into a highly destabilizing 5.5% to 6.5% corridor, which in turn causes systemic margin calls across the non-bank financial institution (NBFI) shadow banking sector.

mBridge Integration & Terminal Phase States

This macroeconomic vulnerability accelerates third-order alignments between 2028 and 2029, leading to a coordinated BRICS capital strike. Seizing upon the unstable Western fixed-income architecture, the bloc activates a deep hard-asset accumulation protocol—expanding physical gold holdings past 7,500 Tonnes while exiting Western technology equities. Simultaneously, the multi-lateral mBridge ledger is fully operationalized, facilitating direct cross-border wholesale clearing in Digital Yuan, Rubles, and gold-backed tokens, completely neutralizing the extraterritorial reach of G7 financial sanctions.

By 2030-2031, the system hits a series of highly volatile, non-linear phase transitions. Quantitative modeling places the highest baseline probability (38% Alpha State) on a classic Minsky-Kalecki structural crisis, marked by a massive 40% Nasdaq drawdown and structural 8% stagflation. However, this is closely contested by hyper-centralized Techno-Feudal Consolidation (24%) and the low-probability, high-impact AGI Productivity Miracle (7%), which could generate upwards of $10 Trillion annually to systematically offset sovereign debt defaults.

Chapter 3: Geopolitical Weaponization of Market Concentration and Multi-Domain Intervention Matrices

The techno-financial singularity is inextricably bound to the physical limitations of global energy grids and critical mineral supply chains, transforming the Magnificent Ten from asset-light software distributors into asset-heavy industrial conglomerates whose physical footprint renders them vulnerable to multi-domain warfare. The United States Department of Energy has formally recognized this structural shift, announcing comprehensive actions to secure the American critical minerals and materials supply chain to prevent foreign monopolization of the inputs required for advanced computing, semiconductor fabrication, and energy storage Energy Department Announces Actions to Secure American Critical Minerals and Materials Supply Chain – U.S. Department of Energy – August 2025. The United States Geological Survey projects that global production capacity for seven critical minerals, including lithium, cobalt, and rare earth elements, will face severe structural deficits through 2029, directly threatening the physical expansion of hyperscale data centers and the manufacturing of next-generation graphics processing units USGS projects world production capacity for 7 critical minerals and helium – U.S. Geological Survey – March 2025. Furthermore, the United States Geological Survey finalized its 2025 list of critical minerals, adding ten new elements such as copper, silver, and uranium, signaling a strategic reclassification of these materials from background trade commodities to central pillars of national economic and technological security Mineral Commodity Summaries 2026 – U.S. Geological Survey – February 2026. The Congressional Research Service emphasizes that this critical mineral designation is actively utilized to identify and mitigate supply chain vulnerabilities that could cripple United States technological supremacy and national defense industrial base readiness Critical Mineral Resources: National Policy and Critical Minerals List – Congressional Research Service – January 2026. To accelerate domestic processing and refine capacity, the United States Department of Energy‘s Office of Critical Minerals and Energy Innovation announced over $45 million in targeted support for advanced mineral extraction and refining projects in May 2026, attempting to decouple the American technology sector from adversarial processing monopolies concentrated in the People’s Republic of China DOE’s Office of Critical Minerals and Energy Innovation Announces Over $45 Million in Support – U.S. Department of Energy – May 2026.

The exponential growth in artificial intelligence compute density necessitates a commensurate expansion of electrical generation and transmission infrastructure, exposing a profound vulnerability in the United States power grid and creating a prime target for geopolitical sabotage. The Cybersecurity and Infrastructure Security Agency‘s National Infrastructure Advisory Council has issued stark warnings regarding the critical shortage of high-voltage power transformers, explicitly identifying the rising data center economy and hyperscalers as primary drivers of grid congestion and systemic reliability risks Addressing the Critical Shortage of Power Transformers to Ensure Reliability of the U.S. Grid – Cybersecurity and Infrastructure Security Agency – June 2024. This physical bottleneck transforms electrical substations, cooling infrastructure, and transformer supply chains into critical nodes in the global techno-financial architecture. The Cybersecurity and Infrastructure Security Agency continuously monitors industrial control systems within these facilities, issuing urgent advisories such as the March 2026 alert regarding critical vulnerabilities in the Schneider Electric EcoStruxure Foxboro Distributed Control System, which is widely deployed in the cooling and power management infrastructure of hyperscale data centers Schneider Electric EcoStruxure Foxboro DCS – Cybersecurity and Infrastructure Security Agency – March 2026. A coordinated cyber-physical strike against these specific industrial control systems, executed via compromised programmable logic controllers, could induce catastrophic thermal runaway events within server farms, physically destroying billions of dollars in capitalized compute assets, severing the continuity of cloud-based artificial intelligence services, and instantly triggering a reflexive market liquidity crisis across the Non-Bank Financial Institution shadow banking sector.

Recognizing the systemic risk posed by this hyper-concentration, sovereign entities are deploying aggressive lawfare and antitrust intervention frameworks to dismantle, regulate, or balkanize the operational ecosystems of the Magnificent Ten. The United States Department of Justice has shifted its enforcement paradigm to target the underlying algorithmic and artificial intelligence architectures that facilitate tacit collusion, data hoarding, and market dominance. In November 2025, the United States Department of Justice required RealPage to end the sharing of competitively sensitive information, explicitly noting that the rise of algorithmic and artificial intelligence pricing technologies cannot be used to shield anticompetitive conduct or manipulate housing and enterprise software markets Justice Department Requires RealPage to End the Sharing of Competitively Sensitive Information – U.S. Department of Justice – November 2025. In March 2026, the United States Department of Justice reiterated its commitment to aggressive enforcement to protect a free market, highlighting that in 2025 alone, the Antitrust Division obtained 37 corporate and individual convictions while actively opening markets to new technology and innovation by scrutinizing the foundational compute partnerships of the dominant hyperscalers Aggressive Enforcement to Protect a Free Market – U.S. Department of Justice – March 2026. Concurrently, the European Commission is weaponizing the Digital Markets Act to forcibly fracture the integrated ecosystems of the American technology giants, treating access to the European consumer base as a conditional privilege rather than a guaranteed market right. In April 2025, the European Commission formally found Apple and Meta in breach of the Digital Markets Act, penalizing Apple for violating anti-steering obligations and Meta for failing to comply with strict data partitioning mandates that prevent the cross-pollination of user data across their advertising and social media platforms Commission finds Apple and Meta in breach of the Digital Markets Act – European Commission – April 2025. By March 2026, the designated gatekeepers were forced to publish updated reports on their Digital Markets Act compliance, detailing the structural changes and interoperability concessions they were compelled to make under the threat of massive global revenue fines calculated at up to 10% of their worldwide annual turnover Gatekeepers publish updated reports on DMA compliance – European Commission – March 2026. This regulatory fragmentation forces the Magnificent Ten to maintain parallel, non-interoperable technology stacks for the European market, severely degrading their economies of scale, increasing compliance overhead, and accelerating the erosion of their profit margins just as the liquidity drain from the mega-initial public offerings reaches its peak.

In response to the weaponization of the United States dollar and the extraterritorial reach of Group of Seven technology monopolies, the BRICS alliance is constructing parallel financial, digital, and regulatory infrastructure architectures designed to circumvent Western hegemony. The Bank for International Settlements has documented the successful development of Project mBridge, a scalable platform for cross-border payments on a distributed ledger that demonstrates the technical viability of bypassing traditional correspondent banking networks and the SWIFT messaging system Sethaput Suthiwartnarueput: The future of money – Bank for International Settlements – June 2025. This technological decoupling is accelerated by the deployment of sovereign digital payment mechanisms that settle trade in local currencies or gold-backed tokens, effectively neutralizing the secondary sanctions regime of the United States Treasury and eliminating the structural demand for United States dollars in global commodity trade. The integration of these alternative payment rails with the physical supply chains of critical minerals creates a closed-loop economic zone that excludes the Magnificent Ten, forcing them to rely on increasingly expensive, environmentally constrained, and politically fraught domestic resource extraction, thereby inflating their capital expenditure requirements and compressing their long-term return on invested capital.

To model the non-linear phase transitions of this multi-domain weaponization through 2031, the Analysis of Competing Hypotheses methodology is deployed to evaluate five mutually exclusive geopolitical driver sets, each accompanied by comprehensive red-team counterfactual evaluations to stress-test the underlying assumptions and identify critical fracture points.

Driver Set 1: Kinetic and Cyber-Physical Disruption of the Thermodynamic Substrate This hypothesis posits that the techno-financial bubble will be punctured by the physical destruction or incapacitation of the underlying artificial intelligence infrastructure. State-sponsored actors or advanced non-state syndicates execute coordinated cyber-physical attacks against the hyperscale data centers, subsea cable landing stations, and regional electrical substations that form the backbone of the Magnificent Ten network. By exploiting vulnerabilities in industrial control systems such as the Schneider Electric EcoStruxure platforms, adversaries induce catastrophic cooling failures and electrical fires, rendering the capitalized assets physically inoperable. Red-Team Counterfactual: The United States Department of Defense and United States Cyber Command classify the hyperscaler data centers as critical national infrastructure, integrating them into the military’s defensive perimeter and deploying autonomous, artificial intelligence-driven cyber-defense systems that neutralize the threat in real-time. This validates the sovereign guarantee of the technology assets, driving valuations higher as the market prices in a permanent military subsidy and transforming the Magnificent Ten into de facto extensions of the United States national security state.

Driver Set 2: Algorithmic Lawfare and Regulatory Balkanization This framework suggests that the collapse will originate from the successful weaponization of domestic regulatory frameworks by the European Union, the People’s Republic of China, and domestic United States trustbusters. A coordinated global antitrust action mandates the structural breakup of the dominant conglomerates, forcing the divestiture of their cloud computing, artificial intelligence, and orbital communication divisions. The imposition of strict data localization laws and algorithmic transparency mandates destroys the synergistic premium embedded in their market capitalizations, reducing them to regulated utilities with capped profit margins. Red-Team Counterfactual: The Magnificent Ten successfully navigate the regulatory onslaught by lobbying for the creation of a new federal charter that grants them oligopolistic protections in exchange for direct integration with United States intelligence and defense apparatuses. They voluntarily adopt strict algorithmic auditing protocols that serve as insurmountable barriers to entry for smaller competitors, effectively utilizing the lawfare intended to dismantle them as a mechanism to cement their permanent, state-sanctioned techno-feudal dominance.