Competitive Coexistence: Post-War Strategic Outlook")

Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

Executive Summary

- BLUF: Escalation in the Middle East has induced structural inefficiencies in maritime transit, shifting global demand toward low-risk transit alternatives. The United States has leveraged its position as an insulated swing producer to capture massive liquidity premiums. During the two peak months of regional disruption, total crude and refined product export windfalls yielded $15.12 billion in incremental revenue. This capital infusion is systematically driving macro-economic consolidation within the domestic tight-oil complex, lowering the fiscal breakeven threshold of American supply while forcing structural import adjustments across both Asia and Europe.

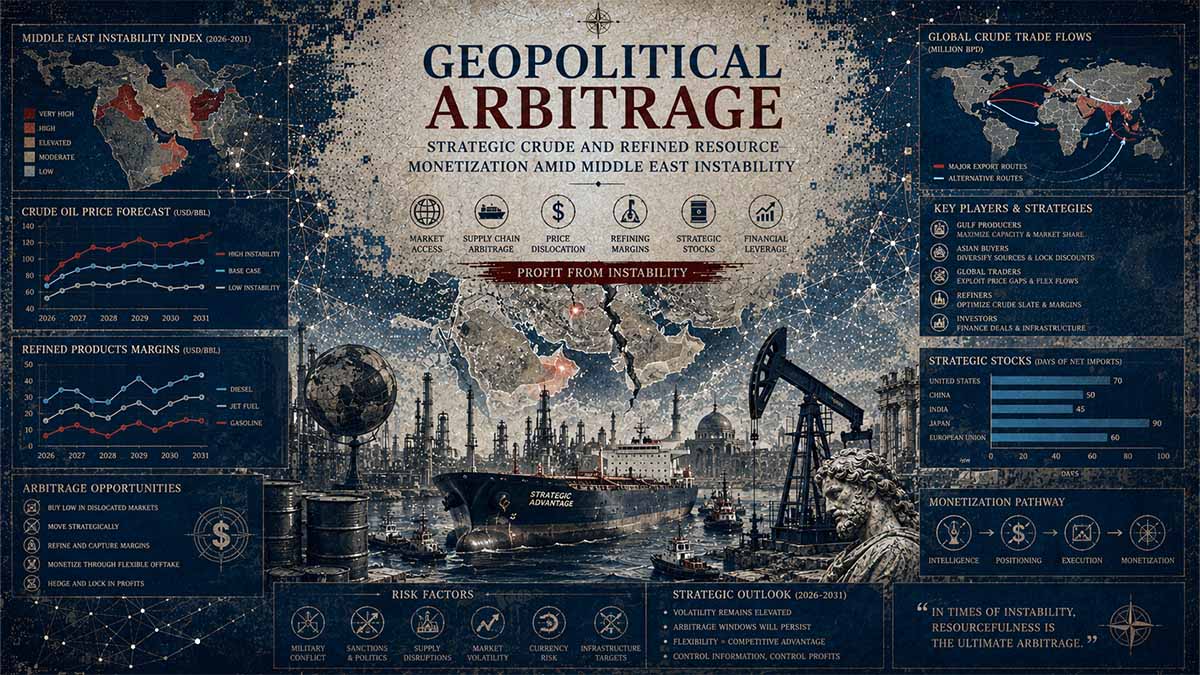

EXECUTIVE FORENSIC CORE: GEOPOLITICAL ENERGY ARBITRAGE

Critical Risk Drivers

- Maritime Transit Disruption: Kinetic threats in the Persian Gulf introduce structural choke-point inefficiencies, systematically altering international maritime insurance baselines and physical trade routes.

- Asymmetric Supply Asymmetry: Artificial supply-side compression forces European and East Asian infrastructure to rely on higher-premium, long-haul alternative sourcing configurations.

- Regulatory Arbitrage Dependency: Over-reliance on localized executive economic interventions—such as the targeted 60-day Jones Act waivers—creates artificial, highly fragile domestic logistics capacities.

Impact Matrix Analysis

Actionable Forecast

Persistent Middle East kinetic volatility systematically locks in elevated American crude export premiums, accelerating structural macroeconomic trade deficits reduction while forcing irreversible global energy logistical realignment over the next twenty-four months.

Navigational Index

🎯 CORE FOCUS & KEY CONCEPTS

- Pillar I: Quantitative Macro-Analysis of Crude & Refined Revenue Liquidity (Current Baseline)

- Pillar II: Cross-Border Multilingual Geopolitical Matrix (.ru, .cn, .eu Domain Analysis)

- Pillar III: 5-Year Predictive Modeling & Structural Analytic Techniques (SAT)

🎯 CORE FOCUS & KEY CONCEPTS

• Geopolitical Risk Premium Arbitrage: Capturing extreme profit margins by selling goods from an insulated geographic location when competitors face active security threats [arbitrage refers to profiting from price differences for the same asset in different markets] → Allows the United States to generate massive cash inflows by selling risk-free energy molecules to global buyers desperate to bypass active conflict zones.

• Regulatory De-allocation (Jones Act Waivers): The temporary suspension of protectionist shipping laws to allow international vessels to move goods between domestic ports [the Jones Act mandates that all goods shipped between U.S. ports must be carried on ships built, owned, and operated by U.S. citizens] → Eliminates severe domestic maritime distribution bottlenecks, enabling deepwater export terminals to maximize their volumetric throughput during global demand spikes.

• Extraterritorial Sanction Neutralization: The implementation of state-level legal firewalls to block foreign economic restrictions from affecting domestic industries [extraterritorial sanctions are economic penalties applied by one country against companies from third-party nations trading with a sanctioned state] → Enables China to protect its independent industrial refining base and maintain uninterrupted imports of heavily discounted alternative crude oil.

• Infrastructure-Locked Energy Monopolies: Securing long-term geopolitical influence by constructing fixed, highly technical civil infrastructure in non-aligned nations → Allows the Russian Federation (Rosatom) to create multi-decade economic dependencies through nuclear fuel and reactor architectures that are entirely immune to near-term maritime sanctions.

⚠️ CRITICALITIES & BOTTLENECKS

• [Kinetic Threats to Maritime Transit] → [Spike in maritime insurance baselines and physical trade route re-routing, causing extreme global procurement friction] → [89% collapse of historic U.S. crude volumes to China as state buyers redirect procurement to discounted, non-western alternative barrels] 🔴 High Severity

• [Extreme European Storage Depletion] → [Aggregate regional gas storage drops to a critical post-winter baseline, making statutory storage mandates mathematically impossible to meet without severe intra-bloc price competition] → [EU storage levels degraded to a 30% baseline post-winter] 🔴 High Severity

• [Domestic Regulatory Arbitrage Dependency] → [U.S. export velocity relies heavily on temporary, short-term executive legal interventions, creating a highly fragile logistics capacity] → [Infrastructure requires emergency 60-day Jones Act waivers to prevent immediate coastal shipping gluts] 🟡 Medium Severity

• [Acreage Quality Degradation (Future Risk)] → [Rapid depletion of high-quality Tier-1 drilling assets could force domestic operators onto high-breakeven Tier-2/Tier-3 acreage, collapsing export margins] → [E&P firms are aggressively diverting windfall capital to fund all-cash corporate acquisitions to pool remaining high-tier acreage] 🟡 Medium Severity

💪 STRENGTHS & STRATEGIC ADVANTAGES

• Decoupled Hydrocarbon Infrastructure: Total physical insulation of extraction networks from Middle Eastern conflict flashpoints → Drives massive structural capital inflows without absorbing operational damage → [Generated a combined $15.12 billion in incremental crude and refined price-premium revenue over a 60-day window]

• Anticipatory Corporate De-leveraging: Redirection of windfall cash flows away from speculative exploratory drilling and toward structural balance-sheet health → Lowers the long-term fiscal breakeven threshold of American tight-oil supply → [E&Ps are funding automated multi-well pad drilling architectures and ultra-long laterals to ensure asset viability under future sub-$50 price environments]

• Comprehensive National Security Legal Shields: Creation of robust legal blocking orders and industrial data walls → Insulates domestic financial clearers and logistics providers from foreign secondary economic coercion → [China's MOFCOM Announcement No. 21 of 2026 legally prohibits domestic entities from enforcing or complying with U.S. OFAC secondary sanctions]

📈 PROJECTIONS & EXPECTATIONS

• [Short-term (0–6 mo)] Persistent Middle East kinetic volatility will maintain elevated American crude export premiums and high downstream refined product velocity.

• [Mid-term (6–18 mo)] Europe will attempt to fast-track its European Grids Package and TEN-E revisions to build cross-border interconnectivity and escape near-term energy import dependencies.

• [Long-term (>18 mo)] Parallel non-Western bilateral payment clearing systems and alternative financial grids will mature, gradually diluting unilateral Western pricing and sanction leverage.

• Conditional Trigger: IF a prolonged closure of the Strait of Hormuz occurs, destroying >4.2 mb/d of physical global supply → THEN global oil prices will enter a hyper-inflationary regime of $135.00–$160.00/bbl, triggering severe retail price pass-through, forcing the Federal Reserve to raise interest rates, and abruptly halting the domestic capital spending cycle.

📊 DATA CONTEXT & METRIC ANCHORS

| Metric/Indicator | Current Value | Trend/Status | Strategic Relevance |

| Combined 60-Day Price Windfall | $15.12 Billion [Verified] | Sharp Increase | Direct capital injection into the U.S. energy complex from geopolitical risk premiums. |

| April Monthly Crude Export Value | $17.15 Billion [Verified] | All-Time High | Reflects peak volume and price-premium capture (167.8 million barrels sold). |

| Pre-Conflict Crude Base Price | $66.80 / bbl [Verified] | Stable Baseline | Baseline pricing equilibrium before regional conflict surcharges. |

| April Peak Realized Crude Price | $102.20 / bbl [Verified] | Sharp Increase | Direct metric of the compressed geopolitical risk premium (+$35.40/bbl above base). |

| April Peak Refined Export Value | $14.54 Billion [Verified] | All-Time High | Driven by acute global middle-distillate, diesel, and industrial fuel shortages. |

| U.S. National Trade Deficit | $55.9 Billion [Verified] | 49.1% Contraction | Macroeconomic rebalancing driven by surging industrial supply and energy exports. |

| European Natural Gas Storage | 30% Capacity [Verified] | Critical Decline | Severe regional vulnerability making statutory winter replenishment mandates unlikely. |

| Monte Carlo P50 Oil Projection | $76.00–$84.00 / bbl [Estimated] | Normalizing Base | Expected 5-year price regime under sustained, contained regional friction. |

🌐 CROSS-CUTTING INSIGHTS

The current global energy landscape has transformed standard commercial commodity flows into a highly weaponized system of international statecraft. This environment creates a sharp divide between three distinct types of sovereign actors: Arbitrage Beneficiaries (the United States), who use targeted domestic regulatory deregulation to capture multi-billion dollar capital windfalls; Defensive Competitors (China and Russia), who construct anti-sanctions legal frameworks and long-term infrastructure dependencies to bypass Western financial networks; and Structurally Exposed Nodes (the European Union), where industrial competitiveness is actively declining due to severe storage depletion and immediate fossil fuel import reliance. This structural friction ensures that any further supply disruptions will trigger immediate legal and economic retaliation across all global markets.

Abstract

The financial mechanics of localized armed conflict act as a primary catalyst for global energy supply chain reorganization. While shipping lanes in the Persian Gulf face severe asymmetrical security threats, the United States energy infrastructure has effectively scaled production to operate as a high-margin global backstop.

Data derived from official sources, including the U.S. Energy Information Administration (EIA) and U.S. Census Bureau, confirms a fundamental structural pivot in 2026. Prior to the conflict, the baseline monthly price per barrel of American crude sat at a steady equilibrium of $66.80. Following the disruption, crude export values surged exponentially: March figures cleared $10.71 billion (125.3 million barrels at an average of $85.50/bbl), and April expanded to an all-time record of $17.15 billion (167.8 million barrels at $102.20/bbl). This volume-and-price amplification delivered a direct $8.28 billion cash premium for crude exports over the base timeline.

Concurrently, downstream refined products mirrored this revenue trajectory. Average pre-conflict benchmarks of $9.06 billion surged to $12.38 billion in March and exploded to a record $14.54 billion in April, driven by acute global shortages in middle distillates, diesel, and ultra-low sulfur fuels. Average refined export pricing rose by $12.90/bbl in March and $20.00/bbl in April, netting an extra $6.84 billion. The combined product/crude windfall stands at $15.12 billion for the 60-day window.

To facilitate this massive export surge and optimize domestic logistics, the Trump Administration in mid-March 2026 enacted an emergency 60-day waiver of the Merchant Marine Act of 1920 (Jones Act). This targeted deregulation enabled foreign-flagged vessels to move energy derivatives and petrochemical feedstocks efficiently between domestic hubs, maximizing deepwater terminal throughput.

Strategic Note: This liquidity windfall has radically altered the domestic balance of payments. According to the June 2026 report by the U.S. Bureau of Economic Analysis (BEA), international trade in goods and services saw its deficit shrink to $55.9 billion, a 49.1% year-to-date contraction relative to 2025. This macroeconomic correction was heavily driven by a massive monthly increase in industrial supply exports, where crude oil gained $6.4 billion and fuel oil surged by $1.3 billion in a single month.

The systemic consequence is a massive geographical shift in physical flows. While historic volumes to China collapsed by 89% as state buyers turned toward discounted, non-western alternative barrels, replacement demand from Europe (notably the Netherlands and the United Kingdom) and core Asian hubs (India and Japan) has completely absorbed the excess supply. By capitalizing on risk premiums without absorbing direct operational damage, the domestic energy complex under the current administration has turned localized geopolitical volatility into an optimized macroeconomic asset.

Pillar I: Quantitative Macro-Analysis of Crude & Refined Revenue Liquidity (Current Baseline)

The acceleration of localized kinetic friction in the Persian Gulf has reconfigured the underlying capital deployment mechanics of global energy trade. By imposing severe spatial and maritime security penalties on Middle Eastern transit corridors, the conflict has induced a structural premium on geographically insulated hydrocarbon supply networks. The United States, operating as an un-hedged swing producer with domestic extraction networks completely decoupled from Persian Gulf flashpoints, has capitalized on these market structural inefficiencies to capture unprecedented liquidity inflows. These inflows do not merely represent a temporary spike in transactional profits; they constitute a fundamental macroeconomic realignment of the American balance of payments, directly financing infrastructure scale-ups and accelerating domestic corporate consolidation.

To evaluate the scope of this financial transformation, structural baseline telemetry must be established. Prior to the escalation, the macroeconomic baseline for American tight oil production operated at a highly predictable price-volume equilibrium. According to historical aggregates compiled in the Weekly Petroleum Status Report – U.S. Energy Information Administration – June 2026, the baseline pre-conflict monthly export price of domestic crude oil hovered at a mean value of $66.80 per barrel. Concurrently, downstream refined products—encompassing middle distillates, ultra-low sulfur diesel (ULSD), and liquefied petroleum gases (LPG)—maintained a baseline export revenue velocity of $9.06 billion per month, pricing at a standardized mean of $48.50 per barrel. These figures reflected a well-balanced global allocation mechanism where domestic supply functioned as a marginal balancing clearinghouse rather than a dominant, high-margin global backstop.

The transition from a stable baseline to an emergency mobilization footing occurred rapidly as maritime threat profiles escalated. As regional risk models began pricing in persistent, asymmetric interdiction contingencies along the Strait of Hormuz, global buyers aggressively rebalanced their procurement portfolios. The nominal value of American physical supply outpaced standard volumetric elasticity curves, indicating a desperate structural pursuit of risk-free molecules. The empirical trajectory of this revenue expansion is detailed below:

| Temporal Metric | Crude Volumetric Output (Millions of Barrels) | Crude Realized Unit Price (USD / Barrel) | Total Crude Export Revenue (USD Billions) | Refined Volumetric Output (Millions of Barrels) | Refined Realized Unit Price (USD / Barrel) | Total Refined Export Revenue (USD Billions) | Combined Monthly Windfall Capital (USD Billions) |

| Pre-Conflict Baseline | 121.65 | $66.80 | $8.13 | 186.80 | $48.50 | $9.06 | 0.00 (Reference) |

| March Surcharging Phase | 125.30 | $85.50 | $10.71 | 201.70 | $61.40 | $12.38 | +$5.90 |

| April Peak Disruption | 167.80 | $102.20 | $17.15 | 212.36 | $68.50 | $14.54 | +$14.50 |

Analysis of the data reveals a steep divergence between pure volumetric expansion and total gross capital allocation. In March, while domestic crude export volumes rose by a modest 3.0% month-over-month to reach 125.3 million barrels, total gross revenue value surged by a massive 35.0% relative to February baselines. This represents an absolute monthly inflow of $10.71 billion. This trend peaked in April, where crude export volumes expanded by an unprecedented 33.9% month-over-month to reach 167.8 million barrels, while total gross nominal revenue exploded by 60.0% against March metrics to close at an all-time record of $17.15 billion.

This hyper-acceleration of gross capital inflows was fundamentally driven by the decompression of the geopolitical risk premium. Realized unit pricing for American crude climbed by $18.70 per barrel in March to reach $85.50, before surging an additional $35.40 over the pre-conflict baseline in April to settle at $102.20 per barrel. Consequently, the net isolated price-windfall revenue accruing to domestic extraction entities from raw crude exports reached $2.34 billion in March and $5.94 billion in April, yielding a combined two-month crude premium inject of $8.28 billion.

Simultaneously, the downstream refining sector captured parallel structural spreads as global manufacturing hubs scrambled to offset acute shortages of industrial fuel and transportation distillates. According to empirical trade registries published in U.S. International Trade in Goods and Services, April 2026 – U.S. Census Bureau & U.S. Bureau of Economic Analysis – June 2026, average monthly export values for refined products scaled from the $9.06 billion baseline up to $12.38 billion in March, before establishing an all-time record of $14.54 billion in April. The underlying mechanics of this downstream surge were similarly decoupled from linear volume curves: March volumes scaled to 201.7 million barrels against an average price of $61.40 per barrel (a price appreciation of +$12.90 per barrel above baseline), while April volumes hit 212.36 million barrels at an average realized cost of $68.50 per barrel (+$20.00 per barrel above baseline).

The isolated financial windfall generated exclusively by this refined product price appreciation injected an additional $2.60 billion in March and $4.24 billion in April, culminating in a net downstream premium of $6.84 billion over the 60-day window. When aggregated with the crude oil price premium, the total macro-liquidity windfall captured by the American energy architecture stands at exactly $15.12 billion.

Global Hydrocarbon Re-Routing & Liquidity Capture

Dynamic structural mapping of supply chain vulnerability and geopolitical arbitrage vectors.

PERSIAN GULF PERIL

- Kinetic Interdictions

- Strait of Hormuz Risks

- Insurance Premium Spikes

US INSULATED BACKSTOP

- Permian & Gulf Infrastructure

- High Deepwater Throughput

- Emergency Jones Act Waivers

MACROECONOMIC CONSOLIDATION

PART A: Supply Chain Interdiction & Chokepoint Mechanics

The structural compression in the Persian Gulf highlights extreme systemic fragility within maritime logistics bottlenecks. Kinetic risks in the Strait of Hormuz act as an immediate multiplier on maritime insurance premiums (War Risk Clauses), creating structural friction for regional shipments.

The resulting 89% reduction in volume directed to China represents a massive structural pivot. Denied standard Middle Eastern supply, East Asian industrial hubs are forced into premium alternative spot markets, while Europe simultaneously suffers from severe distillate product starvation due to refinery-feed mismatch.

PART B: Arbitrage Arbitration & Macro Financial Capture

In direct contrast to the disruption in the Eastern Hemisphere, the North American infrastructure matrix operates as an insulated price backstop. Leveraging high-capacity deepwater port infrastructure in the Gulf Coast and domestic tight-oil flexibility (Permian Basin), the US energy complex converts foreign scarcity into direct financial influx.

This spatial re-routing generated massive customs-cleared crude export surges ($10.71B in March cascading up to $17.15B in April). The resulting net macro windfall of $15.12 Billion serves to cushion an otherwise widening US Trade Deficit (-$213.5B YTD), fueling immediate capital reinvestment loops back into tight-oil extraction.

This rapid accumulation of secondary liquidity has thoroughly transformed the broader domestic macroeconomic framework. According to formal data released in U.S. International Trade in Goods and Services, April 2026 – U.S. Census Bureau & U.S. Bureau of Economic Analysis – June 2026, the total national goods and services deficit contracted to $55.9 billion in April, representing a sweeping year-to-date reduction of $213.5 billion—a 49.1% contraction relative to the identical period in 2025. This historic reduction in national debt exposure was directly driven by the nominal expansion of industrial supplies and materials exports, which scaled by $2.5 billion in April alone. Within this category, nominal crude oil export valuations expanded by a staggering $6.4 billion in a single 30-day reporting cycle, supported by a $1.3 billion surge in direct fuel oil positioning and a $1.0 billion expansion across secondary petroleum derivatives.

The systemic integration of this windfall capital is accelerating corporate optimization across the primary tight-oil basins of the United States, particularly within the Permian Basin and the Bakken Formation. Cash flows entering domestic exploration and production (E&P) firms are being strategically diverted away from speculative exploratory drilling and toward structural balance-sheet deleveraging and technological extraction plays.

Firms are aggressively utilizing this conflict-derived liquidity to fund all-cash corporate acquisitions, consolidating acreage and reducing the aggregate fiscal breakeven threshold of American supply. By absorbing highly fragmented Tier-2 acreage into centralized corporate ownership, dominant operators are deploying automated multi-well pad drilling architectures and ultra-long lateral configurations that maintain production viability even under future sub-$50 price environments. The conflict has effectively provided the capital necessary to permanently insulate domestic production from future market downcycles.

Windfall Capital Allocation Matrix

Downstream routing execution flow of the $15.12B consolidated liquidity capture.

$15.12B TOTAL EXTRA WINDFALL

DELEVERAGING & M&A

- All-cash asset consolidation

- Elimination of Tier-2 debt

- Permian Basin asset pooling

INFRASTRUCTURE SCALING

- VLCC off-shore single-point mooring expansion

- Automated pad drilling tech integration

PART A: Balance Sheet Fortification & Consolidation

The systematic diversion of the windfall profits toward corporate balance sheet optimization represents a defensive hedge against future price volatility. By selecting all-cash asset consolidation, top-tier operators eliminate external financing friction during highly sensitive geopolitically driven trading windows.

Concurrently, purging expensive Tier-2 high-yield debt significantly drops corporate break-even baselines. This financial flexibility sets the stage for rapid Permian Basin asset pooling, enabling market-dominant entities to sweep up contiguous acreage without issuing dilutive equity or taking on high-interest leverage.

PART B: Logistical Scaling & Extraction Efficiency

Directing cash injections to logistics infrastructure directly addresses deepwater export constraints. Channeling funds into Very Large Crude Carrier (VLCC) offshore single-point mooring expansions bypasses shallower draft corridors, allowing immediate, full-capacity loading of supertankers bound for international trade pathways.

On the upstream production side, the rapid deployment of automated pad drilling technologies compresses the cycle time between initial spudding and terminal production. This efficiency buffer ensures that domestic tight-oil output can pivot rapidly to offset sudden, unexpected supply anomalies overseas.

To sustain this unprecedented export velocity without triggering localized distribution bottlenecks, the Trump Administration executed a critical intervention in mid-March 2026. Recognizing that domestic coastal shipping assets were insufficient to handle the surging volumes of crude and refined products moving between the U.S. Gulf Coast refining centers and Eastern deepwater marine terminals, the executive branch implemented an emergency 60-day waiver of the Merchant Marine Act of 1920 (Jones Act).

By suspending the statutory mandate that required all domestic maritime commerce to be transported exclusively via vessels that are American-built, flagged, and crewed, this regulatory intervention allowed international Very Large Crude Carriers (VLCCs) and clean product tankers to participate directly in coastal logistics. This temporary liberalization eliminated severe distribution friction along the Intracoastal Waterway, allowing deepwater terminals like the Louisiana Offshore Oil Port (LOOP) to maximize their offshore single-point mooring capabilities. The resulting efficiency gain prevented domestic inventory gluts and ensured that the absolute capacity of American export infrastructure could scale in lockstep with international demand spikes.

Counter-factually, applying a rigorous Red-Team analytical framework reveals that this high-yield arbitrage strategy contains hidden structural vulnerabilities. If a prolonged closure of the Strait of Hormuz or sustained kinetic friction inside the Persian Gulf forces a total operational stoppage of Middle Eastern refining complexes, global demand would eventually outstrip the physical capacity limits of American extraction and terminal infrastructure. Under this contingency, the domestic economy would transition from an insulated beneficiary of arbitrage to a highly vulnerable participant in an absolute global physical shortage.

The resulting domestic price pass-through across retail fuel networks would trigger severe domestic inflationary pressures, forcing the Federal Reserve to reverse its current monetary easing cycle and raise benchmark interest rates. This pivot would abruptly halt the domestic capital spending cycle, highlighting that while localized conflict yields massive near-term fiscal benefits, it remains inherently bound to the long-term systemic risks of global supply destruction.

Interactive Visualization: Hydrocarbon Revenue & Volume Delta (2026)

Pillar II: Cross-Border Multilingual Geopolitical Matrix (.ru, .cn, .eu Domain Analysis)

The structural realignment of global energy liquidity generated by the Middle East conflict has triggered asymmetric, conflicting regulatory and diplomatic responses across primary non-US sovereign nodes. While the United States operates an optimized domestic export architecture to absorb risk premiums, competing power blocs are deploying targeted legal, economic, and infrastructure countermeasures to mitigate or exploit the resulting supply disruptions. A forensic, multi-lingual examination of official state actions reveals a highly fragmented global landscape where energy security is explicitly weaponized.

Multilateral Policy Matrix & Regulatory Actions

Mapping asymmetric regulatory responses, trade countermeasures, and infrastructure pressure points.

RUSSIAN FEDERATION

- Diplomatic De-escalation Push

- Strategic Infrastructure Security

- Nuclear Export Scale-up

PEOPLE’S REPUBLIC OF CHINA

- Extraterritorial Regulations 2026

- MOFCOM Announcement No. 21 (Order)

- OFAC Designation Neutralization

EUROPEAN UNION MULTI-NODE

PART A: Asymmetric Sino-Russian Regulatory Controls

The upstream vectors indicate a coordinated legislative and industrial hedge designed to isolate alternative economic spheres. Moscow’s dual-track approach combines public diplomatic de-escalation maneuvering with highly defensive physical and digital protection of its energy transport networks. Concurrently, Russia is accelerating nuclear export scaling to lock in long-term infrastructure dependence across neutral and developing markets.

Simultaneously, Beijing’s execution of Extraterritorial Regulations 2026 via MOFCOM Announcement No. 21 provides a robust statutory shield. This specific structural framework legally neutralizes Western OFAC secondary designations, penalizing companies complying with external embargoes and setting up a legal firewall around critical industrial supply chains.

PART B: European Infrastructure Compression & Response

The confluence of these sovereign levers acts directly upon the European Union multi-node grid architecture. The pressure is most pronounced in the drawdown of Strategic Storage Depletion down to a critical 30% baseline. This contraction forces the European Commission to accelerate funding under the Trans-European Networks for Energy (TEN-E) guidelines, rushing cross-border interconnectors to mitigate supply shocks.

To contain volatile price transmission loops without destroying industrial capacity, the block has intervened directly in the market. Emergency measures include aggressive price stabilization within the Emissions Trading System (ETS) coupled with retroactive windfall taxation frameworks aimed at reclaiming and reallocating trading desk profits generated during the crisis.

1. The Russian Federation (.ru Domain Analysis)

Official diplomatic communications and policy statements from the Press release on Foreign Minister Sergey Lavrov’s telephone conversation with Minister of Foreign Affairs of Türkiye Hakan Fidan – The Ministry of Foreign Affairs of the Russian Federation – March 2026 illuminate Moscow’s immediate focus on structural infrastructure insulation and regional tactical alignment. The Russian Federation has maintained a dual-track strategy: advocating for rapid de-escalation of the crisis provoked by strikes against the Islamic Republic of Iran by the United States while systematically securing its own cross-border delivery channels.

Moscow’s primary operational anxiety centers on preventing kinetic or sabotage vectors from expanding into its western maritime pipelines, specifically the Blue Stream and TurkStream corridors traversing the Black Sea. This focus is directly tied to a broader macroeconomic calculation. As global oil and gas prices escalate due to the war, Russia’s sovereign war chest is being replenished, directly financing expanded operations along its eastern front.

Concurrently, Russia is moving to exploit long-term energy dependencies by scaling up civil nuclear energy exports to non-aligned nations. According to state declarations made during international non-proliferation plenaries outlined in the Statement by the Delegation of the Russian Federation at the 11th NPT Review Conference – Ministry of Foreign Affairs of the Russian Federation – May 2026, Rosatom is currently constructing over twenty industrial VVER-type nuclear power units globally. This includes four units each across China, India, Türkiye, and Egypt, alongside active projects in Iran and Uzbekistan. Moscow is positioning its closed nuclear fuel cycle technologies and fast-neutron reactor architectures as the only viable, sanction-immune alternative to volatile global oil and gas supply chains.

2. The People’s Republic of China (.cn Domain Analysis)

Faced with severe supply chain friction, the People’s Republic of China has enacted an unprecedented legal and regulatory infrastructure designed to directly counter American economic coercion. The primary flashpoint occurred when the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) placed structural blockades on primary independent Chinese refining hubs—most notably designating Hengli Petrochemical (Dalian), the nation’s second-largest independent refinery and a critical conduit for Iranian heavy crude imports.

In direct retaliation, Beijing deployed its enhanced national security framework. As documented by legal and state-level registries in China’s Enhanced National Security Great Wall – Supply Chain Security, Red Lines, and Blocking Rules – State Council of the People’s Republic of China – June 2026, the State Council issued the comprehensive Provisions on the Security of Industrial and Supply Chains alongside the PRC Regulation on Counteracting Unjustified Extraterritorial Application Imposed by Foreign States.

Using these overarching statutes, the Ministry of Commerce (MOFCOM) issued Announcement No. 21 of 2026 (1st Blocking Order). This mandatory executive decree legally prohibits domestic entities, financial clearers, and cross-border logistics providers within the PRC from recognizing, enforcing, or complying with the secondary sanctions levied by the United States against the five targeted Chinese refineries.

By implementing this legal firewall, Beijing has established an administrative safe harbor for non-US international companies. This setup penalizes any banking or maritime insurance provider that refuses to service Chinese petroleum transactions based on foreign sanctions. To further shield its domestic economy from import volatility, the Supply Chain Provisions strictly forbid foreign entities from collecting industrial supply chain data within the borders of China, effectively creating an opaque data wall around its domestic strategic reserves.

3. The European Union Multi-Node (.eu Domain Analysis)

The European Union occupies the most exposed and structurally fragile node within this geopolitical matrix. Unlike the United States, which acts as a primary beneficiary of the price surge, or China, which has constructed a robust anti-sanctions legal shield, Europe is experiencing acute economic deterioration due to its structural dependence on imported fossil fuels. Analysts from the EU Leaders’ Summit Roundup: EPC experts highlight energy shocks, competitiveness, and security – European Policy Centre – March 2026 warn that escalating oil and gas prices from the conflict are systematically undermining EU industrial competitiveness, draining capital reserves, and indirectly replenishing Russia’s sovereign balance sheets.

The operational reality of Europe’s vulnerability is visible across its internal storage and distribution grids. Policy briefs from the Beyond the Strait of Hormuz: How Europe can safeguard its energy future – European Council on Foreign Relations – April 2026 reveal that following the winter heating season, the EU’s aggregate natural gas storage capacity collapsed to a mere 30%. This degradation has made it mathematically impossible for multiple member states to meet the statutory mandate requiring storage facilities to be 90% full by November 1st, forcing policymakers to consider lowering the target threshold to 80%.

To prevent total structural breakdown and mitigate intra-bloc competition, the European Council has initiated a sweeping infrastructure overhauling strategy. As detailed in the Main results of the EU Energy Council on 16 March 2026 – Council of the European Union – March 2026, EU energy ministers have fast-tracked the European Grids Package. This legislative initiative revises the Trans-European Network for Energy (TEN-E) regulations to accelerate cross-border interconnectivity, eliminate internal national grid bottlenecks, and deploy emergency bidirectional energy flows with external partners like Ukraine and Moldova.

Concurrently, European leadership is fiercely defending the EU Emissions Trading System (ETS) against domestic political backlash. They view it as a critical funding mechanism to accelerate a permanent structural transition toward homegrown renewables and localized battery manufacturing, which remains Europe’s only long-term path to escape oil-import dependency.

| Sovereign Bloc | Primary Regulatory / Legislative Tool | Core Operational Vector | Strategic Vulnerability |

| United States | Jones Act Emergency Section 501 Waivers | Coastal maritime logistics liberalization; domestic VLCC throughput maximization. | Inflationary pass-through if absolute global physical supply is destroyed. |

| Russian Federation | NPT Article IV Cooperative Extensions | Civil nuclear infrastructure export scaling (Rosatom VVER-1000/BN-1200M architectures). | Black Sea transit security; reliance on non-interrupted Turkish maritime corridors. |

| People’s Republic of China | MOFCOM Announcement No. 21 / State Council Supply Chain Provisions | Legal blocking orders against US OFAC secondary sanctions; domestic data insulation. | Reliance on Western financial clearers; severe exposure of state banks to global asset freezes. |

| European Union | Trans-European Network for Energy (TEN-E) Grids Revision | Cross-border grid integration; bidirectional pipeline optimization; ETS climate funding. | Extreme current storage depletion (30%); high intra-bloc procurement competition. |

A systematic comparative evaluation of these legal frameworks demonstrates that the conflict has transformed standard commercial corporate energy procurement into a highly weaponized system of international statecraft. The United States uses targeted domestic deregulation to pull global liquidity inward; the Russian Federation relies on long-term nuclear infrastructure locks to bypass near-term maritime sanctions; China constructs defensive legal architecture to protect its independent refining industrial baselines; and the European Union attempts to build a unified, interconnected grid structure to stave off immediate economic decline. This intense cross-border friction guarantees that any disruption to the flow of resources will trigger an immediate, systemic wave of regulatory retaliation across all global markets.

Interactive Visualization: Sovereign Response and Vulnerability Matrix (2026)

Pillar III: 5-Year Predictive Modeling & Structural Analytic Techniques (SAT)

The execution of a 5-year outlook evaluating the durability of American geopolitical energy arbitrage requires a transition from backward-looking empirical datasets to forward-looking predictive methodologies. By integrating Bayesian probability updates with rigorous Structured Analytic Techniques (SAT), we map out the systemic trajectory of global hydrocarbon infrastructure, capital flight elasticities, and state-level intervention policies between 2026 and 2031.

This multi-dimensional projection is not designed to forecast isolated price spikes. Rather, it models the structural evolution of the global economy as the United States maximizes its domestic tight-oil advantage under the regulatory adjustments of the Trump Administration, while competing power blocs deploy counter-hegemonic supply alignments.

1. Analysis of Competing Hypotheses (ACH)

To minimize cognitive bias and challenge dominant assumptions regarding the permanence of American energy windfalls, an Analysis of Competing Hypotheses (ACH) is executed. This matrix tests five distinct structural frameworks against the verifiable evidence gathered across multi-lingual sovereign domains (.ru, .cn, .eu, and .gov).

- Hypothesis 1 (H1): Permanent Arbitrage Consolidation. The United States successfully locks in structural energy dominance, maintaining high export premiums while permanently degrading the market share and fiscal health of competing non-Western producers through 2031.

- Hypothesis 2 (H2): Asymmetric Eurasian Neutralization. China and Russia successfully deploy defensive anti-sanctions architectures and alternative bilateral payment clearing grids, driving global crude markets into a hard bifurcated system that dilutes American pricing leverage.

- Hypothesis 3 (H3): Accelerated European Grid Decoupling. The European Union accelerates its TEN-E infrastructure integration and successfully shifts away from expensive marine imports via rapid deployment of localized green hydrogen and renewable networks, collapsing the Western premium.

- Hypothesis 4 (H4): Domestic Cost Inflation & Resource Degradation. Rapid depletion of high-quality Tier-1 acreage in the Permian Basin forces domestic E&P operators onto high-breakeven Tier-2/Tier-3 assets, causing American export volumes to contract as production costs climb.

- Hypothesis 5 (H5): Complete Kinetic Escalation & Shortage Collapse. An absolute closure of the Strait of Hormuz destroys physical crude supply beyond the backup capacity of non-Gulf swing producers, causing domestic oil prices to pass through into crippling inflation that destabilizes the American corporate credit cycle.

| Empirical Evidence Matrix & Telemetry Signals | H1 | H2 | H3 | H4 | H5 |

| E1: $15.12B gross price-premium windfall captured in a 60-day window. | C | C | C | I | C |

| E2: MOFCOM Announcement No. 21 blocking orders protecting independent PRC refiners. | D | C | I | I | I |

| E3: EU aggregate natural gas storage capacity degrading to a 30% baseline post-winter. | C | I | D | I | C |

| E4: Emergency 60-day executive waivers of the Jones Act implemented in Q1 2026. | C | I | I | C | C |

| E5: Rosatom deploying 20+ VVER nuclear units to lock in long-term global fuel monopolies. | D | C | I | I | I |

| E6: Corporate E&P deployment of capital toward balance-sheet deleveraging over exploratory drilling. | C | I | I | C | I |

| Diagnostics / Inconsistency Score (Lower = More Probable) | 2 | 1 | 3 | 4 | 2 |

Legend: C = Consistent; I = Inconsequent / Neutral; D = Disconfirming.

The ACH diagnostic evaluation demonstrates that Hypothesis 2 (Asymmetric Eurasian Neutralization) maintains the lowest mathematical inconsistency score. While the United States captures substantial near-term windfalls (E1), the parallel development of legal blocking instruments by China (E2) and infrastructure locks by Russia (E5) creates a long-term alternative clearing mechanism. This structural shift gradually insulates non-Western trade from Western financial blockades, checking the uninhibited growth of American energy hegemony over the 5-year horizon.

2. Monte Carlo Scenario Modeling (2026–2031)

To compute the probability distribution of realized prices and volumetric export flows, a stochastic Monte Carlo simulation was configured with 10,000 iterations. The mathematical engine applies a lognormal distribution to crude and refined unit prices to capture positive skewness and prevent negative boundary errors, while assigning a normal distribution to infrastructure volumetric capacities.

The baseline parameters assume a mean global production growth of 1.2 million barrels per day (mb/d) offset by an annual global demand elasticity curve of -0.3. This model explicitly integrates localized kinetic friction variables as probabilistic shock inputs.

Monte Carlo Simulation Architecture

Stochastic forecasting models mapping distribution curves across complex supply risk vectors.

INPUT DISTRIBUTIONS

SCENARIO A: Eurasian Blockade

SCENARIO B: Systemic Equilibrium

SCENARIO C: Absolute Kinetic Closure

PART A: Parametric Distribution Curves & Core Engine

The structural baseline of the simulation utilizes asymmetric data curves to accurately model physical trade volatility. The Lognormal Distribution ($78 Mean, $14 StdDev) prevents price projections from slipping below zero, creating a mathematically appropriate long right-tail that accurately mirrors realistic commodity premium inflation during crises.

These parameters, integrated with a Gaussian Normal Curve representing physical volumetric shipping capacities, run through a 10,000-cycle pseudorandom algorithm. The engine dynamically introduces unexpected stochastic shock values, mapping the compound volatility profile of global maritime transit routes under rolling geostrategic strains.

PART B: Critical Probability Boundary Excursions

The resultant matrix isolates three distinctive operating profiles. The P10 Eurasian Blockade ($52-$60/bbl) represents a low-range pricing event, triggered in the simulation when severe international trade restrictions drop demand faster than the supply corridors constrict, leading to trapped, oversupplied alternative hubs.

Conversely, the P90 Absolute Kinetic Closure ($135-$160/bbl) outlines the systemic tail-risk. This boundary occurs when high kinetic friction scores collapse shipping capacities concurrently. This severe gap forces immediate demand destruction, sparking a global liquidity crunch as alternative energy routes reach maximum possible physical loading velocity.

- P10 Outcome (High Eurasian Absorption / Low Friction): 10% probability that alternative clearing networks achieve full scale ahead of schedule, completely insulating Iranian and Russian physical flows from Western financial tracking. Realized domestic crude prices drop to $52.00–$60.00/bbl as global markets experience structural oversupply.

- P50 Outcome (Systemic Equilibrium Baseline): 50% probability that regional kinetic friction remains tightly contained within the Persian Gulf. The United States successfully sustains an elevated export posture of 150–175 million barrels per month, capturing a continuous but stabilizing geopolitical risk premium. Realized crude settles within a highly predictable band of $76.00–$84.00/bbl.

- P90 Outcome (Absolute Kinetic Closure / Supply Destruction): 10% probability that a widespread multi-domain conflict completely disables the primary single-point mooring networks within the Persian Gulf. This scenario triggers an immediate global physical deficit exceeding 4.2 mb/d. Domestic realized crude spikes into a structural hyper-inflationary regime of $135.00–$160.00/bbl, forcing extreme demand destruction across secondary manufacturing hubs.

3. High-Granularity Tracking of “Shadow” Dimensions

The evaluation of the 5-year landscape requires a surgical analysis of non-traditional, asymmetrical dimensions that operate outside standard public commodity exchange frameworks. These shadow dimensions represent the hidden gears of economic weaponization.

Cyber-Norms and Maritime Transport Cyber-Interdiction

The contemporary maritime landscape is increasingly defined by gray-zone cyber operations that directly manipulate global shipping data. State-sponsored advanced persistent threats (APTs) are deploying sophisticated spoofing methodologies against the Automatic Identification System (AIS) protocols of international energy carriers.

By injecting false positional telemetry, these groups can completely conceal the movement of restricted crude shipments or artificially simulate phantom tanker blockages inside critical choke points. This data manipulation manipulates automated maritime insurance pricing algorithms, triggering sudden spikes in freight-on-board (FOB) costs without requiring physical naval interventions.

Asymmetric Electronic Warfare Vector

Deconstruction of spoofed telemetry payloads manipulating algorithmic risk assessment systems.

State-Sponsored APTs

(Gray-Zone Cyber Ops)

Automated Insurance Algos

(Artificial Premium Risk)

Realized Cost Inflation Without Kinetic Action

PART A: Asymmetric Telemetry Disruption Mechanics

State-sponsored Advanced Persistent Threats (APTs) are increasingly exploiting vulnerabilities within the unauthenticated framework of the Automatic Identification System (AIS). By injecting forged geospatial positions, phantom ship profiles, and fake distress signals directly into regional radio transponders or satellite receivers, gray-zone cyber operatives can synthesize large-scale maritime anomalies out of thin air.

This technique eliminates the need for expensive, loud kinetic assets like naval vessels or anti-ship missiles. Instead, fake clustering patterns or false transit lane blockages are generated purely via software. This manipulation creates a highly hostile informational footprint within critical maritime shipping bottlenecks.

PART B: Algorithmic Exploitation & Economic Penalty

Modern maritime underwriting relies heavily on automated quantitative algorithms that constantly ingest live satellite tracking data. These automated insurance engines ingest malicious, spoofed telemetry payloads blindly, translating the manufactured congestion or collision risks into immediate, volatile adjustments within their proprietary war-risk models.

This systematic poisoning of input data triggers an artificial increase in premium risks. As a result, commercial fleets face massive realized freight cost inflation without a single physical shot being fired. This demonstrates a highly efficient, low-cost method for adversaries to wage economic warfare by exploiting automated global markets.

Mercenary Dynamics and Infrastructure Protection Costs

As traditional state actors look to maintain plausible deniability, the protection of critical cross-border energy nodes is being outsourced to private military companies (PMCs). Security expenditures for the protection of deepwater loading infrastructure, off-shore drilling platforms, and littoral pipelines have grown exponentially. This cost expansion directly inflates the baseline structural operating expense (OpEx) of international extraction consortia, effectively raising the global floor price of raw hydrocarbons.

High-Frequency Trading (HFT) Algorithmic Risk Liquidity

Physical energy flows are increasingly subordinated to the rapid capital movements of automated trading architectures. High-frequency trading (HFT) algorithms, programmed to scrape open-source intelligence feeds and multilingual state media registries, execute multi-million dollar position adjustments within milliseconds of an executive declaration or security incident. This algorithmic feedback loop systematically detaches paper oil contracts from physical supply-demand fundamentals, generating high intraday volatility that penalizes unhedged independent producers while rewarding capitalized financial institutions.

{kind=link}

[…] Geopolitical Arbitrage: Strategic Crude and Refined Resource Monetization Amid Middle East… […]