Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

ABSTRACT

The meeting between Hungarian Prime Minister Viktor Orbán and Russian President Vladimir Putin in Moscow on 28 November 2025 crystallizes a structural contradiction at the heart of the European Union’s Russia policy: while most member states seek to phase out Russian fossil fuels, Hungary is deepening a highly asymmetric but mutually beneficial energy partnership with Moscow. According to convergent reporting by major wire services and Russian state media, Orbán’s priority in Moscow is to secure continued flows of Russian crude oil and natural gas for the coming winter and the next year, under the protection of a recent U.S. sanctions exemption that shields Hungary’s Russian energy transactions from secondary sanctions. (Reuters) The meeting is explicitly framed around energy security and implicitly linked to ongoing diplomatic manoeuvres over the war in Ukraine, where Budapest positions itself as a dissident EU and NATO voice arguing for negotiated accommodation rather than indefinite escalation.

Hungary’s structural dependence on Russian hydrocarbons remains unusually high by EU standards, despite continent-wide efforts to reduce exposure after the full-scale invasion of Ukraine in 2022. International Energy Agency data show that oil products accounted for the largest share of Hungary’s final energy consumption in 2023, at roughly 39 %, followed by natural gas at around 27 %, underlining the centrality of liquid fuels and gas in the country’s energy mix. (IEA) Although EU-wide Russian gas reliance has fallen sharply—to about 14 % of total gas consumption in 2024, down from roughly 45 % before the war—analytical work on Central Europe highlights Hungary, alongside Slovakia and Austria, as among the most exposed to the loss of Russian pipeline deliveries. (Ember Energy) In this context, Orbán’s insistence on maintaining Russian supplies, and his willingness to accept political isolation within EU forums to do so, reflects not only ideological affinity with Moscow but also a sober reading of Hungary’s immediate energy-security constraints.

The gas relationship with Russia is anchored in a long-term supply architecture that pre-dates the current crisis but has been actively reinforced since 2021. In September of that year, Hungarian state wholesaler MVM CEEnergy and Gazprom Export signed a 15-year contract to supply up to 4.5 billion cubic metres (bcm) of gas annually, with volumes delivered mainly via the TurkStream pipeline and related southern corridors, thereby circumventing the Ukrainian transit route. (IEA) Subsequent analyses document that Budapest quickly sought additional volumes under this framework as prices surged in 2022, and by August 2025 Russian gas deliveries via TurkStream to Hungary had reached a record 5 bcm for the year, even as other EU states curtailed imports. (jamestown.org) The 2025 Engie and Shell liquefied natural gas (LNG) deals—amounting to roughly 400 million cubic metres per year from Engie between 2028–2038 and 200 million cubic metres per year from Shell starting in 2026—will cover only about 5 %–7 % of Hungary’s current annual gas consumption of approximately 8 bcm, underlining that diversification measures are additive rather than substitutive and leave the core Russian contract intact. (Reuters)

On the oil side, Hungary’s relationship with Russia is dominated by pipeline-borne crude delivered through the southern branch of the Soviet-era Druzhba system. The EU’s sixth sanctions package in 2022 banned seaborne Russian crude and refined products but granted a temporary exemption for pipeline deliveries, effectively preserving Druzhba flows to landlocked Hungary and Slovakia. (europarl.europa.eu) Subsequent policy work on Central Europe’s energy transition stresses that this carve-out turned Hungary into a residual market for Russian pipeline oil within the EU, even as seaborne imports were phased out. (energyandcleanair.org) However, military and sabotage risks have increasingly transformed this legal privilege into an operational vulnerability. In March 2025, a Ukrainian drone strike on Druzhba infrastructure temporarily halted oil shipments to Hungary and Slovakia, and in August 2025 Budapest reported a further suspension of Russian crude deliveries after another attack, underscoring the insecurity of relying on a single transit corridor through an active war zone. (Reuters) Orbán’s Moscow agenda therefore also seeks assurances on the resilience and scheduling of crude flows, even as Hungary simultaneously explores additional pipeline connections with Serbia that could move several million tonnes of Russian oil annually by 2028. (Reuters)

Nuclear cooperation forms the second strategic pillar of Hungary’s entanglement with Russia and is less immediately substitutable than oil or gas. The Paks Nuclear Power Plant—four Soviet-designed VVER-440 reactors with combined capacity in the 1.9–2.0 GWe range—has long supplied around half of Hungary’s domestic electricity generation and roughly one-third of final electricity demand, according to the World Nuclear Association and operator reporting. (world-nuclear.org) The Paks II expansion project, agreed in 2014 with Russian state corporation Rosatom, foresees the construction of two VVER-1200 units of about 1,200 MW each. (Balkan Green Energy News) Russian and Hungarian officials consistently place the total project cost above €12.5 billion, backed by a Russian state loan facility of up to €10 billion, embedding Hungary’s power sector in a long-term debt and technology relationship with Moscow. (TASS) In 2025, Hungary’s foreign minister announced that full-scale construction is expected to begin in early 2026, and Rosatom communications emphasise that the project remains a flagship of Russian nuclear export strategy in the EU. (nucnet.org)

At the same time, Budapest has quietly diversified parts of its nuclear fuel cycle away from exclusive Russian control. In early 2025, a U.S.–Hungarian nuclear cooperation arrangement was publicized under which American fuel can be used at Paks I, complementing Russian-supplied assemblies. (Reuters) This dual-sourcing approach mirrors broader EU efforts to reduce dependence on Russian nuclear fuel while avoiding abrupt supply disruptions. Orbán’s Moscow visit thus occurs within a complex triangular setting in which Hungary relies on Russia for new reactor construction and much of its operating know-how, but signals openness to Western suppliers for fuel and selected services, leveraging competition between Russian and U.S.–European vendors to obtain more favourable contractual terms.

Beyond hydrocarbons and nuclear power, Hungary and Russia have cultivated sector-specific economic ties that reinforce the political relationship. Pre-war trade data from UN Comtrade and derivative compilers indicate that Hungarian exports to Russia exceeded $1 billion in 2024, with pharmaceuticals constituting a central pillar. (Trading Economics) Studies of Russian–Hungarian pharmaceutical alliances describe a pattern in which Hungarian firms provide high-value medicines and know-how, while Russian partners offer market access and local production capacity, generating joint ventures that can partially bypass Western sanctions regimes targeting Russia’s broader industrial base. (Portale di Periodici Scientifici RUDN) This sectoral interdependence is politically salient because it creates a lobby within Hungary—concentrated in export-oriented manufacturing and R&D—that favours maintaining stable relations with Moscow irrespective of wider EU sanction dynamics.

Infrastructure and logistics initiatives add a further layer of path dependency. In December 2021, Russian Railways Holding, Hungary’s CER Cargo Holding and Austria’s Rail Cargo Group agreed to establish a joint venture to act as a freight forwarder and logistics provider on China–Europe rail routes associated with Beijing’s Belt and Road Initiative. (RailFreight.com) While the war in Ukraine and subsequent sanctions significantly constrained east–west overland cargo flows through Russia, the institutional and corporate frameworks created by this joint venture remain in place as a potential vehicle for future cooperation, particularly if a negotiated settlement alters the current geopolitical environment. For Moscow, the persistence of such arrangements underscores that at least one EU and NATO member state remains open to integrating Russian transport corridors into broader Eurasian connectivity schemes; for Budapest, they represent an option value on a possible future in which Hungary functions as a logistics hub between European and Eurasian markets.

Hungary’s political positioning within EU and NATO structures amplifies the leverage both sides derive from the energy relationship. Analyses by European policy institutes and official EU communications describe a pattern in which Budapest has repeatedly vetoed, delayed or diluted joint decisions on Russia, including sanctions packages and macro-financial aid for Ukraine, while arguing that punitive measures against Russian energy exports harm Central European consumers more than they constrain Moscow’s warfighting capacity. (Bruegel) Orbán’s government frames this stance as a defence of national sovereignty and economic pragmatism, insisting that affordable Russian energy is indispensable for preserving Hungary’s industrial competitiveness and domestic price-control schemes. Russia, in turn, gains the practical advantage of at least one EU capital willing to challenge collective decisions, as well as the symbolic benefit of high-profile meetings between Putin and a sitting EU head of government, which can be portrayed domestically as evidence that Western isolation is incomplete.

The 28 November 2025 Moscow talks therefore sit at the intersection of three overlapping logics: Hungary’s search for guaranteed oil, gas and nuclear inputs under adverse market and security conditions; Russia’s effort to preserve a foothold inside the EU energy and political space despite extensive sanctions; and the EU’s attempt to maintain unity over Ukraine while phasing out Russian fossil fuels by the late 2020s. (Reuters) The quantitative indicators that are already visible—record Russian gas volumes to Hungary in 2025, sustained Druzhba pipeline flows despite repeated disruptions, and continued investment momentum at Paks—suggest that, for now, the balance of material gains favours both Budapest and Moscow more than it does Brussels’ decoupling agenda. (Reuters) However, the mounting risks associated with transit vulnerability, legal and financial exposure to evolving sanctions, and technological lock-in to Russian nuclear designs indicate that the price of this bilateral cooperation may rise over time, potentially forcing a recalibration of Hungary’s strategy if the external environment continues to harden.

CHAPTER INDEX

Core Concepts in Review: What We Know and Why It Matters

- Structural Energy Dependence: Hungary’s Hydrocarbon and Power Mix in a Post-2022 Europe

- Gas Contracts, TurkStream, and the Druzhba Exemption: Legal and Physical Infrastructures of Reliance

- Nuclear Entanglement: Paks I, Paks II, and Competing U.S.–Russian Technology and Fuel Frameworks

- Trade, Pharmaceuticals, and Industrial Alliances: Sectoral Interdependence Beyond Energy

- Budapest in Brussels and Brussels in Budapest: Hungary’s Russia Policy Inside EU and NATO Decision-Making

- Moscow’s Strategic Calculus: Using Hungary to Navigate Sanctions, War Diplomacy, and Eurasian Connectivity

- TABLE OF ARGUMENTS / CONCEPTS

Core Concepts in Review: What We Know and Why It Matters

At the heart of the recent saga involving Hungary, the European Union, and Russia lies a core set of interlocking realities — infrastructural, contractual, geopolitical — that together shape not only whether Budapest continues to import Russian energy, but also whether Moscow will retain leverage over portions of Europe. Understanding these core concepts is essential to assessing the strategic, economic, and political stakes of the current transition.

First: energy dependence is not just about volumes shipped, but about locked-in contracts and pipeline geography. Hungary’s continuation of Russian gas and oil imports stems from long-term arrangements — in particular, a 15-year gas supply contract with Russian supplier Gazprom Export, signed in 2021, which commits Hungary to receive roughly 4.5 billion cubic metres per year via the TurkStream pipeline and related Balkan transit routes. (Reuters) Because the pipeline infrastructure already exists and delivers under legally binding contracts, switching away from Russian gas is not a matter of toggling a new supplier — it requires reconfiguring supply chains, renegotiating or breaking contracts, and building or scaling alternative import routes.

Second: the timing of legal and regulatory shifts at the EU level now collides with that structural dependence. In October 2025, the energy ministers of EU member states agreed in principle to a plan to end Russian oil and gas imports by January 1, 2028, with bans on new contracts as early as January 2026, and on short-term contracts by mid-2026. (Reuters) That plan reflects the bloc’s desire to cut off a major source of revenue to Russia and reduce strategic vulnerability, but it also imposes a hard deadline on countries like Hungary — countries for which Russian imports remain a core part of the energy mix.

Third: this tension between long-term dependence and regulatory pressure creates a zone of strategic friction inside the EU. Hungary has already resisted EU proposals to phase out Russian energy imports, arguing that its economy and energy security depend on maintaining access to pipeline supplies. (Reuters) The result is a situation in which certain member states may comply with the phase-out, while others — because of geography, contracts, or political choice — resist, undermining solidarity and complicating the uniform implementation of EU energy policy.

Fourth: incremental diversification efforts — such as Hungary’s recent deal with French company Engie to buy 400 million cubic metres per year of gas from 2028 onward — do not materially alter the dependency equation. (Reuters) Given that Hungary’s domestic demand remains near 8 billion cubic metres per year, this new supply would cover at most 5 %–6 % of consumption. That suggests such diversification is more symbolic or hedging than structural — providing marginal alternative capacity, but not displacing Russian pipeline gas as the backbone of supply.

Fifth: the political economy of energy in Hungary — and in pipeline-dependent states more broadly — reflects what one might call the “path-dependence trap.” Once infrastructure is built and large investments made, and once domestic industries, utilities, and social policies (e.g., regulated energy prices, low tariffs, domestic manufacturing reliant on stable energy) are calibrated to continuous Russian supply, the cost of reversal skyrockets. Regulatory bans or contract cancellations are not cost-free — they may result in supply disruptions, legal disputes, higher prices, consumer hardship, industrial slowdowns. In this sense, infrastructure and contracts themselves become political and economic barriers to decoupling.

Sixth: for Russia, these pipelines and long-term deals represent far more than export routes — they are strategic levers. By anchoring parts of Central Eastern Europe (Hungary, Slovakia, others) to its energy supply, Moscow preserves revenue streams, retains influence inside the EU, and mitigates the effects of broader sanctions and decoupling efforts. As analysts argue, pipelines such as TurkStream — and countries willing to maintain imports — create “asymmetric leverage,” whereby Russia’s losses from declining export volumes are cushioned even as the rest of Europe moves away. (Reuters)

Seventh: the current window — from 2025 through 2028 — is a critical geopolitical inflection point. The EU’s formal phase-out timetable establishes a clear deadline for decoupling. For Hungary, that raises existential strategic choices: comply and rewire supply, negotiate carve-outs or transitional mechanisms, resist and confront EU law, or secure external exemptions. Already, Budapest has indicated willingness to challenge parts of the EU’s energy-transition proposal in court and to demand special treatment. (euronews)

Eighth: the stakes go beyond energy prices or fuel imports. The intertwining of energy strategy, infrastructure, industrial policy, and geopolitical alignment means that these choices affect national sovereignty, foreign-policy direction, alliances, and even internal governance models. Countries that decouple swiftly may face short-term pain but gain strategic leverage and alignment with EU and Western security architecture. Countries that resist risk institutional friction, internal economic strain, and potentially — if sanctions regimes tighten — legal or diplomatic consequences.

Ninth: the “dual-track” model of partial decoupling plus hedging — small diversification deals, contractual extensions, regulatory resistance — may succeed in stretching out the timeline, but at increasing cost and risk. As sanctions deepen and alternative suppliers and infrastructure scale up elsewhere in Europe, pipeline-dependent countries may find themselves ever more isolated, or forced to pay premiums for risk — whether insurance, financing, or political concessions.

Finally: the current moment underscores a broader strategic lesson for policymakers and legislators: energy security is deeply political, not just technical or economic. Pipelines, contracts, and supply sources are geopolitical assets. The countries that control them — and the companies that manage them — wield influence. Changing them is disruptive. Any transition away from a dominant supplier requires carefully calibrated policy, infrastructure investment, legal adaptation, and — crucially — regional coordination.

For a new policymaker, newly elected member of a legislature, or for a policy-major preparing recommendations, the question is not simply “should we cut off Russian energy?” but “how do we manage a transition whose cost, risk, and timeline depend on more than energy — on infrastructure, industrial dependencies, geopolitical dynamics, and socio-economic trade-offs.” The Hungarian case shows that even well-intentioned regulatory initiatives, if imposed without realistic transitional planning, risk provoking economic disruption, political backlash, or strategic fragmentation.

Understanding these core concepts — contract lock-in, infrastructural path-dependence, geopolitical leverage, regulatory timelines, and dual-track hedging — is therefore essential if Europe is to move toward energy security and political coherence without destabilising individual member states or inadvertently reinforcing the very dependencies it aims to dismantle.

image : The new TurkStream pipeline – copyright debuglies.com

Structural Energy Dependence: Hungary’s Hydrocarbon and Power Mix in a Post-2022 Europe

The transformation of the European Union energy system after 2022 has been defined by deliberate disengagement from Russian fossil fuels, yet Hungary has maintained and even deepened a pattern of reliance that predates the war in Ukraine. At EU level, official assessments of the REPowerEU agenda record a sharp contraction in Russian gas’s share of EU imports from about 45 % in 2021 to 19 % in 2024, with projections indicating a further fall to around 13 % in 2025, while Russian crude oil’s share in EU imports has dropped to below 3 %. (Energy) These aggregate figures obscure a strong divergence among member states: the bulk of the post-2022 adjustment has been borne by western and northern members through a rapid expansion of non-Russian pipeline and liquefied natural gas supplies, while landlocked Central European states continue to receive Russian pipeline gas and crude. Among them, Hungary stands out because its leadership has politically committed to preserving Russian energy flows even as the European Commission and Council advance legislation that would terminate all Russian gas contracts by the end of 2027 and phase out fossil fuel imports from Russia entirely by the late 2020s. (AP News)

The structural character of Hungary’s dependence emerges clearly from international energy statistics. According to the International Energy Agency, oil products accounted for about 39 % of Hungary’s total final energy consumption in 2023, making liquid fuels the single largest component of end-use energy. (IEA) Natural gas represented an additional 27 % of total final consumption in the same year, while the share of natural gas in total energy supply reached roughly 29.5 % in 2024, underscoring the centrality of gas both in power and heat supply. (IEA) The IEA country profile further indicates that more than four-fifths of overall primary energy in Hungary continues to come from fossil fuels, with coal playing a declining but still significant role and renewables—dominated by bioenergy and rapidly expanding solar generation—taking a minority share. (IEA) In other words, the energy system into which post-2022 shocks have been injected remains structurally fossil-fuel-intensive, with liquid fuels and gas together making up roughly two-thirds of consumption and almost all of that supply imported.

Within this aggregate fossil dependence, the gas sector has become the most politically sensitive vector of Russian influence. The IEA reports that domestic gas production in Hungary has been in long-term decline, leaving imports to cover the bulk of demand, which stabilised at around 8–9 billion cubic metres per year in the early 2020s following a peak near 15 billion cubic metres in 2005. (IEA) The long-term contract signed in September 2021 between state-owned wholesaler MVM CEEnergy and Gazprom Export binds Hungary to Russian gas for up to 15 years, with annual deliveries of as much as 4.5 billion cubic metres, predominantly routed via the TurkStream system and associated pipelines through the Western Balkans rather than through Ukraine. (OSW Ośrodek Studiów Wschodnich) The design of this contract, as described in official company presentations and government statements, explicitly sought to secure low-cost baseload volumes with renegotiation options after 10 years, reflecting a pre-war assumption that Russian pipeline gas would remain the cheapest and most predictable supply source for Central Europe. (OSW Ośrodek Studiów Wschodnich)

The shocks of 2022–2024 did not fundamentally alter this contract architecture. Instead, Hungary opted to layer diversification measures on top of, rather than in place of, the Russian supply pillar. In October 2025, the government announced what it described as its largest liquefied natural gas deal to date: a long-term contract under which MVM CEEnergy will purchase 400 million cubic metres per year from Engie between 2028 and 2038, equivalent to roughly 5 % of current annual gas consumption, complemented by an earlier agreement with Shell for 200 million cubic metres per year starting in 2026. (Reuters) Official statements emphasised that these arrangements were intended to strengthen energy security and bargaining power rather than to replace “stable” Russian pipeline supplies, and Reuters reporting on the same deals highlighted that by August 2025 Hungary had already imported around 5 billion cubic metres of Russian gas via TurkStream in that year alone, a record volume for the route. (Reuters) The net effect is an energy system in which diversification modestly broadens the supply portfolio but leaves Russian pipeline gas as the dominant marginal source and as the anchor of pricing arrangements for households and industry.

This gas-based dependence is reinforced by the structure of end-use demand. Eurostat and IEA data show that the residential and commercial sectors, which rely heavily on gas for space heating and hot water, account for a large share of Hungary’s final gas consumption, while industry uses gas both as a fuel and as a feedstock in chemicals and fertilisers. (European Commission) The legacy of extensive gasification of district heating and building stock during the socialist period, combined with post-1990 price subsidies and regulated tariffs, has created social and political expectations of plentiful, affordable gas that successive governments have been reluctant to challenge. The long-term contract with Gazprom thus operates as both a commercial and a social-policy instrument: it underpins the “utility price cut” agenda, through which the government caps household energy prices, and it sustains energy-intensive manufacturing that is geographically concentrated in politically influential constituencies. (balkaninsight.com)

Oil dependence is structurally different but strategically intertwined. On the demand side, transport sector statistics confirm that road transport is responsible for about 62 % of oil product use in Hungary, with diesel and gasoline powering freight and passenger mobility, while industry and other sectors consume the remainder. (IEA) On the supply side, IEA data note that Hungary refines more crude oil than it consumes in oil products on a net basis, with domestic refining accounting for about 103 % of final oil product consumption in 2023–2024, implying that refineries serve both domestic and export markets. (IEA) The crude feeding this refining system arrives primarily by pipeline, and since the EU embargo on seaborne Russian crude and petroleum products entered into force in December 2022, the southern branch of the Druzhba pipeline—linking Russian fields to refineries in Hungary and Slovakia—has become the last remaining sanctioned-exempt route for Russian oil into the EU. (Parlamento Europeo)

The exemptions granted to Hungary and Slovakia mean that Russian crude continues to be delivered to the MOL group’s refineries, even as overall EU imports of Russian oil have fallen sharply. The European Parliamentary Research Service notes that the Russian share of EU crude oil imports declined from 27 % in 2021 to around 3 % by 2024–2025, a change driven primarily by seaborne import bans and re-routing of tanker flows. (Parlamento Europeo) Because pipeline flows to Hungary and Slovakia have no defined end date in the current sanctions regime, analytical work on EU–Russia oil trade stresses that Druzhba now functions as a residual but politically sensitive artery for Russian exports to Europe. (kpler.com) In practical terms, this institutional carve-out allows Hungary to secure crude at prices that have at times been significantly discounted relative to global benchmarks, supporting refinery margins and domestic fuel price controls, but it also locks the country into a vulnerable infrastructure corridor running through a war zone.

That vulnerability has become increasingly evident through repeated disruptions since 2022. Reporting on August 2025 interruptions indicates that Ukrainian attacks on Russian energy infrastructure temporarily halted Druzhba flows, forcing MOL to rely on refinery and strategic reserves while exploring increased imports via the Adriatic pipeline from Croatia. (Reuters) The company’s leadership has publicly acknowledged that, although the Adriatic route can compensate for some shortfalls, pipeline capacity constraints mean that it would be difficult to run both MOL refineries at full load solely on non-Russian, non-Druzhba crude. (Reuters) As a result, Hungary’s oil supply chain is structurally exposed to both kinetic risks in Ukraine and to regulatory risks in Brussels, where proposals to phase out Druzhba exemptions by 2027–2028 are gaining momentum alongside broader regulations to end Russian fossil fuel imports. (AP News)

Electricity generation constitutes the third pillar of Hungary’s energy system and displays a different but related pattern of structural dependence, centred on nuclear rather than hydrocarbons. The World Nuclear Association’s December 2024 country profile for Hungary reports that the four reactors at the Paks Nuclear Power Plant, with combined net capacity of 1,916 megawatts electric, generate “about half” of national electricity output. (world-nuclear.org) A recent International Atomic Energy Agency mission to the Hungarian Atomic Energy Authority in October 2025 similarly notes that Hungary produces roughly half of its electricity at Paks and is planning to construct two additional units at the same site. (world-nuclear-news.org) This dominance of nuclear in generation is reflected in the broader power mix: while the IEA estimates that renewables—including a rapidly expanding fleet of solar photovoltaic installations—reached a share of about 20.2 % of power generation in 2024, nuclear remains the single largest low-carbon source, displacing what would otherwise be substantial gas- or coal-fired output. (IEA)

The strategic dependence arises from the technology and finance underpinning both existing and planned capacity. The original VVER-440 units at Paks are Soviet-designed, and their fuel supply and many major components have historically been sourced from Russian entities. The planned Paks II expansion, contracted in 2014 between the Hungarian government and Russian state company Rosatom, will deploy two VVER-1200 reactors of about 1,200 megawatts each and is backed by a Russian state loan facility widely reported in official and semi-official sources as amounting to up to €10 billion of a total project cost exceeding €12.5 billion. (Parlamento Europeo) While construction has faced delays due to regulatory scrutiny and the evolving sanctions environment, recent Reuters coverage of United States sanctions licences and nuclear cooperation agreements with Hungary confirms that both Paks I and Paks II remain central to government planning for long-term electricity supply. (Reuters)

At the same time, Hungary has begun to reduce the most acute aspects of fuel-supply dependence by diversifying nuclear fuel vendors. Official statements and Reuters reporting in November 2025 explain that a bilateral nuclear cooperation agreement with the United States enables American companies to supply fuel for Paks I and provide technology for spent fuel storage, with the U.S. Treasury issuing a general licence that allows transactions related to Paks II to proceed without violating Russia-related financial sanctions. (Reuters) From a structural perspective, this creates a dual-dependence environment: reactor technology, construction and much of the engineering base remain tied to Russian designs and contractors, while fuel supply gradually becomes contestable between Russian and Western vendors. In energy-security terms, this reduces the risk of an abrupt, politically motivated fuel cut-off but preserves long-term technical lock-in to Russian nuclear standards, complicating any future decision to pivot away from Russian involvement altogether.

These three pillars—gas, oil and nuclear—are embedded within a broader macro-energy trajectory that underscores Hungary’s vulnerability to both external shocks and internal policy choices. A 2024 systems-modelling study of Hungarian energy transition pathways, published in a peer-reviewed engineering journal, estimates that total final energy demand will stabilise near 210 terawatt-hours by 2050, but that the current roughly 65 % fossil fuel share of supply, much of it imported, leaves the country exposed to price volatility and supply interruptions. (cetjournal.it) The same study argues that without accelerated deployment of renewables and efficiency measures, Hungary will struggle to meet EU climate targets while simultaneously managing the security and affordability dimensions of energy policy. The post-2022 shift in EU-level regulation—especially the REPowerEU target to end Russian fossil fuel imports and the proposed bans on new Russian gas contracts—directly intersect with this structural challenge, because they constrain the set of feasible long-term supply configurations for a system that was built around Russian hydrocarbon and nuclear inputs. (Energy)

From the standpoint of dependence, two ratios are particularly revealing: import dependency and concentration of suppliers. Eurostat’s energy balance databases show that Hungary’s import dependency for natural gas and oil is close to 100 %, with negligible domestic production relative to consumption, while overall energy import dependency exceeds 50 %. (European Commission) The concentration dimension is more opaque because Eurostat’s public data on the geographical origin of imports are more detailed at EU aggregate level than at member-state level, but multiple official and semi-official sources concur that Russia remains the dominant external supplier for both gas and crude. European Commission and European Parliament analyses on phasing out Russian fossil fuels repeatedly single out Hungary as a key beneficiary of the remaining Druzhba exemption and of continued Russian pipeline gas deliveries, while independent economic research notes that the share of gas in Hungary’s gross inland energy consumption was among the highest in the EU in the mid-2000s, and although it has fallen since then, it remains structurally significant. (Parlamento Europeo) In statistical terms, this combination of high import dependency and supplier concentration implies that Hungary’s energy security is highly sensitive to changes in Russian export policy, to disruptions in single transit routes, and to the evolving architecture of EU sanctions and energy regulation.

The post-2022 EU policy response has aimed precisely at reducing such vulnerabilities at the bloc level, but in doing so it has accentuated divergences between states that have rapidly diversified and those, like Hungary, that have not. The Quarterly Report on European Gas Markets for Q4 2024, published by the European Commission, notes that total EU gas consumption in 2024 was around 332 billion cubic metres, roughly 20 % below 2021 levels, with the share of Russian pipeline gas falling sharply and Norwegian, North African and LNG supplies—especially from the United States—filling the gap. (Energy) At the same time, supplementary analyses by think-tanks and financial institutions highlight that physical Russian gas deliveries to a small group of member states, notably Hungary, Slovakia and Austria, have persisted or even increased, particularly via TurkStream and its onshore extensions. (wiiw.ac.at) From Brussels’ perspective, this concentrates residual Russian leverage in a narrow sub-set of the EU, while from Budapest’s perspective it offers an opportunity to position the country as a regional hub for Russian gas, with transit and storage infrastructure potentially generating rents. (balkaninsight.com)

The same divergence is now visible in oil policy. The European Commission and Council are advancing legal proposals that would use trade law and internal-market competences to ban new Russian gas contracts and to phase out existing ones by 2027–2028, coupled with a broader regulatory framework to end imports of Russian fossil fuels. (AP News) Hungary has responded by announcing its intention to challenge these measures before the European Court of Justice, arguing that they circumvent national veto powers on sanctions and violate EU treaties. (AP News) In substantive terms, this legal dispute is an extension of underlying structural tensions: compliance with a hard 2027–2028 timeline would require Hungary to replace nearly all Russian gas and crude imports within a few years, a task that would involve large-scale infrastructure investments, renegotiation of long-term contracts, and potentially substantial price increases for consumers. By contrast, the status quo allows Hungary to continue profiting from discounted Russian supplies and from the refining margins associated with processing Russian crude that cannot be sold elsewhere in the EU.

Finally, structural dependence must be understood not only in supply-side and legal terms but also in the configuration of domestic economic interests. The IEA country statistics on sectoral energy consumption show that transport, industry and residential users together account for the overwhelming majority of fossil energy demand in Hungary, with energy-intensive manufacturing, automotive production and chemicals forming key export sectors. (IEA) The profitability and international competitiveness of these sectors are sensitive to energy price differentials within the EU, and access to relatively cheap Russian gas and oil has functioned as a comparative advantage. At the same time, the nuclear-dominated power mix, underpinned by Paks and future Paks II capacity, provides relatively stable wholesale electricity prices and a low-carbon narrative that can be deployed in EU climate policy debates. (world-nuclear.org) The result is an intricate web of structural incentives that align significant segments of Hungary’s political economy with the preservation of energy ties to Russia, even as the wider EU seeks to exit that relationship.

In sum, post-2022 Hungary finds itself operating an energy system in which hydrocarbons still dominate final consumption, nuclear power anchors electricity generation, and import dependency on a single external supplier—Russia—remains pronounced across gas, oil and key nuclear inputs. The EU-wide drive to phase out Russian fossil fuels and to reduce exposure to Russian nuclear technology is reshaping the strategic environment, but the underlying physical and contractual structures of Hungary’s hydrocarbon and power mix continue to reflect choices made over decades in which Russian energy was treated as abundant, reliable and apolitical. The tensions between those inherited structures and the new regulatory and geopolitical landscape form the backdrop against which Budapest now negotiates both with Moscow and with Brussels, and they condition the range of feasible options for any reorientation of the country’s energy policy in the years leading up to 2027–2028. (Energy)

Gas Contracts, TurkStream and the Druzhba Exemption: Legal and Physical Infrastructures of Reliance

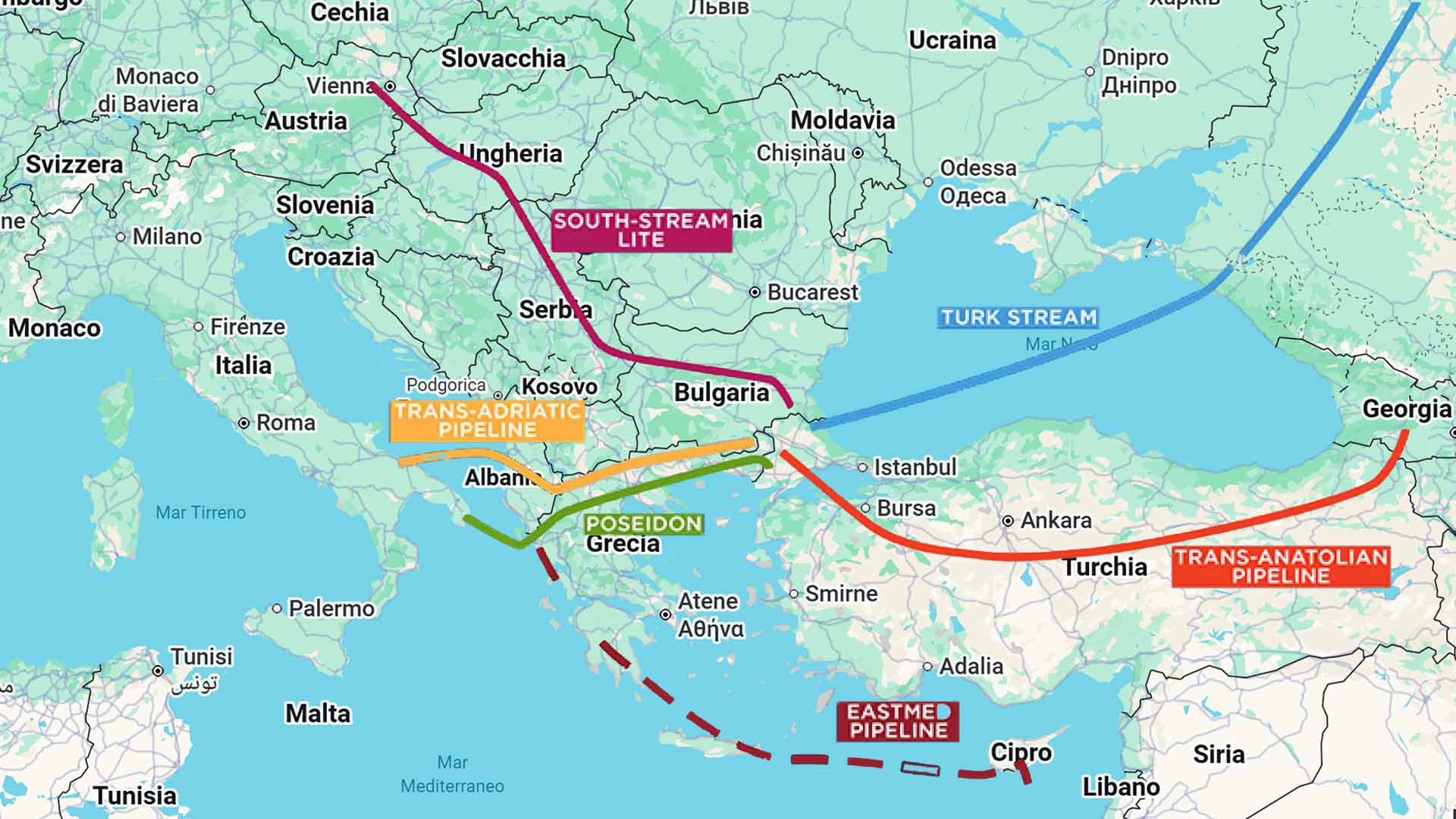

The long-term gas contract that Hungary concluded with Gazprom Export in September 2021 forms the backbone of its present-day dependence on Russian gas and illustrates how commercial arrangements, transit infrastructure and European Union law have become tightly interwoven. On 27 September 2021, MVM CEEnergy and Gazprom Export signed two interlinked agreements in Budapest, under which Hungary is entitled to receive up to 4.5 billion cubic metres of gas annually for 15 years, with an option to renegotiate volumes after 10 years. (OSW Ośrodek Studiów Wschodnich) The deal, as described in contemporaneous official and analytical reports, redirected Hungary’s contractual supply away from the traditional Ukraine transit route and into a new configuration in which about 3.5 billion cubic metres per year are delivered via TurkStream and onshore pipelines through Bulgaria and Serbia, while the remaining 1 billion cubic metres arrive from Austria. (Anadolu Ajansı) The explicit objective was to lock in predictable volumes at a price formula benchmarked to regional hubs, while embedding the Russian supply relationship in a legal framework that would outlast short-term market fluctuations and, at the time of signing, any foreseeable political tensions.

This contractual pivot toward TurkStream rests on a physical system that had been under construction since the late 2010s as a replacement for earlier projects, most notably South Stream, that had run afoul of EU internal-market rules. In technical terms, the offshore section of TurkStream consists of two parallel pipelines laid across the Black Sea seabed between Russia and Turkey, with a combined capacity of 31.5 billion cubic metres per year, or 15.75 billion cubic metres per line. (congress.gov) One line supplies the Turkish domestic market, while the second continues into south-eastern Europe via onshore pipes running from Kıyıköy in Turkey through Bulgaria and Serbia toward the Hungarian border. (congress.gov) Policy analysis from European think-tanks underlines that this corridor allows Gazprom to reach Central European customers while minimising reliance on Ukraine as a transit state, thereby reducing legal and geopolitical exposure to disputes similar to those that disrupted supplies in 2006 and 2009. (Bruegel) For Hungary, connecting to this southern route through interconnectors with Serbia and Bulgaria offered both diversification away from a single transit corridor and an opportunity to position itself as a potential hub for Russian gas entering the EU from the south. (balkaninsight.com)

The way this infrastructure has been used since 2022 reveals how contractual and physical arrangements have interacted with sanctions and war. Data reported by Hungarian officials and summarised in international coverage indicate that by the end of August 2025, Hungary had already imported around 5 billion cubic metres of Russian gas via TurkStream, putting the country on track for a record annual volume through this route despite significant reductions in Russian flows to the rest of the EU. (Reuters) This occurred at a time when the European Commission’s own gas-market reports were recording a sharp fall in Russian gas’s share of aggregate EU supply—from around 45 % in 2021 to roughly 19 % in 2024, with projections toward 13 % in 2025, and when Russian pipeline deliveries to western and northern member states had dwindled. (Parlamento Europeo) The persistence and even increase of flows to Hungary and a small cluster of Central European states is therefore not the residue of old habits but the result of deliberate contractual choices made shortly before the invasion and subsequently defended in the face of mounting political pressure.

Parallel to the consolidation of TurkStream as the main gas corridor, Hungary and Russia have preserved a second, older artery for energy flows in the form of the southern branch of the Druzhba oil pipeline. Originally constructed in the 1960s, Druzhba—literally “Friendship”—runs from Almetyevsk in Tatarstan across Russia and branches through Belarus and Ukraine, delivering crude oil to refineries in Poland, Germany, Czechia, Slovakia and Hungary. (Global Energy Monitor) The southern branch is of particular importance for Hungary: after crossing Ukraine, the line splits near Uzhhorod into one segment that continues to Slovakia and Czechia and another that feeds directly into Hungary, supplying MOL’s Duna refinery near Százhalombatta and, via an internal network, the Tisza refinery as well. (IAOT) Estimates compiled by infrastructure monitors assign the overall system a capacity in the range of 1.2–1.4 million barrels per day, with potential expansion to 2 million barrels per day, underscoring that Druzhba remains one of the largest crude export pipelines in the world. (IAOT) For landlocked Hungary, this infrastructure has historically served as the primary route for crude imports, structuring refinery configurations and product flows in ways that are not easily reversed.

The legal environment governing Druzhba changed dramatically with the EU’s sixth sanctions package against Russia, adopted in June 2022 in response to the full-scale invasion of Ukraine. The package introduced bans on seaborne imports of Russian crude oil and oil products but deliberately exempted pipeline deliveries to member states with particular pipeline dependence, allowing them to continue receiving crude via Druzhba beyond the entry into force of the embargo in December 2022 for crude and February 2023 for refined products. (Servizio Europeo per l’azione esterna) Parliamentary and Commission documents explicitly reference Hungary, Slovakia and Czechia as beneficiaries of this temporary exemption, justified on the grounds that these landlocked countries lack immediate alternative supply routes of sufficient capacity to fully replace pipeline crude. (Parlamento Europeo) In practice, the absence of a fixed end date for the exemption and the difficulty of rapidly upgrading alternative infrastructure, such as the Adriatic pipeline from Croatia, transformed a nominally temporary derogation into a semi-permanent structural carve-out that preserved a distinct enclave of Russian oil trade within the wider EU sanctions regime.

Hungarian political leaders have treated this carve-out not as an unwelcome transitional necessity but as a strategic asset. Statements and diplomatic manoeuvres in Brussels emphasise that Budapest regards the Druzhba exemption as integral to its energy security and has repeatedly signalled a willingness to veto or legally challenge any move to terminate it unilaterally. (CE Energy News) At the same time, infrastructural planning indicates that Hungary is not content merely to preserve existing pipeline flows but seeks to expand its role as a conduit for Russian crude to neighbouring states that face tighter constraints. A Memorandum of Understanding signed in June 2023 between Hungary and Serbia sets out plans to construct a new oil pipeline along the route Százhalombatta–Algyő–Röske–Novi Sad, with a total length of around 304 kilometres and potential extension to the Serbian refinery town of Pančevo. (mre.gov.rs) The new line is projected to carry between 4–5 million tonnes of crude per year and to become operational by 2027, coinciding with the timeline under which other EU members are expected to have phased out Russian oil imports altogether. (Anadolu Ajansı)

By building a dedicated connection between Druzhba and Serbia, Hungary positions itself as an intermediary capable of channeling Russian crude to a non-EU neighbour whose traditional supply route via Croatia’s JANAF pipeline has come under pressure from sanctions. Reuters reporting on U.S. measures targeting Serbia’s NIS refinery and subsequent Croatian decisions to halt shipments notes that MOL is preparing to increase deliveries to Serbia and that the new pipeline could fully cover Serbia’s crude needs by 2028. (Reuters) Analytical commentary in specialised outlets observes that this would effectively render Serbia dependent on Russian oil routed through EU territory under Hungarian control, at a time when most other member states have severed such links. (Anadolu Ajansı) The combination of the Druzhba exemption and the new pipeline thus generates a layered infrastructure of reliance in which Hungary is both a dependent consumer of Russian crude and a regional distributor with leverage over a neighbouring state’s supplies.

Legal proposals tabled by the European Commission since mid-2025 seek to unwind this architecture by using internal-market and trade-law instruments to make the phasing-out of Russian gas and oil imports legally binding and resistant to individual vetoes. On 16–17 June 2025, the Commission presented a package that would, if adopted, prohibit EU gas imports under new contracts with Russian suppliers as of 1 January 2026, terminate imports under existing short-term contracts by the end of 2025, and require the phase-out of long-term contracts by 1 January 2028. (European Commission) The same package outlines an intention to end imports of Russian liquefied natural gas and to progressively close remaining loopholes in the oil regime, including revisiting pipeline exemptions. (European Commission) The legislative technique is significant: by framing the measures as trade restrictions under Article 207 TFEU and as energy-security measures within the internal market, the Commission aims to adopt them through qualified majority voting rather than unanimity, thereby reducing the ability of individual states, above all Hungary, to block their adoption. (eur-lex.europa.eu)

Hungary’s response has been to contest both the substance and the procedure of these proposals. Public statements by Budapest officials indicate that the government regards a mandatory 2027–2028 deadline for ending Russian gas imports as incompatible with national energy-security needs and with the long-term gas contract concluded in 2021, and it has threatened to challenge the Commission’s approach before the Court of Justice of the European Union. (CE Energy News) At the same time, Hungary continues to sign new diversification deals that are carefully framed as adjuncts rather than alternatives to Russian supplies. The October 2025 agreement under which MVM CEEnergy will purchase 400 million cubic metres of liquefied gas per year from Engie between 2028–2038, alongside a separate contract with Shell for 200 million cubic metres per year starting in 2026, is officially presented not as a step toward ending Russian imports but as a way to strengthen negotiating power and to ensure that competitive alternatives exist. (Reuters) In practice, given that Hungary’s total annual gas consumption hovers around 8 billion cubic metres, these contracts together cover only about 7–8 % of demand, leaving the bulk of supply to be met by existing pipeline arrangements. (Reuters)

The legal tension between EU-level decoupling and national-level contractual commitments is compounded by the complexity of the physical system through which gas and oil move. The Agency for the Cooperation of Energy Regulators notes in its 2024 gas-market monitoring reports that Hungary is connected to multiple neighbouring markets via interconnectors with Austria, Slovakia, Romania and Serbia, and that the regional gas market has become increasingly integrated since 2021 as new capacity and reverse-flow capabilities have come online. (acer.europa.eu) From a purely infrastructural perspective, this means that non-Russian gas delivered to LNG terminals in the Adriatic or Aegean and to Central European hubs could, in principle, reach Hungary in significant volumes, especially if market signals favour such flows. However, long-term contracts, regulated domestic prices and political preferences have so far constrained the extent to which these physical options are used to displace Russian imports. (balkaninsight.com)

Similar dynamics apply to oil infrastructure. The European Parliament’s briefing on EU energy infrastructure emphasises that, while pipeline oil was exempted from the 2022 embargo to protect landlocked countries, most member states have since found alternative crude suppliers by increasing reliance on seaborne imports and building new logistical chains. (Parlamento Europeo) For Hungary, access to the Adriatic pipeline via Croatia theoretically provides an alternative to Druzhba, but capacity constraints and the need for refinery adaptations limit how quickly this option can fully substitute for Russian crude. (Parlamento Europeo) The planned Hungary–Serbia oil pipeline, instead of reducing dependence on Russian oil, deepens the role of Russian crude in regional supply by creating a new route for Urals-grade oil at precisely the moment when other EU members are phasing it out. (Anadolu Ajansı)

From a strategic standpoint, the combined effect of the 2021 gas contracts, the TurkStream and Druzhba corridors, and the legal exemptions and proposals that surround them is to create what might be described as an infrastructure of asymmetric resilience. For Russia, the existence of alternative southern routes and of pipeline-dependent customers inside the EU cushions the impact of EU-wide decoupling and preserves a degree of political leverage. For Hungary, the same system provides short-term price and supply advantages, but at the cost of growing entanglement in a legal and infrastructural configuration that is increasingly out of step with EU policy trajectories. (Parlamento Europeo) The more the EU embeds a 2027–2028 cut-off for Russian gas and oil into binding law, the more the long-term gas contract and pipeline investments risk turning from assets into potential liabilities, raising questions about stranded infrastructure, compensation for contract terminations and the allocation of costs between national budgets, EU funds and private companies. (eur-lex.europa.eu)

The legal-physical nexus around TurkStream and Druzhba thus constitutes far more than a set of tubes in the ground. It encodes a particular vision of regional energy order—one in which Hungary acts as a loyal client and partial intermediary for Russian hydrocarbons inside the EU—and sets that vision against an emerging EU legal order that seeks to close the chapter on Russian fossil fuels altogether by the end of the decade. The confrontation between these two logics is now being waged simultaneously in Commission drafting rooms, in Council negotiations, in courtrooms and in the highly material realm of compressor stations, pumping units and metering stations that can be shut down by drones or cyberattacks. (Reuters) How that confrontation is resolved will determine whether the infrastructures that today sustain Hungary’s reliance on Russian gas and oil become bridges to a managed transition or monuments to a strategic bet that ran against the direction of the wider European energy and security system.

Nuclear Entanglement: Paks I, Paks II and Competing U.S.–Russian Technology and Fuel Frameworks

Nuclear power in Hungary is anchored in a single site whose technical configuration, regulatory environment and financing arrangements collectively illustrate how deeply the country’s energy system is enmeshed with Russian technology while increasingly incorporating Western oversight and fuel alternatives. The four units of the Paks nuclear power plant, built on Soviet VVER-440 designs, have operated since the 1980s as the backbone of the national power system, and international reference data compiled by the International Atomic Energy Agency in its 2024 edition of the reference series “Nuclear Power Reactors in the World” confirm that these reactors form a compact site with total net capacity in the two-gigawatt range, classed as VVER-440/V-213 pressurised water reactors. (www-pub.iaea.org) Supplementary reporting by the Hungarian Atomic Energy Authority, including its 2024 newsletter on recent developments in nuclear safety, underscores that Paks remains the country’s only commercial nuclear station and is treated in regulatory planning as an essential “base-load” asset for the coming decades. (haea.gov.hu)

From the standpoint of system operation, these four units supply roughly half of Hungary’s domestically generated electricity, with the remainder covered by fossil-fired plants and an expanding solar fleet, while the country continues to import a significant share of its total consumption from neighbouring systems. This profile is reflected in international energy statistics compiled by the International Energy Agency, which report that nuclear power’s contribution to total generation has hovered around the mid-40s to low-50 % range in recent years. (Wikipedia) The centrality of Paks to grid stability is accentuated by the plant’s high capacity factors and by the fact that nuclear output is largely insensitive to short-term fuel price fluctuations, in contrast to gas- or coal-fired generation. As a result, the site functions not only as a low-carbon generator but also as an implicit hedge against the volatility of imported fossil fuel prices, a role that gained additional strategic importance after 2022 when gas and electricity prices across Europe spiked in response to cuts in Russian pipeline deliveries.

The life-extension strategy for Paks shows how a legacy Soviet-designed facility has been progressively re-embedded in contemporary safety and licensing frameworks while still relying on Russian-origin technology. The original design lifetime of the VVER-440 units was about 30 years, which for reactors commissioned between the early 1980s and late 1980s would have implied shutdown dates in the 2010s. Hungarian authorities instead opted for systematic modernisation and life-extension, a choice that required comprehensive safety reviews and regulatory upgrades. The Hungarian Atomic Energy Authority’s public reporting describes how life-extension programmes, implemented from the mid-2000s onwards, were assessed against updated safety standards, with the regulator issuing operating licence extensions out to the 2030s for each unit. (haea.gov.hu) In parallel, progressive uprating and equipment replacement programmes have kept the units competitive in terms of output and availability, reinforcing their status as long-term pillars of the power system rather than residual assets approaching retirement.

Regulatory scrutiny of this extended operating life has intensified in recent years, reflecting both the age of the reactors and the broader post-Fukushima tightening of nuclear safety standards. In 2024, Hungary invited the International Atomic Energy Agency to conduct a follow-up Integrated Regulatory Review Service mission, assessing governmental, legal and institutional frameworks for nuclear and radiation safety. According to the IAEA press release summarising the October 2025 mission, the expert team reviewed oversight arrangements for nuclear power plants, research reactors, radiation sources and waste management facilities and concluded that Hungary demonstrates a strong commitment to nuclear and radiation safety, while recommending further enhancements in areas such as human resources and regulatory independence. The mission was requested by the government and hosted by the Hungarian Atomic Energy Authority, serving as a peer review of how national regulation aligns with international safety standards. (IAEA)

If Paks I represents the inherited core of Hungary’s nuclear sector, Paks II epitomises its new entanglement with Russian reactor exports, state financing and European Union law. In 2014, Hungary concluded an intergovernmental agreement with Russia under which Russian state corporation Rosatom would design and build two new VVER-1200 units at the Paks site, effectively doubling installed nuclear capacity. The project is referenced in multiple international documents, including the IAEA’s “Nuclear Technology Review 2024”, which notes that preparations for constructing two VVER V-527 reactors at Paks II are underway, and in EU-level legal and policy texts that treat the expansion as a major test case for state aid control and procurement rules in the nuclear sector. (IAEA)

The financing structure of Paks II involves substantial state participation and a Russian state loan, raising questions under EU competition law. By 2017, the European Commission had completed a multi-year investigation into whether the financial support Hungary planned to provide to the project constituted compatible state aid. In its Commission Decision (EU) 2017/2112 of 6 March 2017, the Commission found that the aid did meet the criteria for state aid under Article 107(1) TFEU but considered it compatible with the internal market under Article 107(3)(c), subject to conditions intended to limit distortions of competition, such as separating the new nuclear assets from existing generation activities and ensuring that any excess profits would accrue to the state. (EUR-Lex) The decision relied on the reasoning that nuclear power contributes to public objectives such as security of supply and climate mitigation, and that the particular structure of Paks II would not unduly crowd out private investment in other technologies.

This conclusion did not go unchallenged. Austria, a long-standing opponent of nuclear power, brought an action before the Court of Justice of the European Union seeking annulment of the Commission’s approval. The case, C-135/21 P, culminated in a judgment delivered in September 2025, in which the Court annulled the Commission’s decision on specific grounds related to public procurement. According to the Court’s summary in Press Release No. 116/25, the judges held that because the direct award of the construction contract to a Russian undertaking was inextricably linked to the object of the aid, the Commission should have examined whether that award complied with EU public procurement rules, and its failure to do so rendered the state aid decision unlawful. (Corte di giustizia europea) The ruling did not pronounce on the substantive merits of building Paks II but signalled that EU institutions must scrutinise closely how major nuclear projects select strategic suppliers, especially when contracts are granted without open tendering.

Despite this judicial setback, Hungary has reiterated its intention to proceed with Paks II, treating the Court’s judgment as a procedural issue to be addressed through further engagement with the European Commission rather than as a substantive veto. Public statements by government officials following the decision emphasise that preparatory works at the site are continuing under licenses issued by the Hungarian Atomic Energy Authority and that construction will go ahead once outstanding legal and technical questions are resolved. (neimagazine.com) This stance underscores how deeply nuclear expansion has been integrated into Hungary’s long-term energy strategy: the project is expected to provide large volumes of low-marginal-cost electricity well into the second half of the century, and its cancellation would leave a significant gap in the country’s planning for decarbonisation and security of supply.

The external environment for Russian nuclear exports has, however, changed markedly since 2014. European Union sanctions adopted in response to Russia’s actions in Ukraine have so far stopped short of imposing comprehensive restrictions on civil nuclear cooperation, but pressure has grown to address Rosatom’s role in the Russian state apparatus. A 2023 answer by the European Commission to a parliamentary question on sanctions against Rosatom, published as an official document on the European Parliament’s website, summarises existing measures targeting dual-use and high-technology exports that could contribute to Russian military capabilities and notes that some member states support expanding sanctions to cover the nuclear sector. (Parlamento Europeo) At the same time, the document acknowledges that several EU countries rely on Russian technology or fuel and that any such step would have to consider security-of-supply implications. In this context, Paks II sits at the intersection of competing imperatives: the desire to maintain a predictable, low-carbon baseload resource and the political objective of reducing dependence on Russian strategic industries.

The United States has emerged as a key actor in reshaping this balance through both sanctions design and bilateral nuclear cooperation with Hungary. Under Executive Order 14024, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) imposed wide-ranging restrictions on transactions with Russian financial institutions and entities, affecting, inter alia, the financing channels available for large infrastructure projects. Initially, these measures complicated payment flows linked to Paks II, as Russian banks involved in the project were placed under sanctions, and Hungary complained that this amounted to an extraterritorial attempt to halt a civil nuclear project. (Reuters) In November 2025, however, OFAC issued General License No. 132, explicitly titled “Authorizing Certain Transactions Involving Paks II Civil Nuclear Power Plant”, which authorises, under defined conditions, transactions otherwise prohibited under the Russian Harmful Foreign Activities Sanctions Regulations when they involve the Paks II project. (ofac.treasury.gov) The license text specifies that dealings with named Russian financial institutions and entities are permitted for the limited purpose of supporting the civil nuclear project, while excluding categories such as new debt of longer maturities or transactions with individuals listed on sanctions lists.

This general license operates alongside a separate, politically significant nuclear cooperation arrangement between Hungary and the United States that focuses on fuel supply and spent fuel management at Paks I. Statements by Hungarian officials and international reporting describe an agreement under which Hungary will purchase U.S. nuclear fuel and adopt American technology for the storage of spent fuel, marking the first time that Paks will be able to source fuel from a non-Russian supplier. (Reuters) This arrangement is part of a broader push, encouraged by EU institutions and G7 partners, to diversify nuclear fuel supplies away from Russian vendor TVEL, which has historically dominated the VVER fuel market in Europe.

Fuel diversification is also progressing through commercial contracts with private suppliers. In November 2025, Westinghouse Electric Company announced a “landmark nuclear fuel partnership” with MVM Group, the owner of Paks, under which Westinghouse will manufacture VVER-440 fuel assemblies in Europe and supply them to Paks from 2028, subject to licensing. The company’s official release, “Westinghouse and Hungary Establish Landmark Nuclear Fuel Partnership”, emphasises that this contract completes its portfolio of VVER-440 customers in Europe and Ukraine, signalling a structural shift in fuel markets long dominated by Russian designs. (Westinghouse Nuclear) Media and industry reports further indicate that Hungary has arrangements to source fuel from Framatome from 2027, creating a multi-vendor environment in which Paks I can be loaded with assemblies from different Western suppliers once regulatory approvals are secured. (World Nuclear News)

In technical terms, this move toward multi-sourcing is non-trivial. VVER-440 reactors are standardised designs, but fuel assemblies embody detailed specifications in geometry, materials, burnup characteristics and neutronic behaviour. Introducing a new fuel vendor into an operating reactor fleet requires extensive licensing, including verification that the new assemblies are compatible with reactor core physics, thermal-hydraulic margins, control systems and safety analysis assumptions. The IAEA’s publications on the management of spent fuel and on VVER decommissioning highlight how design choices in fuel and reactor systems propagate through the entire life-cycle, affecting storage, transport and disposal requirements. (www-pub.iaea.org) For Paks, switching from Russian-supplied TVEL fuel to Westinghouse or Framatome designs entails not just contractual changes but a re-engineering of fuel qualification, safety cases and waste management strategies, tasks that will occupy regulators and operators well into the 2030s.

The resulting configuration is a hybrid nuclear ecosystem in which Russian technology and Western fuel and finance co-exist under dense layers of EU, U.S. and international regulation. On the one hand, Rosatom remains the reactor vendor and principal contractor for Paks II, with its VVER-1200 design subject to domestic licensing by the Hungarian Atomic Energy Authority and peer scrutiny through IAEA mechanisms. The IAEA’s “Nuclear Technology Review 2024” lists Paks II among ongoing preparations for new VVER units, placing it within a broader portfolio of Russian nuclear export projects ranging from Türkiye’s Akkuyu plant to units in Bangladesh and Egypt. (IAEA) On the other hand, OFAC’s General License No. 132 and the bilateral cooperation agreement on fuel and waste storage integrate U.S. financial and technological interests into the same project, ensuring that Western suppliers and regulators have a stake in its evolution. (ofac.treasury.gov)

This hybridisation complicates governance. The Court of Justice of the European Union’s annulment of the original state aid approval means that any revised European Commission decision on Paks II will have to take into account not only the compatibility of financial support with EU competition rules and public procurement law, but also the changing landscape of fuel supply, sanctions and safety obligations. (Corte di giustizia europea) The Commission’s evolving approach to Russian energy dependence—visible in proposals to phase out Russian gas contracts and to reduce exposure to Russian nuclear fuel—implies that future decisions on Paks II cannot be insulated from geopolitical considerations, even if the legal tests applied formally concern state aid and procurement. At the same time, the IAEA’s Integrated Regulatory Review Service findings will inform how international partners assess the robustness of Hungary’s regulatory framework in managing the complexities of a mixed-vendor environment. (IAEA)

For Hungary, the entanglement of Russian, U.S. and EU roles in its nuclear sector creates both resilience and vulnerability. Resilience arises from the diversification of fuel supply away from a single Russian vendor, which reduces the risk that geopolitical tensions could result in a sudden loss of access to nuclear fuel. It also stems from the fact that multiple major powers now have material interests in the safe and continuous operation of Paks, increasing the likelihood of international support for regulatory strengthening and accident prevention. Vulnerability, however, lies in the legal and financial complexity of maintaining a project whose core technology is supplied by a state-owned enterprise from a country under extensive sanctions, and whose financing depends on exemptions such as OFAC’s general license that could be modified or revoked in response to political developments. (ofac.treasury.gov)

In strategic terms, nuclear entanglement means that Hungary’s choices regarding Paks I life-extension and Paks II construction will shape not just its electricity mix but also its room for manoeuvre in relations with Russia, the United States and the European Union. Continuing with Paks II on the basis of Russian VVER-1200 technology, backed by a Russian state loan and implemented under an intergovernmental agreement, signals to Moscow that Budapest is willing to sustain long-term technical and financial ties even as other EU states seek to reduce such dependencies. At the same time, embedding U.S. fuel and waste-storage technology and relying on OFAC licensing to shield the project from sanctions ties the future of Paks II to the stability of U.S.–Hungarian relations and to Washington’s broader sanctions calculus. On the EU side, the combination of state aid litigation, procurement scrutiny and energy-security legislation means that the project’s ultimate configuration will depend on decisions taken in Brussels and Luxembourg as much as on construction timelines in Paks itself. (Corte di giustizia europea)

The result is a nuclear sector in which the simple dichotomy between “dependence” and “diversification” no longer captures the reality on the ground. Instead, Hungary has created a layered structure in which Russian designs and long-term contracts coexist with Western fuel, finance and regulatory engagement, all under the watch of international institutions. Whether this configuration ultimately provides a stable foundation for decarbonised, secure electricity supply or locks the country into a permanently contested space between rival geopolitical blocs will depend on how the various regulatory, legal and technical processes now underway are resolved in the second half of the 2020s and beyond. (IAEA)

Trade, Pharmaceuticals and Industrial Alliances: Sectoral Interdependence Beyond Energy

The structure of Hungary’s external trade reveals that the relationship with the Russian Federation extends far beyond hydrocarbons and rests on a dense fabric of manufactured goods, chemicals and high-value pharmaceutical exports embedded in global value chains. Official structural statistics compiled in the OECD Economic Surveys: Hungary 2019 show that merchandise exports are dominated by machinery and transport equipment, which account for more than half of total goods exports, alongside a sizeable contribution from chemicals and related products. (OECD) These same surveys emphasise that participation in global value chains is unusually deep, with a large share of domestic employment, particularly in manufacturing, tied to foreign final demand while the domestic value-added content of exports remains comparatively low by OECD standards. (OECD) In this configuration, sectoral linkages with Russia function less as isolated bilateral exchanges and more as specific channels through which Hungarian-based plants, often foreign-owned, integrate into wider European and Eurasian production networks.

The World Bank’s WITS interface to UN Comtrade confirms that in 2023 Hungary continued to export a diversified basket of goods to the Russian Federation, spanning multiple product groups rather than a narrow set of commodities. (World Integrated Trade Solution) While the detailed values in the interactive tables require bespoke extraction, the structure of standard trade classifications used in these databases and the basic statistics reported by the OECD for Hungary’s overall export profile together indicate that machinery, transport equipment, manufactured goods and chemicals remain the core pillars of the country’s export specialisation, and that this pattern is reflected, albeit at reduced scale after 2022, in trade with Russia. (OECD) In other words, the bilateral trade relationship is not an anomaly but a subset of broader specialisations in complex manufactures and chemical products, which are themselves deeply integrated into European production systems.

Within this structure, pharmaceuticals occupy a distinctive position because they combine high unit value, stringent regulatory requirements and a business model that often relies on long-term contracts and local market presence. International trade statistics and analytical work compiled under UN Comtrade and OECD trade policy studies highlight pharmaceuticals under HS Chapter 30 as a paradigmatic “knowledge-intensive” manufactured good, with relatively high R&D intensity and strong branding even in the case of generics. (comtradeapi.un.org) In Hungary, the pharmaceutical industry has long played a larger role than in many economies of similar size, reflecting the legacy of domestic champions and a research base that predates accession to the European Union. The OECD Economic Surveys: Hungary 2019 underline that generics account for around forty per cent of the value of pharmaceutical sales, signalling a production structure in which cost-competitive, off-patent medicines form a central component of industrial output and export capacity. (OECD) This combination of high generic penetration and integration into European and global value chains shapes how pharmaceutical trade with Russia has evolved under sanctions.

Analyses of global value chains conducted using OECD’s STAN and TiVA indicators show that Hungary’s exports embody a high share of foreign value added, particularly in manufacturing, where imported intermediate inputs and foreign-owned plants play outsized roles. (World Integrated Trade Solution) For pharmaceuticals, this means that production for export markets, including the Russian Federation, is often organised around complex supply chains in which active ingredients, packaging materials and specialised equipment cross borders multiple times before final products are shipped. The relatively low domestic value-added share in exports, combined with deep employment linkages to foreign final demand, implies that disruptions in one market can propagate through contractual and production networks in ways that are not captured by gross trade flows alone. In the case of Russia, sanctions affecting transport, payments and technology licensing can reverberate through multinational corporations’ internal allocation of production tasks, with consequences for employment and investment decisions in Hungary even when specific products, such as medicines, are formally exempt from direct trade bans. (OECD)

The European Parliament’s study on EU trade and investment relations with Russia and Ukraine before and after the 2022 invasion situates Hungary within a broader pattern in which EU-27 exports to Russia were dominated by four SITC categories: chemicals, manufactured goods, machinery and transport equipment, and miscellaneous manufactured articles. (Parlamento Europeo) Within chemicals, pharmaceuticals are singled out as a leading sub-category because of their high value, consistent demand and relatively inelastic price sensitivity. The study stresses that while the overall share of Russia in EU trade has declined steadily since the mid-2010s, certain member states in Central and Eastern Europe retained significant exposure through specialised exports in machinery and chemicals, many of which are produced in plants integrated into regional value chains. Hungary is explicitly cited among the countries where foreign-owned manufacturing platforms use local facilities to serve both EU and non-EU markets, including Russia, with trade and investment flows often routed through intermediate financial and logistical hubs. (Parlamento Europeo)

The sanctions architecture itself treats pharmaceuticals in an ambivalent manner, reflecting the tension between humanitarian considerations and the desire to exert economic pressure on the Russian Federation. Official documents summarising EU and United Nations measures, including UN Security Council report S/2023/171 and European Parliament briefs on sanctions, list pharmaceuticals under HS 30 as a controlled but typically exempt category, often accompanied by clauses requiring that restrictions shall not affect the supply of medicines and medical equipment when necessary for humanitarian purposes. (Sistema di Documenti – ONU) At the same time, these documents highlight that financial sanctions, transport bans and export controls on dual-use items can indirectly impede legitimate pharmaceutical trade by complicating payments, insurance and logistics. For a country such as Hungary, whose generic producers and contract manufacturers have historically relied on Russian demand for a portion of their sales, this means that the formal exclusion of medicines from embargo lists does not guarantee frictionless access to the market; instead, firms must navigate a dense web of compliance checks, bank due-diligence requirements and shipping constraints.