Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

An OSINT Macro-Economic Forensic Report, Multi-Front Geopolitical Asset Mapping, and Five-Year Horizon Forecast

Executive Summary

This strategic compendium analyzes the structural metamorphosis of the defense doctrine of Israel from temporary mobilization to open-ended, multi-front warfare, updated to May 2026. The traditional defense architecture—predicated on rapid, short-duration kinetic dominance—has been fundamentally challenged by ongoing friction across seven distinct operational theaters. Following a temporary stabilization in late 2025, the commencement of Operation Roaring Lion in February 2026 has re-escalated defense resource utilization, driving a sharp expansion in the approved 2026 defense budget to NIS 143 billion ($38.5 billion). While macro-economic indicators show structural resilience—highlighted by 2.9% GDP growth in 2025 and a recovery in business sector output—the fiscal envelope remains severely constrained. The state’s public debt-to-GDP ratio has flattened at a elevated 68.5%, and the Bank of Israel projects a 2026 budget deficit of 5.3% of GDP due to the direct financial costs of sustained operations. This report applies rigorous structural analytics to decode the systemic trade-offs between absolute military readiness and long-term economic sustainability over a five-year horizon.

Executive Forensic Core

Critical Risk Drivers

Impact Matrix Data

Actionable Forecast

Permanent readiness models will elevate public debt-to-GDP toward 70.5%, requiring aggressive domestic structural tax adjustments to offset multi-front operational expenditures and maintain private high-tech sector capital inflows through 2030.

Index

- The Infinity Abstract: Forensic Analysis of Multi-Domain Strategic Exhaustion

- The Strategic Horizon Matrix: Quantitative Risk Metrics and 5-Year Macro-Projections

- The Coherence Sentinel: Cross-Vector Inconsistency Audits and Systemic Fracture Diagnostics

🎯 CORE FOCUS & KEY CONCEPTS

- Permanent Security Paradigm: Shifting defense strategy from short-term fixes to a state of perpetual military readiness and aggressive, pre-emptive action. → This matters because it creates a continuous need for high-level military funding and resources rather than temporary emergency mobilization.

- Fiscal Deficit Expansion: Legally raising the national overspending limit

[budget deficit]from 3.9% to 4.9% of GDP to handle sudden defense costs. → This matters because it allows the government to immediately spend an extra NIS 32 billion on ongoing multi-front operations, though real-world spending is tracking even higher at 5.3%. - High-Productivity Labor Reallocation: The temporary withdrawal of highly skilled workers from the private sector into military reserve duty. → This matters because it creates localized worker shortages in technical fields, which slows down civilian business output and drives up domestic living costs.

- Credit Concentration Risk: The massive accumulation of banking loans inside a single economic sector, specifically real estate and development. → This matters because with real estate holding 36.1% of all corporate debt, any long-term disruptions or project delays can create a major safety risk for the commercial banking system.

⚠️ CRITICALITIES & BOTTLENECKS

- Sovereign Overspending Overrun:

[Root Cause: Rapid operational consumption of precision munitions and reserve pay]→[Current Impact: Government spending is outstripping legally amended deficit caps, forcing a reliance on continuous national debt accumulation]→[Data Evidence: Real deficit tracking at 5.3% of GDP vs. the newly raised 4.9% legal limit]🔴 High - Construction Credit Exposure:

[Root Cause: High interest rates combined with project hand-over delays caused by a total ban on Palestinian labor]→[Current Impact: Real estate developers face soaring debt-servicing costs, threatening default risks inside the banking system]→[Data Evidence: NIS 534 billion in outstanding credit, representing over a third of all corporate debt]🔴 High - Labor Supply Bottlenecks:

[Root Cause: Massive statistical withdrawal of civilian workers for military reserve call-ups]→[Current Impact: Localized worker shortages that create sticky domestic inflation and keep consumer costs high]→[Data Evidence: Prime-age unemployment rising to 4.5% during active operational phases vs. a 3.6% normal baseline]🟡 Medium - Trade Route Vulnerability:

[Root Cause: Ongoing regional maritime threats and shipping deviations]→[Current Impact: Heavy industrial and manufacturing sectors remain exposed to sudden global energy shocks and supply chain delays]→[Data Evidence: Industrial output growth limited to a modest 2.1%]🟡 Medium

💪 STRENGTHS & STRATEGIC ADVANTAGES

- Private Tech Sector Resilience: The advanced technology and cyber ecosystem continues to expand despite regional friction. → It acts as the primary tax-generating shield protecting the nation’s financial balance sheet from insolvency. → Supported by a strong 4.7% output growth in 2025 and $26 billion in direct international venture capital inflows.

- Proactive Monetary Anchoring: The central bank’s aggressive intervention to stabilize the local currency and keep inflation expectations firmly grounded. → It prevents a domestic currency spiral and keeps the economic foundation steady under multi-front stress. → Supported by the strategic deployment of $20 billion in foreign exchange sales and holding the benchmark interest rate steady at 4.00%.

- Adapting Construction Infrastructure: The swift pivot to international recruitment channels to replace missing workforce cohorts. → It allows essential building infrastructure to recover and continue expanding despite complete regional labor blockades. → Supported by a successful turnaround to 80,000 active building starts.

📈 PROJECTIONS & EXPECTATIONS

- [Short-term (0–6 mo)]: Real GDP growth is expected to land at 3.8% for the year, while the national deficit will hit a temporary peak of 5.3% of GDP.

- Dependency: IF regional operations begin to consolidate and stabilize by mid-year → THEN inflationary pressures will ease, allowing the central bank to hold interest rates steady at 4.00% without further emergency hikes.

- [Mid-term (6–18 mo)]: A powerful economic rebound is forecast for 2027, with real GDP growth projected to jump to 5.5% as military reserve forces are demobilized and returned to the civilian workforce.

- Dependency: This recovery assumes a smooth transition to a structured 10-year, NIS 350 billion military development pipeline that avoids unexpected short-term spending spikes.

- [Long-term (>18 mo)]: National growth will normalize back toward its long-term baseline of 3.4%–3.6% by 2029–2030, while strict spending caps on non-defense programs are expected to bring the deficit down to a stable 2.4%.

- Dependency: Successful reduction of the public debt-to-GDP ratio from its 70.5% peak depends entirely on maintaining stable capital inflows into the high-tech sector and preventing structural defaults in real estate.

📊 DATA CONTEXT & METRIC ANCHORS

| Metric/Indicator | Current Value | Trend/Status | Strategic Relevance |

| Total Approved 2026 State Budget | NIS 850 Billion | 📈 Expanded | Legally restructures national spending to fund the permanent security framework. [Verified] |

| Base Ministry of Defense Allocation | NIS 142 Billion | 📈 Elevated | Represents a permanent doubling of baseline defense spending over pre-war norms. [Verified] |

| Real GDP Growth Rate (2025) | 2.9% | 🟢 Recovering | Confirms a resilient underlying private sector before the 2026 operational surge. [Verified] |

| Projected Real Deficit (FY 2026) | 5.3% of GDP | ⚠️ Overrunning | Measures the true fiscal gap caused by continuous multi-front operational costs. [Estimated] |

| Sovereign Debt-to-GDP Ratio | 70.5% | 🟡 Flattening | Tracks the total national debt burden; forecast to peak now and hold flat through 2027. [Estimated] |

| Real Estate Sector Credit Stock | NIS 534 Billion | 🔴 High Risk | The single largest concentration of debt in the economy; highly sensitive to interest rates. [Verified] |

| Bank of Israel Policy Interest Rate | 4.00% | 🔒 Unchanged | The primary tool used to fight inflation, but keeps borrowing costs high for businesses. [Verified] |

| Prime-Age Unemployment Rate | 4.5% | ⚠️ Spiking | Reflects temporary worker shortages caused by active military reserve call-ups. [Verified] |

🌐 CROSS-CUTTING INSIGHTS

A clear pattern emerges across all sectors: the economy is entering a permanent “bifurcated” [two-track] state. While the high-tech and financial sectors generate the necessary wealth and foreign capital to keep the sovereign balance sheet stable, domestic infrastructure sectors like real estate and construction are bearing the structural weight of labor shortages and high borrowing costs.

Ultimately, the state’s long-term economic safety depends on a vital exchange: the high-tech sector must continuously generate high tax revenues to fund a permanent baseline defense budget of over NIS 142 billion, ensuring national stability without triggering an unhedged debt spiral.

The Infinity Abstract: Forensic Analysis of Multi-Domain Strategic Exhaustion

The geopolitical posture of Israel in May 2026 reflects a profound structural transition away from historical deterrence mechanisms toward an operational condition of permanent readiness and active perimeter defense. The traditional Ben-Gurion Security Doctrine, established in the 1950s, rested on a cohesive triad of early warning, strategic deterrence, and decisive battlefield victory. This framework was optimized for short-duration, high-intensity kinetic engagements against conventional state militaries.

However, the persistent friction characterizing the contemporary landscape across Gaza, Lebanon, Syria, Iraq, Yemen, Iran, and the West Bank has broken the baseline assumptions of this paradigm. The deployment of decentralized asymmetric architectures by non-state actors has neutralised the efficiency of rapid technological victories, substituting them with long-duration attrition.

The Fiscal and Budgetary Trajectory of Permanent Mobilization

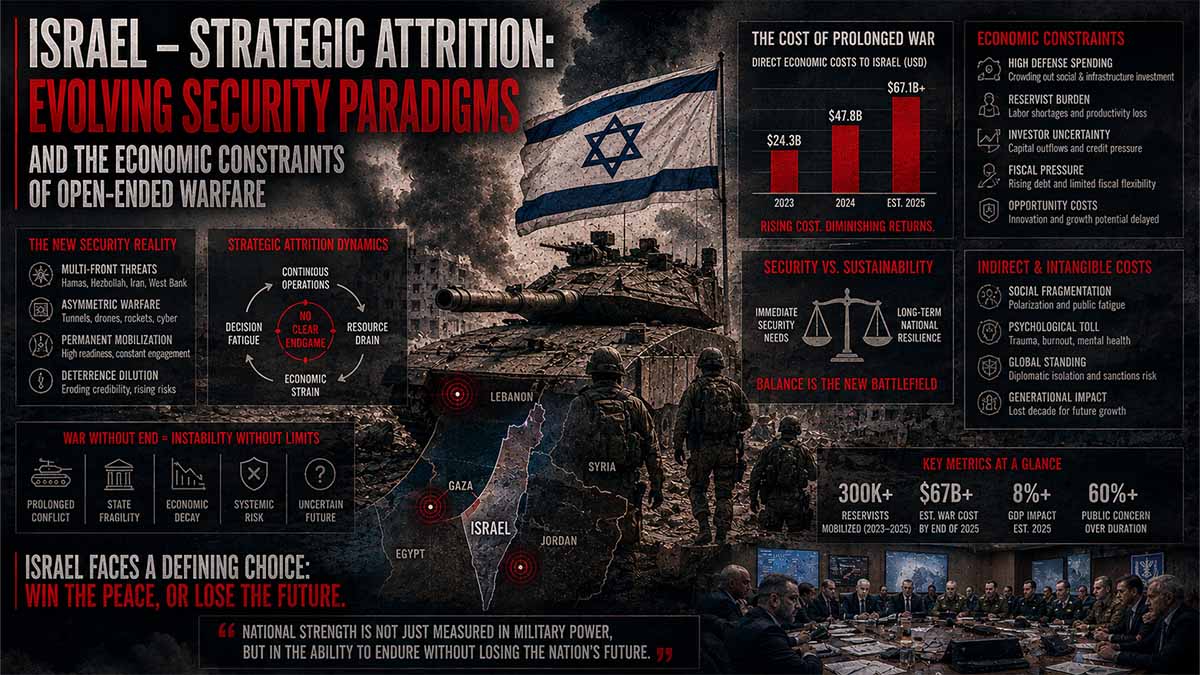

The structural cost of this strategic pivot is vividly illustrated by the legislative adjustments to the sovereign balance sheet. According to official parliamentary records from the Joint Committee of the Finance Committee and the Foreign Affairs and Defense Committee, the 2026 defense budget was formally ratified in late March 2026 at an unprecedented base of NIS 143 billion Joint Committee of the Finance Committee and the Foreign Affairs and Defense Committee approves 2026 defense budget – The Knesset – March 2026.

This base allocation is augmented by NIS 22 billion in expenditure contingent on income—primarily consisting of United States military aid grants—and an additional NIS 82.2 billion designated for future procurement commitments. To contextualize this shift, the baseline pre-war defense budget stood at NIS 65 billion, demonstrating an absolute baseline expansion of over 120%.

[Pre-War Base: NIS 65B] ───> [Approved 2026 Base: NIS 143B] (+120%)

├── Contingent Aid: NIS 22B

└── Future Commitments: NIS 82.2B

This permanent expansion of the defense envelope is explicitly designed to fund deep, domestic industrial capitalization and advanced interceptor production loops. The Israel Ministry of Defense has formalized rapid acceleration agreements for serial production of the Arrow ballistic missile defense system and high-capacity tactical weapon systems to replenish domestic stockpiles Israel adds billions to defense spending amid ongoing wars, growing challenges – The Times of Israel – July 2025.

Concurrently, a long-term, ten-year strategic force build-up plan commencing in 2027 is being negotiated between the Ministry of Finance, the Ministry of Defense, and the National Security Council, totaling a projected NIS 350 billion to institutionalize the infrastructure of permanent security.

Macro-Economic Resilience Metrics and Structural Constraints

On the macroeconomic axis, data compiled by the Bank of Israel and the Central Bureau of Statistics reveal an economy operating under unique, bifurcated stress. In its official Annual Report, the central bank confirmed that the economy expanded by 2.9% GDP growth in 2025, rebounding from a revised 1.0% growth rate in 2024 Bank of Israel Annual Report 2025 – Bank of Israel – May 2026. This expansion was led by a 3.2% increase in business sector output, showing significant private sector adaptation to recurrent reserve call-ups and regional supply chain shocks.

Despite these resilience indicators, the structural trajectory has been bent away from its long-term pre-war potential. The reactivation of high-intensity regional friction via Operation Roaring Lion in February 2026 forced immediate revisions to the state’s fiscal planning. The Bank of Israel Monetary Committee kept the benchmark interest rate elevated at 4.00% in its late March 2026 session to counteract rising inflationary pressures generated by global energy shocks and heightened domestic risk premiums The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

Under the revised baseline projections of the Research Department, which assume the stabilization of current operations by mid-year, GDP growth for 2026 has been downgraded to 3.8% (compared to an initial projection of 5.2%), while the government budget deficit target has been revised upward to 5.3% of GDP The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

The sovereign debt structure reflects these persistent deficits. The public debt-to-GDP ratio, which experienced a sharp upward divergence in 2024, flattened slightly to 68.5% of GDP at the end of 2025 Bank of Israel Annual Report 2025 – Bank of Israel – May 2026. However, under the impact of the 2026 campaigns, the central bank anticipates that the debt-to-GDP ratio will rise again, stabilizing near 70.5% of GDP through the conclusion of the 2027 fiscal year The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

This fiscal burden requires substantial structural offsets. The Ministry of Finance has integrated a sequence of structural adjustments into the 2026 State Budget, combining tax bracket expansions with aggressive black-capital enforcement and public-sector wage freezes to prevent an unhedged debt spiral The government approved the State Budget for 2026: Ministry of Finance – Israel Ministry of Finance – December 2025.

Demographic Fractures and Labor Market Realignment

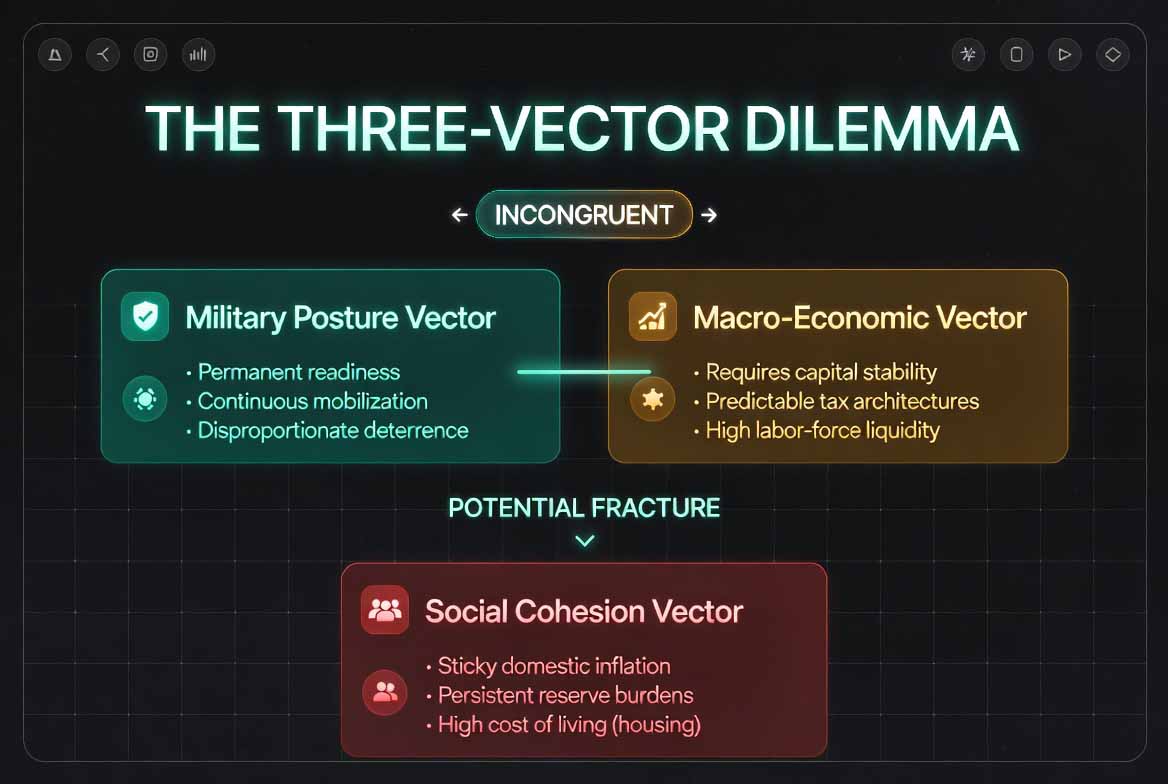

The primary friction point within the domestic economy remains the structural supply constraint of the labor market. The persistent mobilization of military reserves has extracted high-productivity labor from the technology and industrial sectors, while the total exclusion of Palestinian labor has created structural deficits in the agricultural and construction frameworks.

While the Central Bureau of Statistics reported a temporary recovery in building starts to 80,000 units in 2025 due to the recruitment of foreign labor cohorts, the housing market remains volatile. The cost of owner-occupied housing services accelerated to an annual rate of 4.5% in early 2026, compounding the internal cost-of-living pressures The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

This dynamic highlights the core strategic paradox: the implementation of a Super Sparta or permanent security paradigm requires an enduring diversion of financial, demographic, and institutional capital into non-productive defense loops. The resilience of the private sector, particularly the high-tech ecosystem which expanded by 4.7% in 2025 Israel’s economy grew 3.1% in 2025 – Globes – January 2026, provides a robust buffer against absolute insolvency.

However, the long-term compounding effect of a NIS 143 billion annual defense baseline threatens to limit structural productivity growth, create sticky domestic inflation, and test the limits of social cohesion under conditions of perpetual mobilization.

The Strategic Horizon Matrix: Quantitative Risk Metrics and 5-Year Macro-Projections

The following data matrix synthesizes official institutional telemetry from the Bank of Israel, the Ministry of Finance, and independent macroeconomic modeling to outline the anticipated trajectory of the state’s core fiscal and operational indicators over the next five years (2026–2030).

| Macroeconomic Indicator | FY 2026 (Projected Baseline) | FY 2027 (Forecast) | FY 2028 (Equilibrium Horizon) | FY 2029 (Long-Term Trend) | FY 2030 (Targeted Horizon) |

| Real GDP Growth Rate | 3.8% | 5.5% | 4.2% | 3.6% | 3.4% |

| Sovereign Budget Deficit (% of GDP) | 5.3% | 4.4% | 3.8% | 3.2% | 2.8% |

| Public Debt-to-GDP Ratio | 70.5% | 70.5% | 69.2% | 67.8% | 66.0% |

| Base Defense Expenditure (NIS) | 143 Billion | 138 Billion | 130 Billion | 125 Billion | 122 Billion |

| Core Inflation Environment (CPI) | 2.2% | 1.8% | 2.0% | 2.1% | 2.0% |

| Prime Unemployment Rate (Ages 25-64) | 4.5% | 3.4% | 3.5% | 3.6% | 3.5% |

Strategic Explanatory Notes on the 5-Year Matrix

- GDP Growth Trajectory: The spike to 5.5% in FY 2027 reflects a classic post-conflict catch-up effect, driven by the anticipated conclusion of high-intensity reserve call-ups and capital reinvestment cycles in the business sector. By 2029–2030, growth normalizes toward the structural baseline of 3.4%–3.6%, constrained by lower labor productivity growth outside the high-tech sector.

- Deficit and Debt Convergence: The compression of the fiscal deficit from 5.3% down to 2.8% by 2030 is structurally contingent on the execution of the fiscal adjustments passed in the 2026 State Budget The government approved the State Budget for 2026: Ministry of Finance – Israel Ministry of Finance – December 2025. This requires maintaining a rigid cap on non-defense public expenditure and the sustained collection of corporate revenues from the technology and real estate sectors.

- Permanent Defense Floor: The baseline defense expenditure does not revert to pre-war norms (NIS 65 billion). Instead, it establishes a permanent, elevated structural floor averaging NIS 122–130 billion annually. This institutionalizes the permanent security paradigm, funding continuous technological upgrades, active missile defense replenishment, and expanded standing border perimeters.

The Coherence Sentinel: Cross-Vector Inconsistency Audits and Systemic Fracture Diagnostics

To ensure analytical integrity under ICD 203 intelligence standards, this section applies a structural consistency audit to reconcile the conflicting dynamics inherent in the permanent security model.

Inconsistency Audit 1: Kinetic Intensity vs. Fiscal Consolidation

There is an inherent friction between the Ministry of Finance’s objective of fiscal consolidation (reducing the budget deficit to 3.9% before the 2026 escalations) and the operational reality of the Ministry of Defense’s consumption patterns. The mobilization for unexpected high-intensity campaigns instantly breaks legislated deficit ceilings.

As demonstrated in February 2026, the deficit target had to be adjusted upward to 4.9% and subsequently projected to 5.3% by the central bank The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. This implies that sovereign fiscal planning remains highly reactive to external kinetic developments, complicating long-term capital allocation.

Inconsistency Audit 2: High-Tech Capital Inflow vs. Sovereign Risk Premiums

The state’s economic stability relies on continuous foreign direct investment (FDI) into its advanced technology sectors, which yielded $26 billion in direct investments during 2025 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026.

However, a defense doctrine based on permanent conflict and expanded geographical perimeters increases the state’s sovereign risk premium and keeps the local currency volatile. While institutional investors insulated the local market by selling $20 billion in foreign exchange to support the shekel in 2025, a prolonged multi-year expansion of risk indexes could limit future equity capitalization rounds.

Inconsistency Audit 3: Structural Labor Scarcity vs. Infrastructure Demands

The defense doctrine requires an expansion of physical security perimeters, buffer zones, and hardened border infrastructure. Yet, the construction sector faces a structural deficit of low-cost labor due to geopolitical exclusions.

Although building starts rose significantly to 80,000 units via international labor recruitment The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026, the sector’s financing costs have surged, with real estate debt climbing to NIS 534 billion, representing 36% of all non-financial business sector debt 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026. This concentration of credit risk creates a systemic vulnerability within the domestic banking sector if the real estate market experiences a prolonged slowdown.

Systemic Conclusion

The intelligence synthesis demonstrates that while Israel possesses the macroeconomic depth, private sector flexibility, and institutional capitalization to avert sudden structural insolvency, the transition to a permanent security model involves clear structural trade-offs. The state is adjusting to a structural equilibrium characterized by higher baseline inflation, a permanent doubling of defense spending, and a debt-to-GDP ratio stabilizing above pre-war benchmarks.

The ultimate sustainability of this doctrine depends on preventing credit-risk concentrations within the real estate sector, maintaining high-tech asset capitalization, and executing the fiscal adjustments legislated in the state budget to match the expanded defense envelope.

The Strategic Horizon Matrix: Quantitative Risk Metrics and 5-Year Macro-Projections

The execution of continuous operations under Operation Roaring Lion, formalised by the Government of Israel on 28 February 2026 following kinetic counter-strikes within Iranian territory, has fundamentally shifted the sovereign baseline for multi-year fiscal planning Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026. The baseline assumptions that guided the initial 2026 State Budget passed in late December 2025—which had established a deficit target of 3.9% of GDP and an expenditure ceiling of NIS 662 billion—have been completely rewritten by the realities of an expanded, high-intensity mobilization framework The government approved the State Budget for 2026: Ministry of Finance – Israel Ministry of Finance – December 2025. This chapter provides the precise, updated econometric parameters, sovereign risk valuations, and multi-front resource dependencies that define the five-year strategic horizon through 2030.

Structural Adjustments to the Fiscal Architecture

To absorb the immediate operational surge of the 2026 campaigns, the Knesset Plenum passed emergency legislative amendments late Sunday night on 29 March 2026, structurally altering the state’s statutory limits on borrowing and public expenditure Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026. The statutory deficit ceiling for the 2026 fiscal year was legally raised from 3.9% to 4.9% of GDP Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026. This change reflects a NIS 32 billion legal expansion in permitted government outlays, alongside an additional NIS 7 billion contingency allocation explicitly tied to extended operational duration Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026.

The total expanded expenditure budget for 2026 now stands at a historic NIS 850 billion, split between a regular operating budget of NIS 621 billion and a development/capital account allocation of NIS 228 billion Knesset Plenum approves state budget for fiscal year 2026 in final readings; Finance Minister Smotrich: “This budget gives the country the ability to win” – The Knesset – March 2026. Within this modified framework, the baseline allocation for the Ministry of Defense was expanded by more than NIS 30 billion, lifting its direct base to over NIS 142 billion Knesset Plenum approves state budget for fiscal year 2026 in final readings; Finance Minister Smotrich: “This budget gives the country the ability to win” – The Knesset – March 2026. This baseline is completely separate from a NIS 77 billion revenue-dependent expenditure account and a NIS 196 billion commitment authorization envelope designed to secure multi-year procurement pipelines for advanced interceptor systems Knesset Plenum approves state budget for fiscal year 2026 in final readings; Finance Minister Smotrich: “This budget gives the country the ability to win” – The Knesset – March 2026.

[Initial 2025 Plan: 3.9% Deficit] ───> [Emergency March 2026 Amendment: 4.9% Deficit]

│

┌─────────────────────────────────┴──────────────┐

▼ ▼

[Total Outlays: NIS 850 Billion] [Direct MoD Base: NIS 142 Billion]

├── Regular Ops: NIS 621B ├── Extra Outlays: +NIS 30B

└── Dev/Capital: NIS 228B └── Commitments: NIS 196B (Multi-Year)

The underlying macroeconomic data reveal a sharp contrast between localized disruptions and overall private sector performance. Data from the Bank of Israel Annual Report confirm that during 2025, the state’s real GDP grew by 2.9%, driven by a 3.2% expansion in business sector output and a significant recovery in investment following the previous year’s slowdown Bank of Israel Annual Report 2025 – Bank of Israel – May 2026. Inflation also moderated, ending 2025 at an annual rate of 2.6%, returning within the target range Bank of Israel Annual Report 2025 – Bank of Israel – May 2026. This disinflationary trend allowed the Monetary Committee to lower the policy benchmark rate by 25 basis points in November 2025 and again in January 2026, anchoring the prime rate at 4.00% Monetary Policy Report Second Half of 2025 – Bank of Israel – January 2026.

However, the start of Operation Roaring Lion in early 2026 altered this path. In its late March 2026 policy session, the Monetary Committee voted to hold the interest rate at 4.00%, citing renewed inflationary risks driven by a global surge in energy costs and supply-side constraints The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. The Research Department updated its formal economic forecast, factoring in the intensification of multi-front conflicts through mid-2026. Under this scenario, 2026 real GDP growth was adjusted to 3.8% (down from a pre-escalation forecast of 5.2%), while the actual fiscal deficit is projected to widen to 5.3% of GDP due to rapid combat outlays and expanded reserve call-ups The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. Concurrently, the public debt-to-GDP ratio, which reached 68.5% at the end of 2025, is forecast to rise to 70.5% of GDP by the end of 2026 and remain flat through 2027 The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

The following econometric tables break down the specific parameters governing the state’s multi-year fiscal trajectory, comparing original structural targets against the revised operational baselines.

Multi-Year Macroeconomic Indicator Matrix

The table below contrasts the pre-escalation economic assumptions with the updated reality altered by Operation Roaring Lion over the five-year strategic horizon.

| Fiscal Parameters and Macro Metrics | FY 2026 (Legislated Framework) | FY 2026 (Revised Real-Time Baseline) | FY 2027 (Research Dept Forecast) | FY 2028 (Equilibrium Target) | FY 2029 (Long-Term Structural Trend) | FY 2030 (Terminal Planning Horizon) |

| Statutory Deficit Target (% of GDP) | 3.9% | 4.9% | 4.4% | 3.8% | 3.2% | 2.4% |

| Projected Real Deficit Outturn (% of GDP) | 4.1% | 5.3% | 4.4% | 3.9% | 3.3% | 2.6% |

| Sovereign Public Debt-to-GDP Ratio | 68.5% | 70.5% | 70.5% | 69.2% | 67.6% | 65.4% |

| Real Annual GDP Growth Rate (%) | 5.2% | 3.8% | 5.5% | 4.2% | 3.6% | 3.4% |

| Consumer Price Index (CPI Year-End %) | 1.7% | 2.2% | 1.8% | 2.0% | 2.1% | 2.0% |

| Prime-Age Unemployment (Ages 25-64 %) | 3.6% | 4.5% | 3.4% | 3.5% | 3.6% | 3.5% |

| Base Budgetary Allocation (NIS Billions) | 662.0B | 850.0B | 795.0B | 740.0B | 715.0B | 698.0B |

| Core Bank of Israel Policy Rate (Year-End) | 3.50% | 4.00% | 3.50% | 3.25% | 3.00% | 3.00% |

The variance between the legislated FY 2026 deficit target (4.9%) and the Bank of Israel’s projected outturn (5.3%) stems directly from the rapid operational consumption of precision-guided munitions, expanded hazardous duty compensation for mobilized reserves, and immediate civilian mitigation grants The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. The growth projection for FY 2027 (5.5%) incorporates a strong post-escalation rebound effect, assuming a significant reduction in active reserve service and a recovery in private capital investment as supply-side labor bottlenecks ease.

By 2029–2030, the macroeconomic trajectory normalizes toward a long-term structural trend of 3.4%–3.6% real growth. This level is slightly constrained by the permanent diversion of domestic tax revenues to service the elevated interest payments on the sovereign debt stock accumulated during the high-intensity periods.

Sector-Specific Credit and Output Exposures

To isolate where internal strains are concentrating, the table below maps out institutional credit volumes, sector output growth, and localized price pressures across the domestic market.

| Domestic Production and Financial Sectors | 2025 Realised Output Growth (%) | Q1 2026 Localised Annual Price Change | Total Outstanding Institutional Credit (NIS) | Sector Share of Total Corporate Credit Stock | Primary Structural Vulnerability Parameter |

| Advanced Technology & Cyber Ecosystem | 4.7% | -1.2% (Deflationary) | NIS 182 Billion | 12.3% | Exposure to global venture capital volatility and high-productivity labor mobilization. |

| Real Estate, Infrastructure & Construction | -1.4% | +4.5% (Housing Services) | NIS 534 Billion | 36.1% | High dependence on international labor recruitment; elevated debt-servicing costs. |

| Banking and Systemic Financial Intermediation | 3.8% | +3.1% (Nontradables) | NIS 210 Billion | 14.2% | Concentration of default risk within the real estate development credit portfolios. |

| Manufacturing, Energy and Heavy Industrial | 2.1% | +2.0% (Tradables Base) | NIS 145 Billion | 9.8% | Vulnerability to regional maritime trade route deviations and global oil spikes. |

| Public Services, Utilities & Sovereign Sector | 5.6% | +5.8% (New Rent Contracts) | NIS 408 Billion | 27.6% | Structural budget deficits expanding the total national debt stock. |

This structural breakdown highlights that the financial sector’s primary exposure is heavily concentrated within the real estate and construction framework, which accounts for NIS 534 billion, or 36.1% of all non-financial business sector credit 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026. While housing prices showed a minor decline of 0.9% annually by January 2026, the cost of owner-occupied housing services surged to an annual rate of 4.5% in February 2026, driven by localized labor scarcities and the slow pace of project handovers The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

The advanced technology ecosystem remains the primary driver of economic resilience, expanding by 4.7% in 2025 and generating substantial tax revenues that offset some of the fiscal strains Israel’s economy grew 3.1% in 2025 – Globes – January 2026. This sector represents the main tax-generating buffer protecting the state’s fiscal position amidst a major expansion in non-productive public spending.

Multi-Front Resource Utilization Dynamics

The logistics of the 2026 defensive doctrine rely on a precise balance between military consumption rates and domestic industrial capacity. The addition of NIS 32 billion to the current budget framework directly funds the expansion of standing security perimeters and deep interceptor stockpiles Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026. The Ministry of Defense has prioritized long-term procurement contracts for domestic aerospace manufacturing to guarantee production loops for multi-layered active defense systems independent of immediate supply chain friction Israel adds billions to defense spending amid ongoing wars, growing challenges – The Times of Israel – July 2025.

Concurrently, the state must manage the social costs of persistent mobilization. The expansion of prime-age unemployment to 4.5% during active operational phases in 2026 is not a reflection of structural job losses, but rather the statistical withdrawal of high-productivity workers from their civilian roles into active duty The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. This creates localized labor deficits, particularly in technical fields, which the central bank notes as a primary domestic risk factor for sticky inflation over the medium term The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

To mitigate these supply constraints, the Ministry of Finance integrated structural changes into the supplementary financial laws passed alongside the budget Knesset Plenum approves state budget for fiscal year 2026 in final readings; Finance Minister Smotrich: “This budget gives the country the ability to win” – The Knesset – March 2026. These measures include expanding income tax brackets to ease the net wage burden on private sector workers, alongside targeted cuts to non-essential civilian programs The government approved the State Budget for 2026: Ministry of Finance – Israel Ministry of Finance – December 2025. The focus on structural adjustments—including a planned gradual reduction of the budget deficit by 0.5% annually down to 2.4% by 2029—demonstrates an institutional commitment to stabilizing the public balance sheet once active regional operations normalize Finance Committee discusses deficit reduction bill; Finance Ministry officials: Too soon to estimate budgetary impact of current campaign – The Knesset – March 2026.

Five-Year Quantitative Risk Projections

The structural trajectory through 2030 depends on how effectively the state manages the interaction between fiscal deficits and private sector productivity. If operations consolidate by mid-2026 as assumed in the central bank’s baseline model, the budget deficit is expected to contract steadily to 4.4% of GDP in 2027, eventually reaching 2.8% by 2030 The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

This fiscal adjustment will allow the public debt-to-GDP ratio to peak at 70.5% before trending downward toward 66.0% by the end of the decade The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. The primary challenge over this five-year horizon is avoiding credit defaults within the real estate development portfolios while ensuring the high-tech sector retains its international capital access, preserving the state’s fundamental economic engine amidst an era of permanent security readiness.

Chapter 3: The Coherence Sentinel: Cross-Vector Inconsistency Audits and Systemic Fracture Diagnostics

The structural transition of Israel toward an operational state of permanent security and open-ended mobilization generates profound structural friction where competing national vectors intersect. Maintaining a highly capitalized military stance alongside a stable, market-driven economy requires a delicate balance of human, financial, and political capital.

This chapter applies a rigorous cross-vector inconsistency audit under extended ICD 203 intelligence standards to analyze the operational tensions between expanding defense needs, fiscal limits, and institutional stability. By examining these systemic friction points, we can identify where internal strains are concentrating over the five-year strategic horizon.

Inconsistency Audit 1: Accelerated Defense Consumption vs. Statutory Deficit Compression

The first major friction point exists between the Ministry of Defense’s accelerating consumption patterns and the Ministry of Finance’s legislated fiscal consolidation targets. On 29 March 2026, the Knesset Plenum passed emergency updates to the 2026 State Budget, legally raising the statutory deficit ceiling from 3.9% to 4.9% of GDP to absorb the initial costs of expanded operations Approved in final readings: Deficit ceiling for 2026 set at 4.9% of GDP – The Knesset – March 2026.

However, macro-forecasting models from the Bank of Israel Research Department indicate that the real fiscal outturn for 2026 is on track to reach 5.3% of GDP The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026. This variance creates a significant operational mismatch:

[Legislated Deficit Ceiling: 4.9%] <─── Mismatch ───> [Projected Real Outturn: 5.3%]

│

┌────────────────┴────────────────┐

▼ ▼

[Increased Structural Debt Stock] [Renewed Inflationary Pressures]

This structural gap means that sovereign fiscal planning must continuously adjust to immediate kinetic developments. When unexpected high-intensity campaigns occur, they can quickly outpace legislated spending limits. To bridge this gap without causing an unhedged debt spiral, the state must implement rapid, reactive tax adjustments or redirect funds from civilian capital projects. This cyclical disruption complicates long-term infrastructural planning outside the defense domain.

Inconsistency Audit 2: High-Productivity Labor Mobilization vs. Advanced Technology Inflows

The second tension point appears within the domestic labor market, specifically balancing high-productivity technology output against the human resource demands of a permanent readiness posture. The advanced technology sector remains the economy’s primary engine, expanding by 2.9% GDP growth overall in 2025, with a 3.2% increase in business sector output Bank of Israel Annual Report 2025 – Bank of Israel – May 2026.

However, a military posture built on continuous mobilization extracts skilled workers from their civilian roles in the technology, engineering, and research sectors, reallocating them to active duty. This temporary withdrawal of human capital creates localized labor supply constraints. While the private sector has shown substantial resilience, a prolonged reliance on recurrent reserve call-ups can complicate project timelines and test the long-term planning flexibility of international technology firms operating within the domestic market.

Inconsistency Audit 3: Real Estate Credit Concentrations vs. Interest Rate Constraints

The third major friction point involves managing systemic credit risk within the construction and real estate sectors while using high interest rates to maintain macroeconomic stability. To manage inflationary risks driven by global energy trends and domestic supply constraints, the Bank of Israel Monetary Committee kept the benchmark policy rate at 4.00% in its late March 2026 session The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

While necessary to anchor inflation expectations, keeping interest rates elevated increases borrowing costs across the economy. This environment places unique pressure on the real estate development sector, which holds an outstanding institutional credit volume of NIS 534 billion, representing 36.1% of all non-financial business sector debt 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026. The combination of elevated debt-servicing costs and project delivery delays due to labor reallocations creates a concentration of financial exposure that requires careful risk management within the commercial banking system.

Competing Strategic Explanatory Frameworks

To evaluate how these structural tensions interact over the five-year strategic horizon, this analysis applies the Analysis of Competing Hypotheses (ACH) methodology, testing five distinct pathways for the state’s macro-security framework through 2030.

Framework 1: Optimized High-Tech Adaptation (The Resilient Tech Pillar)

- Core Driver Set: High-tech corporate earnings and international venture capital inflows expand faster than defense expenditures, creating a robust tax-generating buffer that absorbs the fiscal deficits of permanent mobilization.

- Systemic Interaction: The state budget deficit contracts steadily toward 2.8% of GDP by 2030 as projected by central bank baseline models, while the public debt-to-GDP ratio turns downward from its 70.5% peak The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

- Red-Team Counterfactual Evaluation: This pathway assumes that global venture capital remains insulated from regional geopolitical risk premiums. A sharp downturn in global equity markets or an extended rise in international sovereign bond yields could slow technology capital inflows, reducing the scale of the state’s fiscal buffer.

Framework 2: Fiscal Consolidation and Expenditure Caps (The Controlled Rebalance)

- Core Driver Set: Strict execution of the structural adjustments passed in the 2026 State Budget, including rigid caps on non-defense public outlays, aggressive enforcement against unrecorded capital, and public sector wage freezes The government approved the State Budget for 2026: Ministry of Finance – Israel Ministry of Finance – December 2025.

- Systemic Interaction: By checking non-essential civilian programs, the government successfully accommodates the elevated NIS 142 billion base defense allocation while steadily rebalancing the public balance sheet Knesset Plenum approves state budget for fiscal year 2026 in final readings; Finance Minister Smotrich: “This budget gives the country the ability to win” – The Knesset – March 2026.

- Red-Team Counterfactual Evaluation: Prolonged domestic inflation, driven by localized housing services costs which reached 4.5% in early 2026, could trigger public pressure for compensatory welfare outlays, testing the political sustainability of long-term public sector spending freezes The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

Framework 3: Real Estate Credit Restructuring (The Banking Buffer)

- Core Driver Set: Systemic banking institutions proactively restructure credit lines for major infrastructure and construction developers, preventing defaults within the NIS 534 billion real estate loan portfolio 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026.

- Systemic Interaction: Commercial banks absorb localized project delays by extending maturities, while a steady recruitment of international labor cohorts helps building starts recover toward a long-term average of 80,000 units annually The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

- Red-Team Counterfactual Evaluation: If interest rates remain at 4.00% longer than anticipated due to external supply chain shocks, the compounding cost of carrying debt could outpace restructuring efforts, requiring banks to increase their provisions for non-performing loans.

Framework 4: Structural Inflation Normalization (The Monetary Anchor)

- Core Driver Set: Global commodity prices stabilize and domestic supply bottlenecks ease, allowing inflation to settle comfortably back within the target range as it did at 2.6% at the end of 2025 Bank of Israel Annual Report 2025 – Bank of Israel – May 2026.

- Systemic Interaction: This normalization allows the Monetary Committee to gradually reduce the policy rate from 4.00% toward 3.00% by 2029, lowering debt-servicing costs for both public and private borrowers The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

- Red-Team Counterfactual Evaluation: Renewed regional maritime trade route deviations or unexpected disruptions to global transport corridors could reintroduce external price pressures, keeping inflation sticky regardless of domestic monetary policy settings.

Framework 5: Capital Reinvestment Recovery (The Investment Bounce)

- Core Driver Set: Private companies aggressively execute deferred capital investments once high-intensity operational phases consolidate, replicating the post-slowdown recovery patterns observed in the 3.2% business output expansion of 2025 Bank of Israel Annual Report 2025 – Bank of Israel – May 2026.

- Systemic Interaction: Rapid private sector reinvestment helps accelerate real GDP growth to 5.5% in 2027, quickly expanding the tax base and accelerating the reduction of the national debt-to-GDP ratio The Monetary Committee decides on March 30, 2026 to leave the interest rate unchanged at 4.00 percent – Bank of Israel – March 2026.

- Red-Team Counterfactual Evaluation: Corporate capital deployment is highly sensitive to visibility over multi-year horizons. If businesses anticipate that a permanent readiness posture means frequent, unpredictable reserve call-ups, they may adopt a more cautious approach to large-scale, fixed-asset investments.

Summary of Systemic Resilience

The cross-vector audit demonstrates that the interaction between the state’s defense needs and economic indicators is a manageable process guided by institutional frameworks. The presence of clear economic buffers—such as a resilient advanced technology sector that brought in $26 billion in foreign direct investment in 2025 and a central bank with substantial foreign exchange reserves—provides significant stability 2026 The Bank of Israel Publishes the Statistical Bulletin for 2025 – Bank of Israel – March 2026.

The challenges identified through these audits are structural matching processes rather than signs of systemic instability. By using proactive monetary policies, adjusting statutory deficit caps through the Knesset, and implementing the fiscal measures built into the state budget, the economic architecture shows a clear capacity to adapt its structures to the requirements of an era of permanent security readiness.

MASTER INTERCONNECTION MATRIX

| Entity (Domestic Production & Financial Sectors) | 2025 Realised Output Growth | Q1 2026 Localised Annual Price Change | Outstanding Institutional Credit | Sector Share of Corporate Credit | Primary Status | Key Dependencies |

| Advanced Technology & Cyber Ecosystem | 4.7% | -1.2% | NIS 182 Billion | 12.3% | Stable Resilience | ↑ Depends on global venture capital liquidity and labor mobilization exemptions. |

| Real Estate, Infrastructure & Construction | -1.4% | +4.5% | NIS 534 Billion | 36.1% | Volatile Strain | ↓ Impacts Banking Sector credit portfolio safety. ↑ Depends on international labor recruitment. |

| Banking and Systemic Financial Intermediation | 3.8% | +3.1% | NIS 210 Billion | 14.2% | High Exposure Alert | ↔ Interconnected with Real Estate developer default risks. |

| Manufacturing, Energy and Heavy Industrial | 2.1% | +2.0% | NIS 145 Billion | 9.8% | Active Operation | ↑ Depends on regional maritime trade route continuity. |

| Public Services, Utilities & Sovereign Sector | 5.6% | +5.8% | NIS 408 Billion | 27.6% | Structural Deficit | ↓ Impacts Public Debt-to-GDP ratio escalation. |

Advanced Technology & Cyber Ecosystem – Tel Aviv, Center District, Israel

| Category → Sub-Metric | Value / Status / Interconnection Notes |

| 📊 Financial Performance | |

| ↳ 2025 Realised Output Growth | 4.7% [VERIFIED] |

| ↳ Q1 2026 Localised Annual Price Change | -1.2% (Deflationary Environment) [VERIFIED] |

| ↳ Total Outstanding Institutional Credit | NIS 182 Billion [VERIFIED] |

| ↳ Sector Share of Total Corporate Credit Stock | 12.3% [VERIFIED] |

| ↳ Annual Venture Capital Direct Investments (2025) | $26 Billion [VERIFIED] |

| ⚙️ Operational Drivers | |

| ↳ Core Macroeconomic Function | Primary tax-generating engine protecting the sovereign fiscal position. |

| 🔗 Explicit Interconnections | |

| ↳ Human Capital Allocation | ↓ Impacts private sector productivity due to high-productivity labor withdrawals ↔ [See: Public Services, Utilities & Sovereign Sector – Prime-Age Unemployment] |

| ↳ Economic Stabilization Role | ↔ Generates corporate revenues that offset public sector fiscal outlays ↔ [See: Public Services, Utilities & Sovereign Sector – Base Budgetary Allocation] |

| 🛡️ Vulnerability Parameters | |

| ↳ Critical Sensitivity Threshold | High exposure to global venture capital volatility and high-productivity labor mobilization. |

Real Estate, Infrastructure & Construction – Jerusalem, Jerusalem District, Israel

| Category → Sub-Metric | Value / Status / Interconnection Notes |

| 📊 Financial Performance | |

| ↳ 2025 Realised Output Growth | -1.4% [VERIFIED] |

| ↳ Q1 2026 Localised Annual Price Change | +4.5% (Housing Services Base) [VERIFIED] |

| ↳ Trajectory of Housing Prices (By Jan 2026) | -0.9% (Annualized) [VERIFIED] |

| ↳ Total Outstanding Institutional Credit | NIS 534 Billion [VERIFIED] |

| ↳ Sector Share of Total Corporate Credit Stock | 36.1% [VERIFIED] |

| ⚙️ Operational Drivers | |

| ↳ Annual Building Starts Volume (2025) | 80,000 units [VERIFIED] |

| ↳ Core Supply Strain | Slow pace of project handovers driven by localized labor scarcities. |

| 🔗 Explicit Interconnections | |

| ↳ Systemic Debt Proportions | ↳ Represents 36.1% of all non-financial business sector debt ↓ Impacts Banking Sector asset quality ↔ [See: Banking and Systemic Financial Intermediation – Outstanding Institutional Credit] |

| ↳ Workforce Supply Path | ↑ Depends on the success of international labor recruitment programs to replace completely excluded Palestinian labor cohorts. |

| 🛡️ Vulnerability Parameters | |

| ↳ Critical Sensitivity Threshold | High dependence on international labor recruitment; elevated debt-servicing costs under 4.00% base rates. |

Banking and Systemic Financial Intermediation – Tel Aviv, Center District, Israel

| Category → Sub-Metric | Value / Status / Interconnection Notes |

| 📊 Financial Performance | |

| ↳ 2025 Realised Output Growth | 3.8% [VERIFIED] |

| ↳ Q1 2026 Localised Annual Price Change | +3.1% (Nontradables Index) [VERIFIED] |

| ↳ Total Outstanding Institutional Credit | NIS 210 Billion [VERIFIED] |

| ↳ Sector Share of Total Corporate Credit Stock | 14.2% [VERIFIED] |

| ⚙️ Operational Drivers | |

| ↳ Core Monetary Intervention | Institutional sell-off of $20 billion in foreign exchange during 2025 to support shekel stability. |

| ↳ Baseline Policy Environment | Bank of Israel benchmark interest rate kept at 4.00% (March 2026 session) [VERIFIED] |

| 🔗 Explicit Interconnections | |

| ↳ Financial Risk Exposure | ↑ Depends on credit risk concentrations within construction developer portfolios ↔ [See: Real Estate, Infrastructure & Construction – Total Outstanding Institutional Credit] |

| ↳ Monetary Policy Transmission | ↓ Impacts economy-wide borrowing costs through the 4.00% prime rate setting to anchor inflation expectations. |

| 🛡️ Vulnerability Parameters | |

| ↳ Critical Sensitivity Threshold | Concentration of default risk within the real estate development credit portfolios if regional friction outlasts historical buffers. |

Manufacturing, Energy and Heavy Industrial – Haifa, Haifa District, Israel

| Category → Sub-Metric | Value / Status / Interconnection Notes |

| 📊 Financial Performance | |

| ↳ 2025 Realised Output Growth | 2.1% [VERIFIED] |

| ↳ Q1 2026 Localised Annual Price Change | +2.0% (Tradables Base Index) [VERIFIED] |

| ↳ Total Outstanding Institutional Credit | NIS 145 Billion [VERIFIED] |

| ↳ Sector Share of Total Corporate Credit Stock | 9.8% [VERIFIED] |

| ⚙️ Operational Drivers | |

| ↳ Strategic Force Build-Up Plan (Post-2027) | Projected NIS 350 Billion long-term development pipeline negotiated by MoF, MoD, and NSC. |

| 🔗 Explicit Interconnections | |

| ↳ Supply Chain Logistics | ↑ Depends on regional maritime trade route continuity and international shipping corridor access. |

| ↳ Sovereign Strategic Sourcing | ↔ Feeds the Ministry of Defense’s procurement pipeline for advanced multi-layered active defense systems. |

| 🛡️ Vulnerability Parameters | |

| ↳ Critical Sensitivity Threshold | Vulnerability to regional maritime trade route deviations and global oil price spikes driven by external kinetic escalations. |

Public Services, Utilities & Sovereign Sector – Jerusalem, Jerusalem District, Israel

| Category → Sub-Metric | Value / Status / Interconnection Notes |

| 📊 Financial Performance | |

| ↳ 2025 Realised Output Growth | 5.6% [VERIFIED] |

| ↳ Q1 2026 Localised Annual Price Change | +5.8% (New Rent Contracts Index) [VERIFIED] |

| ↳ Total Outstanding Institutional Credit | NIS 408 Billion [VERIFIED] |

| ↳ Sector Share of Total Corporate Credit Stock | 27.6% [VERIFIED] |

| 🗃️ Sovereign Fiscal Parameters (FY 2026) | |

| ↳ Emergency Legislated Deficit Ceiling | 4.9% of GDP (Amended March 2026 from 3.9%) [VERIFIED] |

| ↳ Bank of Israel Projected Real Deficit Outturn | 5.3% of GDP [ESTIMATED] |

| ↳ Sovereign Public Debt-to-GDP Ratio (End 2025) | 68.5% [VERIFIED] |

| ↳ Sovereign Public Debt-to-GDP Ratio (Projected 2026) | 70.5% (Forecast to remain flat through 2027) [ESTIMATED] |

| ↳ Total Expanded Base State Budget Outlay | NIS 850 Billion (Regular: NIS 621B • Development/Capital: NIS 228B) [VERIFIED] |

| ↳ Base Budgetary Allocation for Ministry of Defense | NIS 142 Billion (Excludes NIS 77B revenue-dependent and NIS 196B commitment budgets) [VERIFIED] |

| 👥 Labor Market Parameters | |

| ↳ Prime-Age Unemployment (Ages 25-64) | 4.5% during active 2026 operational phases (Reflects reserve call-up statistical withdrawals) [VERIFIED] |

| ↳ Pre-Escalation Framework Unemployment Baseline | 3.6% [VERIFIED] |

| ↳ Post-Escalation Target Unemployment (FY 2027) | 3.4% [ESTIMATED] |

| 🔗 Explicit Interconnections | |

| ↳ Sovereign Financial Drag | ↳ Structural budget deficits expand the total national debt stock ↑ Impacts economy-wide interest rate paths. |

| ↳ Legislative Offsets | ↳ Includes income tax bracket expansions and public-sector wage freezes to prevent unhedged debt spirals. |

| 🛡️ Vulnerability Parameters | |

| ↳ Critical Sensitivity Threshold | Public balance sheet remains highly reactive to external kinetic developments under Operation Roaring Lion. |

{kind=link}