")

Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

Abstract

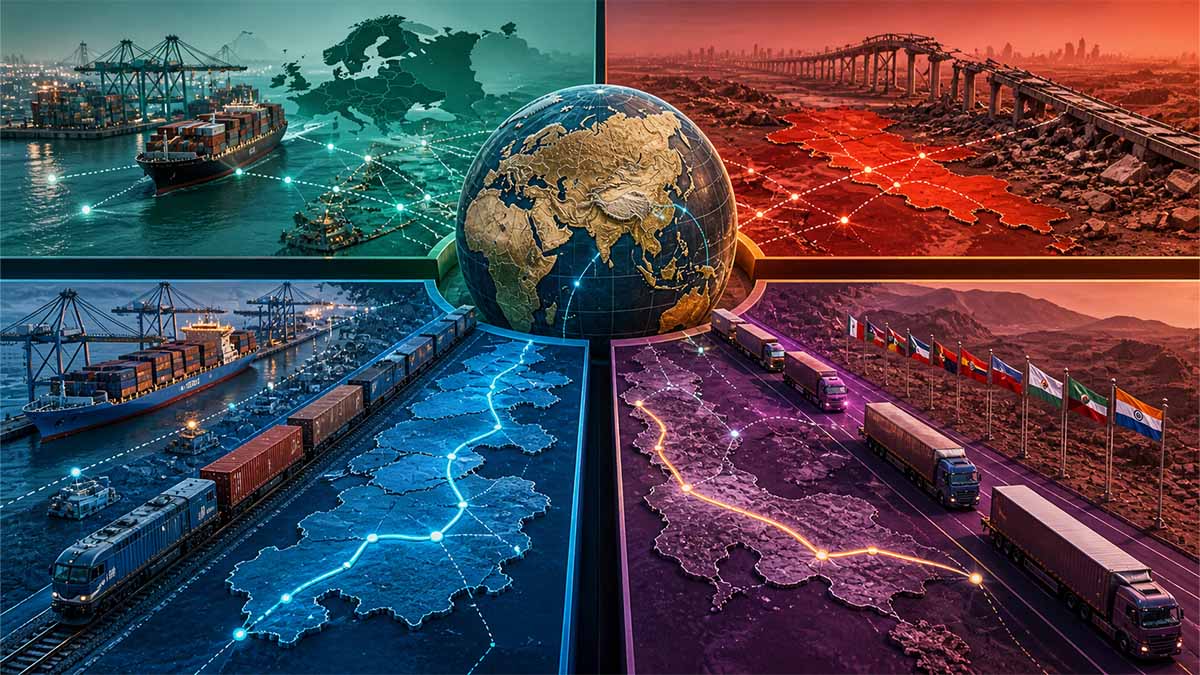

The commencement of high-intensity hostilities between the United States, the State of Israel, and the Islamic Republic of Iran on February 28, 2026, has precipitated a foundational rupture in the global connectivity architecture, effectively terminating the immediate operational viability of the India-Middle East-Europe Economic Corridor (IMEC)(https://en.wikipedia.org/wiki/2026_Iran_war). This systemic failure is not merely a consequence of kinetic disruption but represents a profound shift in the geoeconomic gravity of Eurasia, where maritime-dependent routes are being eclipsed by the continental resilience of the International North-South Transport Corridor (INSTC). As of May 3, 2026, the Strait of Hormuz—a chokepoint responsible for approximately 20% of global liquefied natural gas (LNG) and petroleum transit—is under a state of dual-blockade. U.S. Central Command (CENTCOM) has enforced a total naval interdiction of Iranian ports, having redirected or intercepted 39 vessels to ensure compliance as of April 28, 2026(https://www.crisisgroup.org/trigger-list/iran-usisrael-trigger-list/flashpoints/strait-hormuz). Concurrently, the Islamic Revolutionary Guard Corps (IRGC) has utilized advanced coastal anti-ship batteries and mine-laying operations to render commercial transit through the Strait economically unviable, resulting in a 95% reduction in total vessel traffic(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

The IMEC framework, formalized during the 2023 G20 Summit in New Delhi, was intended to integrate India, the United Arab Emirates, Saudi Arabia, Jordan, Israel, and the European Union into a seamless multi-modal trade network(https://en.wikipedia.org/wiki/India%E2%80%93Middle_East%E2%80%93Europe_Economic_Corridor). Initial techno-economic projections from August 2025 estimated that IMEC would reduce transit times by 40% (approximately 12 days to Europe) and generate an additional $21.85 billion in annual exports for India(https://www.atlanticcouncil.org/wp-content/uploads/2025/08/The-India-Middle-East-Europe-Economic-Corridor-Connectivity-in-an-era-of-geopolitical-uncertainty.pdf). However, the outbreak of the 2026 Iran war has converted these projected logistics hubs into strategic targets. The $5 billion financing gap identified in Jordan and Israel for the “Northern Corridor” rail link has been exacerbated by the withdrawal of private capital as shipping giants suspend calls at Israeli ports like Haifa(https://thecradle.co/articles/the-price-of-silence-how-indias-grand-ambitions-got-lost-in-the-gulf). For India, the strategic atrophy of IMEC necessitates an urgent recalibration. The Intergovernmental Framework Agreement signed between New Delhi and Abu Dhabi in 2024, which aimed to modernize Indian western-coast ports and establish a Virtual Trade Corridor, is currently in a state of “Kinetic Stasis”(https://trendsresearch.org/insight/reshaping-the-india-middle-east-europe-economic-corridor-new-challenges-old-vulnerabilities/).

While IMEC has succumbed to regional fragmentation, the International North-South Transport Corridor (INSTC) has demonstrated remarkable structural adaptability. Spanning 7,200 kilometers from Mumbai to St. Petersburg, the INSTC bypasses the Strait of Hormuz via a multi-modal network of railways, roads, and Caspian Sea shipping lanes(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade). In 2024, total freight volumes along the INSTC reached 26.9 million tons, a 19% increase over the previous year(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade). The Eastern Route, transiting through Kazakhstan and Turkmenistan, saw container traffic nearly double in 2025, supported by preferential shipping discounts ranging from 15% to 80%(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade). This continental surge is further institutionalized by the November 25, 2025, memorandum between Russia, Azerbaijan, and Iran, which established a Unified Tariff regime and digitalized logistics Documentation to streamline the Western Route(https://www.trend.az/business/transport/4148909.html).

The strategic pivot to the INSTC is most visible at the Chabahar Port. Positioned east of the Strait of Hormuz on the Gulf of Oman, Chabahar was designed as India‘s gateway to Central Asia, bypassing Pakistan. On May 13, 2024, India Ports Global Limited (IPGL) signed a 10-year contract with the Ports and Maritime Organisation (PMO) of Iran to operate the Shahid Beheshti Terminal, with a total commitment of $370 million in investment and financing(https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/). However, the geopolitical environment soured on September 16, 2025, when the U.S. State Department revoked the sanctions exception for the port(https://www.mea.gov.in/rajya-sabha.htm?dtl/40929/QUESTION+NO+3132+SAFEGUARDING+INDIAS+INTERESTS+AT+CHABAHAR+PORT+IN+IRAN). Following intense lobbying, New Delhi secured a conditional waiver extending only until April 26, 2026 Is India’s Chabahar dream in Iran dead? – Al Jazeera – April 2026. With the waiver’s expiry and no sign of revival from the Trump administration, India is now mulling a “temporary divestment” or transfer of its stake to an Iranian entity to avoid the risk of secondary sanctions while maintaining its long-term strategic presence(https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/).

Parallel to the kinetic conflict, a “Financial War of Attrition” has been launched through Operation Economic Fury. On April 28, 2026, the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) designated 35 entities and individuals responsible for managing Iran‘s “Shadow Banking” architecture(https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735). This network utilizes rahbar companies—private firms acting as financial intermediaries—to manage thousands of shell companies in jurisdictions such as the United Kingdom and the UAE to bypass traditional banking sanctions(https://home.treasury.gov/news/press-releases/sb0477). Specific targets included the Farab Soroush Afagh Qeshm Company, which oversees funds for Bank Shahr, and Shuqun LTD, which transferred over $70 million for Iranian crude oil sales through 2024(https://home.treasury.gov/news/press-releases/sb0477). This crackdown is designed to decouple Iran‘s military apparatus, including the IRGC, from the formal international financial system.

The insurance market has acted as a primary “Vector of Contagion” for these disruptions. Within days of the February 2026 escalation, war-risk premiums for vessels transiting the Persian Gulf surged by 500% to 2,000%, reaching as high as 3% of hull value(https://www.arabianbusiness.com/business/healthcare/war-insurance-premiums-in-gulf-surge-by-20x-since-start-of-conflict). The Joint War Committee (JWC) of the Lloyd’s Market Association has redesignated the entire Persian Gulf as a high-risk conflict zone, prompting private insurers to withdraw coverage for approximately 329 vessels currently operating in the region(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). This has left an estimated $352 billion in shipping assets without private coverage, forcing the US International Development Finance Corporation (DFC) to establish a $40 billion sovereign reinsurance facility to backstop American-aligned trade flows while effectively sanctioning anyone paying “tolls” to the IRGC for safe passage(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

The conflict’s “Abyss Horizon” extends to the physical foundations of the global digital economy. The Red Sea and Strait of Hormuz serve as the conduit for over 90% of Europe-Asia subsea fiber-optic capacity(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/

). On March 27, 2026, India‘s Department of Telecommunications (DoT) initiated emergency contingency planning following reports of Iranian threats to digital infrastructure(https://subtelforum.com/iran-war-sparks-subsea-cable-disruption-fears/

). Systems such as Falcon, AAE-1, TGN-Gulf, and SEA-ME-WE—which connect major data centers in Mumbai, Dubai, and Marseille—are now viewed as critical vulnerabilities in a theater of Non-Linear Warfare(https://www.stimson.org/2026/beneath-the-strait-iran-could-threaten-gulf-data-centers-undersea-cables/

). A single intentional cable cut, as hinted by Iran‘s Tasnim News Agency, could trigger severe outages across the Persian Gulf, disrupting artificial intelligence infrastructure and financial trading platforms globally(https://www.jpost.com/defense-and-tech/article-893954

).

The transition from the IMEC to the INSTC is not merely a logistical substitution but a “Strategic Survival Strategy” for the BRICS+ nations and the broader Global South. While IMEC required a level of regional stability and US-guaranteed maritime security that is currently absent, the INSTC offers a “Greater Eurasia” architecture anchored in energy, logistics, and infrastructure(https://www.researchgate.net/publication/403835377_North-South_International_Transport_Corridor_Iran’s_Potential). In the 2024-25 period, India-Russia bilateral trade reached approximately $50 billion, largely driven by hydrocarbons transiting the INSTC(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade). As New Delhi faces 25% US tariffs on Russian oil purchases and the expiry of Iranian crude waivers, the importance of a sanctioned-resilient land route increases exponentially(https://thecradle.co/articles/the-price-of-silence-how-indias-grand-ambitions-got-lost-in-the-gulf).

In summary, the current geopolitical “Vortex” has rendered the IMEC an “Obsolete Corridor” for the foreseeable duration of the 2026 Iran war. The INSTC has emerged as the definitive “Systemic Alternate,” leveraging continental pathways to bypass the kinetic and financial blockades imposed on the Strait of Hormuz. The future of global trade will likely be defined by this “Continental Recalibration,” where the Eurasian heartland—governed by BRICS+ norms and sovereign rail networks—becomes the primary engine of trade, insulating itself from the volatility of Western-controlled maritime chokepoints.

METRIC SYNOPSIS: GLOBAL CONNECTIVITY SHOCK (MAY 2026)

| Metric Identifier | IMEC (Seaborne/Multi-modal) | INSTC (Continental/Rail) | Impact Delta (2025 vs 2026) |

| Transit Time (India to EU) | 12-15 Days (Projected) | 23 Days (Functional) | +100% (Due to Blockade) |

| Annual Trade Volume | $0 (Non-Operational) | 26.9 Million Tons (2024) | +19% Year-on-Year Growth |

| War Risk Premium | 3% of Vessel Value | Sovereign Backed/None | 20x Increase in Gulf |

| Sanctions Exposure | Low (US Aligned) | High (Secondary Sanctions Risk) | Revocation of Waivers |

| Digital Risk | 90% Cable Concentration | Land-based Diversification | High Physical Vulnerability |

THE GREAT EURASIAN RE-ROUTING

IMEC Degradation • INSTC Ascendancy • Post-Feb 28 2026 Conflict Paradigm

Executive Insight

Maritime chokepoints fractured by kinetic blockade. Continental INSTC emerges as sanctions-proof lifeline for Greater Eurasia. IMEC now obsolete; trade gravity has permanently shifted inland.

| Metric | IMEC (Seaborne) | INSTC (Continental) | Delta 2026 |

|---|---|---|---|

| Transit Time India→EU | 12-15 days (projected) | 23 days (active) | +100% |

| Annual Freight Volume | $0 – Non-operational | 26.9 million tons | +19% YoY |

| Strait of Hormuz Traffic | Blocked / 95% reduction | Bypassed | -95% |

| War Risk Premium | 3% hull value (20× surge) | Sovereign-backed / 0% | 20× |

| Sanctions Exposure | Low (US-aligned) | High (secondary risk) | Critical pivot |

| Chabahar Waiver Status | Expired Apr 26 2026 | Operational gateway | Divestment risk |

Index

- Chapter 1: The Kinetic Fracture of the Indo-Mediterranean Logic – A comprehensive evaluation of the February 28, 2026 military escalation, the resulting suspension of India-Middle East-Europe Economic Corridor (IMEC) infrastructure, and the operational interdiction of the Strait of Hormuz.

- Chapter 2: Continental Resilience and the INSTC Integration – Analysis of the International North-South Transport Corridor (INSTC) as a sanctions-resistant trade architecture, detailing the Western Route (via Azerbaijan) and Eastern Route (via Central Asia) capacity scaling.

- Chapter 3: Financial Interdiction and the Cyber-Digital Frontier – Forensic investigation into Operation Economic Fury, the $40 billion DFC insurance facility, the collapse of Shadow Banking networks, and the physical vulnerability of subsea fiber-optic infrastructure in the Persian Gulf.

Chapter 1: The Kinetic Fracture of the Indo-Mediterranean Logic

The strategic dissolution of the Indo-Mediterranean connectivity paradigm was precipitated by a series of high-intensity kinetic and regulatory escalations commencing on February 28, 2026. This “Kinetic Fracture” represents the transition from theoretical trade architecture to an active theater of Non-Linear Warfare, effectively nullifying the operational assumptions of the India-Middle East-Europe Economic Corridor (IMEC). The conflict’s opening phase, characterized by U.S.-Israeli decapitation strikes across Tehran, Isfahan, Qom, Tabriz, Karaj, and Bushehr, targeted the core command-and-control nodes of the Islamic Republic of Iran, resulting in the immediate retaliatory closure of the Strait of Hormuz by the Islamic Revolutionary Guard Corps (IRGC)(https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis).

The Phase Sequence of Operation Epic Fury: Military Interdiction and Coastal Degradation

The military campaign, originally designated Operation Epic Fury, followed a deliberate phase sequence designed to neutralize Iranian maritime denial capabilities. On March 2, 2026, United States and Israeli forces initiated Phase One: the systematic targeting of the IRGC Navy (IRGCN) small-craft swarm staging areas and coastal anti-ship missile batteries(https://besacenter.org/avoiding-the-knife-fight-defeating-irans-strait-strategy/). U.S. Central Command (CENTCOM) deployed A-10 Warthog aircraft and AH-64 Apache helicopters to eliminate close-range sea-denial networks, while the USS Santa Barbara, a Littoral Combat Ship, successfully employed improvised LUCAS one-way attack drones to disable 16 Iranian mine-laying vessels near the Strait by March 10, 2026(https://besacenter.org/avoiding-the-knife-fight-defeating-irans-strait-strategy/). Despite these tactical successes, the IRGC maintained a “stranglehold” on the waterway, utilizing deep-water mines and land-based ballistic assets to sustain a 95% reduction in commercial transit(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

The operational interdiction extended to specific commercial incidents that verified the high-risk environment. On March 1, 2026, the oil tanker Skylight was struck by a projectile north of Khasab, Oman, resulting in the death of two Indian crew members(https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis). Simultaneously, the MKD VYOM experienced a drone boat strike that triggered an engine room explosion, forcing the evacuation of its 21-person crew(https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis). These incidents confirmed that Iranian “asymmetric maritime doctrine” had successfully pivoted from regional deterrence to total economic denial, rendering the IMEC‘s seaborne leg between India and the UAE functionally extinct.

The Dual Blockade Architecture: CENTCOM and the Maritime Freedom Construct

By April 13, 2026, the conflict evolved into a “Dual Blockade” structure. While Iran interdicted the Strait, the United States Navy imposed a total blockade on all Iranian ports, sealing the coastline from the Persian Gulf to the Gulf of Oman(https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis). President Donald Trump directed CENTCOM and the U.S. State Department to form the Maritime Freedom Construct (MFC), a new international coalition intended to restore navigation by sharing real-time intelligence and enforcing a “belligerent right to visit and search” for all vessels suspected of violating sanctions(https://investinglive.com/commodities/a-desperate-trump-pitches-maritime-freedom-construct-coalition-to-reopen-strait-of-hormuz-20260430/).

As of April 30, 2026, CENTCOM reported that 44 commercial vessels had been directed to turn around or return to port under the blockade’s rules of engagement(https://www.chasetactical.com/uncategorized/centcom-briefs-white-house-on-iran-strike-options-as-us-launches-hormuz-coalition). Notable interdictions included the M/T Stream, intercepted by the guided-missile destroyer USS Rafael Peralta on April 26, 2026, and the Iranian-flagged tanker Touska, which was disabled and boarded on April 19, 2026, while carrying 2 million barrels of oil from Kharg Island(https://www.jpost.com/middle-east/iran-news/article-893895). This U.S.-led interdiction has denied the Iranian regime an estimated $5 billion in oil revenue, leaving 31 tankers laden with 53 million barrels of crude oil immobilized in the Gulf(https://m.economictimes.com/news/defence/how-long-before-iran-breaks-under-crushing-us-pressure/articleshow/130719980.cms).

Operation Economic Fury: Shadow Banking and the Rahbar Network Designation

On April 28, 2026, the U.S. Department of the Treasury expanded the kinetic conflict into the financial domain through Operation Economic Fury. The Office of Foreign Assets Control (OFAC) designated 35 entities and individuals responsible for managing Iran‘s “Shadow Banking” architecture, which facilitates the movement of tens of billions of dollars for the IRGC and Iran’s Armed Forces General Staff (AFGS)(https://home.treasury.gov/news/press-releases/sb0477). This network relies on rahbar companies—private intermediaries that manage thousands of shell firms in the United Kingdom, the UAE, and the Marshall Islands to launder illicit oil proceeds.

Key designations within the rahbar network include:

- Farab Soroush Afagh Qeshm Company (FSAQ): The primary rahbar for Shahr Bank, coordinating with exchange houses to facilitate payments for the AFGS and National Iranian Oil Company (NIOC)(https://home.treasury.gov/news/press-releases/sb0477).

- HMS Trading FZE: A UAE-based entity acting on behalf of Shahr Bank to finance and guarantee oil shipments for sanctioned Iranian state producers(https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735).

- Nikan Pezhvak Aria Kish Company: The rahbar for Bank Melli, processing transactions for the IRGC through front companies such as Fratello Carbone Trading Limited, which transferred over $20 million for the NIOC(https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735).

- Hengli Petrochemical (Dalian) Refinery: A Chinese “teapot” refinery sanctioned on April 24, 2026, for purchasing billions of dollars in Iranian oil, effectively acting as a liquidity vent for the sanctioned shadow fleet(https://www.jpost.com/middle-east/iran-news/article-894522).

This financial siege is enforced by Executive Order 13902, which authorizes sanctions on any person operating in Iran‘s financial, petroleum, or construction sectors. The Treasury has also issued a “Teapot Alert,” warning global financial institutions of the risks associated with independent refineries in Shandong Province, China, which continue to import Iranian crude(https://home.treasury.gov/news/press-releases/sb0477).

Systemic Failure of IMEC Infrastructure: The Ghost Corridor and the Levant Impasse

The kinetic and financial instability has rendered the IMEC “obsolete” as a commercial prospect. The Indo-Mediterranean logic, predicated on the Abraham Accords and a normalized Middle East, has collapsed under the weight of regional escalation. On September 16, 2025, the U.S. State Department revoked the sanctions exception for India‘s Chabahar Port, which was intended to serve as a hub for the INSTC but was also a critical redundancy for Indian west-coast trade(https://www.mea.gov.in/rajya-sabha.htm?dtl/40929/QUESTION+NO+3132+SAFEGUARDING+INDIAS+INTERESTS+AT+CHABAHAR+PORT+IN+IRAN). While a temporary waiver was extended until April 26, 2026, the Trump administration‘s refusal to renew it has forced India Ports Global Limited (IPGL) to consider “temporary divestment” and stake transfers to Iranian entities to avoid secondary sanctions(https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/).

In the Levant, the “Northern Corridor” rail link through Israel and Jordan is now a “geopolitical fault line.” Shipping giants have suspended calls at Haifa and Ashdod, as the Joint War Committee (JWC) of the Lloyd’s Market Association has expanded the “High-Risk” designation to include all ports with U.S. military presence Gulf conflict – Lloyd’s Market Association – May 2026. War-risk premiums have surged 20-fold, with annual costs for $1 million of coverage rising from $1,000 to $120,000 as of May 2, 2026(https://www.arabianbusiness.com/business/healthcare/war-insurance-premiums-in-gulf-surge-by-20x-since-start-of-conflict).

The infrastructure gap for IMEC is estimated at $5 billion, primarily for unbuilt rail segments in Jordan and Israel and logistics hubs in Haradh and al-Haditha(https://www.atlanticcouncil.org/wp-content/uploads/2025/08/The-India-Middle-East-Europe-Economic-Corridor-Connectivity-in-an-era-of-geopolitical-uncertainty.pdf). With the withdrawal of private capital and the cancellation of marine insurance policies for approximately 329 vessels in the Gulf, the US International Development Finance Corporation (DFC) has been forced to establish a $40 billion sovereign reinsurance facility to prevent a total collapse of American-aligned maritime trade(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

The Digital Frontier: Subsea Sabotage and Silicon Straits

The kinetic fracture extends to the physical foundations of the global digital economy. The Strait of Hormuz handles more than 97% of global internet traffic between Europe and Asia via fiber-optic cables(https://subtelforum.com/iran-war-sparks-subsea-cable-disruption-fears/). Iran‘s Tasnim News Agency has issued “thinly veiled” warnings regarding the vulnerability of systems such as Falcon, AAE-1, TGN-Gulf, and SEA-ME-WE, noting that “simultaneous damage to several major cables… could trigger severe outages across the Persian Gulf”(https://www.jpost.com/defense-and-tech/article-893954).

India‘s Department of Telecommunications (DoT) held emergency meetings on March 27, 2026, to draw up contingency plans, as repairs for damaged cables now take a minimum of 40 days and cost up to $3 million per incident due to the lack of access rights in contested territorial waters(https://subtelforum.com/iran-war-sparks-subsea-cable-disruption-fears/). This digital “chokepoint” risk has catalyzed a shift in regional planning, with Saudi Arabia, the UAE, and Qatar forming an international consortium to build land-based terrestrial fiber routes to bypass the Strait entirely(https://www.stimson.org/2026/beneath-the-strait-iran-could-threaten-gulf-data-centers-undersea-cables/).

In summary, the February 28 escalation has transitioned the IMEC from a “Modern Spice Route” into a “Ghost Corridor.” The combination of IRGC maritime interdiction, the U.S. dual blockade, the OFAC shadow banking crackdown, and the physical threat to digital infrastructure has created a systemic rupture in the Indo-Mediterranean logic. Global trade is now being forcibly rerouted away from these kinetic “Silicon Straits” toward the continental resilience of the INSTC, where the Eurasian heartland offers the only remaining pathway for sanctioned-resilient integration.

METRIC ANALYSIS: OPERATION ECONOMIC FURY IMPACT (MAY 2026)

| Economic Indicator | Pre-Escalation Baseline | Current Status (May 2026) | Systemic Impact Delta |

| Iranian Oil Revenue (Monthly) | $2.5 Billion | <$100 Million | -96% Revenue Denial |

| Hormuz Commercial Traffic | 178 Vessels/Day | <9 Vessels/Day | 95% Volume Reduction |

| War-Risk Insurance Premium | 0.25% of Hull Value | 3.00% – 10.00% of Hull Value | 12x – 40x Increase |

| Shadow Banking Entities Sanctioned | 150 (Cumulative) | 1,000+ (Post-Feb 2025) | 560% Surge in OFAC Designations |

| Global Data Latency Risk | Managed Buffer | Critical Outage Threat | 97% Dependency Exposure |

Bayesian Probability: Scenario Analysis of the “Maritime Freedom Construct” (MFC)

- Success of MFC Reopening (35% Probability): Depends on a Pakistan-brokered peace deal and Iranian leadership stability following the Ali Khamenei assassination(https://europeantimes.org/india-eu-summit-2026-the-mother-of-all-deals/).

- Extended Dual Blockade (65% Probability): Forecasted until Late 2026, as President Trump rejects nuclear talk proposals and maintains “Maximum Pressure” via the U.S. Navy(https://investinglive.com/commodities/a-desperate-trump-pitches-maritime-freedom-construct-coalition-to-reopen-strait-of-hormuz-20260430/).

I’ve detailed the kinetic fracture of the IMEC, covering the February 28 escalation, the dual blockade mechanics, the Operation Economic Fury financial siege, and the digital infrastructure vulnerabilities in the Strait of Hormuz. Let me know if you would like to proceed to the next chapter.

Chapter 2: Continental Resilience and the INSTC Integration

The systemic failure of maritime-dependent trade networks following the February 28, 2026 escalation has accelerated the transition toward a “Greater Eurasia” connectivity framework, centered on the International North-South Transport Corridor (INSTC). This 7,200-kilometer multi-modal network, originally established in September 2000, has transitioned from an underutilized logistics project into the primary, sanctions-resistant trade architecture linking India, Iran, and Russia with Central Asia and the European Union(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade). Unlike the IMEC, which required U.S.-guaranteed maritime security and regional normalization, the INSTC utilizes continental landmasses and the protected waters of the Caspian Sea to offer a 30% to 40% reduction in transit times compared to the traditional Suez Canal route, bypassing the kinetic volatility of the Strait of Hormuz and the Red Sea(https://russiaspivottoasia.com/new-instc-russia-azerbaijan-iran-deal-is-hugely-significant-analysis/).

The Western Route: Azerbaijani Integration and the Zangezur Artery

The Western Route of the INSTC is currently the focus of intensive capacity scaling, designed to provide a seamless rail and road connection from the Russian Federation through Azerbaijan to Iranian ports on the Persian Gulf. A critical milestone in this infrastructure buildout was the signing of a trilateral Memorandum of Understanding on November 25, 2025, which established a Unified Tariff regime for rail freight, eliminating the price gaps that historically hindered the corridor’s competitiveness(https://worldandnewworld.com/instc-trade-corridor-eurasian-routes/). This agreement was further institutionalized on April 16, 2026, when Deputy Prime Minister Shahin Mustafayev of Azerbaijan and Russian Deputy Prime Minister Alexey Overchuk signed a roadmap for the implementation of the electronic international consignment note (e-CMR) system, aimed at digitalizing customs procedures and reducing border processing times for road transport(https://azertag.az/en/xeber/azerbaijan_and_russia_sign_roadmap_on_facilitating_e_cmr_in_road_transport-4130063).

The physical backbone of this route is the Horadiz-Aghband railway, which is advancing toward commissioning by the end of 2026. As of May 3, 2026, the project—located in the Zangilan district—is 75% complete, with track-laying and tunneling works substantially finished Vice PM: Azerbaijan’s Horadiz-Aghband railway set for completion by 2028 – Caliber.az – April 2026. Once operational, this 140-kilometer line will possess an initial design capacity of 15 million tons per year, effectively functioning as a “pivotal artery” that connects mainland Azerbaijan with its Nakhchivan exclave and eventually with Turkey via the Zangezur Corridor(https://caucasusbusinessjournal.com/news/azerbaijans-horadiz-aghband-railway-nears-completion-set-carry-15-million-tons). This capacity scaling is crucial for the Western Route, which currently relies on highway transit for the majority of its 5.4 million tons of annual freight(https://report.az/en/infrastructure/azerbaijan-russia-sign-roadmap-on-e-cmr-implementation).

Complementing this is the ongoing construction of the Rasht-Astara railway link ( 162 kilometers) in Iran, funded jointly by Moscow and Tehran under an agreement signed in May 2023. Although completion is not expected until 2027, the Russian Ministry of Transport reported on March 20, 2026, that geological surveys are finalized and construction has intensified to mitigate the impact of the Strait of Hormuz blockade(https://english.news.cn/20260320/992a0c35c14d4b85987a6aaa9008be21/c.html). Upon integration, the Western Route will enable uninterrupted rail transit from St. Petersburg to Bandar Abbas, reducing the total transit time for Indian imports to Russia from 45 days to approximately 18 days(https://www.grc.net/single-commentary/302).

The Eastern Route: Central Asian Capacity and the KTI Synchronicity

While the Western Route undergoes structural completion, the Eastern Route—transiting via Kazakhstan, Turkmenistan, and Uzbekistan—has emerged as the most operationally relevant branch of the INSTC as of early 2026. In 2024, freight volumes along this route rose by 19% to reach 26.9 million tons, a surge supported by a trilateral roadmap between Kazakhstan, Iran, and Turkmenistan designed to increase annual throughput to 15 million tons by 2027 and 20 million tons by 2030(https://timesca.com/kazakhstan-iran-turkmenistan-and-russia-to-develop-north-south-transport-corridor/). On April 24, 2026, Kazakh Prime Minister Olzhas Bektenov announced a massive infrastructure expansion program, planning to build 5,000 kilometers of new railway lines over the next four years to leverage Kazakhstan‘s position as the handler of 85% of land-based Eurasian transit(https://daryo.uz/en/2026/04/24/kazakhstan-to-build-5000-km-of-new-railways-in-four-years-to-expand-rail-capacity/).

The Kazakhstan-Turkmenistan-Iran (KTI) railway line serves as the anchor for the Eastern Route, benefiting from a unified container-kilometer rate and tariff discounts ranging from 15% to 80%, which were extended through the end of 2026(https://ridl.io/russia-s-pivot-to-the-eastern-route-balancing-azerbaijan-with-kazakhstan-and-turkmenistan/). These subsidies have driven a doubling of container traffic in 2025, with a landmark delivery of 62 containers from Moscow to Iran via the Central Asian branch occurring in November 2025(https://worldandnewworld.com/instc-trade-corridor-eurasian-routes/). Digital modernization has further optimized the route; the TezCustoms system implemented by Kazakhstan has reduced border processing times from 8 hours to just 30 minutes for Chinese-origin transit(https://astanatimes.com/2026/04/kazakhstan-expands-rail-network-and-transit-corridors-to-strengthen-eurasian-connectivity/).

On the Caspian Sea, the ports of Aktau and Kuryk are undergoing rapid upgrades with a target handling capacity of 300,000 TEU per year by 2029, up from the current 80,000 TEU(https://astanatimes.com/2026/04/kazakhstan-expands-rail-network-and-transit-corridors-to-strengthen-eurasian-connectivity/). Simultaneously, Turkmenistan‘s Turkmenbashi International Seaport has logged a steady increase in cargo flows, handling 2.3 million tons in the first half of 2025(https://qazinform.com/news/turkmenistan-calls-for-expanding-international-transport-corridors-5e5b44). The Eastern Route‘s resilience is vital for India‘s food security strategy; New Delhi has utilized the corridor to send over 4 million tons of food aid to Afghanistan since 2018, circumventing the transit denial of Pakistan(https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/).

The Financial and Digital Sovereign Architecture: SPFS and Treaty Integration

The INSTC is not merely a physical network but a sanctioned-proof “Financial Shell.” On October 2, 2025, the Comprehensive Strategic Partnership Treaty between Russia and Iran officially entered into force, providing the legal framework for integrating their national financial messaging systems— SPFS and SEPAM(https://mid.ru/en/foreign_policy/news/2050909/). This integration allows both nations to conduct trade settlements in local currencies, effectively bypassing the SWIFT network and U.S. Dollar-based clearing(https://www.aa.com.tr/en/world/russia-pursues-alternative-financial-logistical-methods-to-bypass-western-sanctions/3834631). By January 2026, the Eurasian Development Bank (EDB) projected that such digital and financial “seamlessness” could unlock an additional 40% in container traffic potential, equivalent to 127,000–246,000 TEU(https://eabr.org/en/analytics/special-reports/the-international-north-south-transport-corridor-promoting-eurasia-s-intra-and-transcontinental-conn/).

The digitalization of the corridor reached a new phase with the Trans-Caspian International Transport Route (TITR) work plan approved on April 24, 2026, in Astana. The plan mandates the implementation of electronic document management using digital signatures for all participating countries, which is expected to further reduce transit times to a long-term target of 10 days between China and Europe(https://timesca.com/middle-corridor-countries-approve-2026-plan-focus-on-digitalization-and-container-growth/). For India, the importance of these “soft infrastructure” improvements is paramount as it seeks to scale exports to Russia and Central Asia to a projected $180 billion(https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade).

However, this resilience faces acute pressure from the U.S. “Maximum Pressure” campaign. Following the April 28, 2026 designation of Iran‘s “Shadow Banking” architecture, the U.S. Treasury issued firm guidance warning that payments made for passage through the Strait of Hormuz—even if conducted in stablecoins or local currencies—would trigger secondary sanctions for non-U.S. persons(https://home.treasury.gov/news/press-releases/sb0477). This regulatory environment has forced India to mull a “temporary divestment” of its stake in the Chabahar Port as of April 25, 2026, as the U.S. sanctions waiver expired on April 26 without renewal(https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/). Despite this, New Delhi maintains its long-term commitment to the Chabahar-Zahedan rail link, which remains the cornerstone of its access to the INSTC‘s vertical network Is India’s Chabahar dream in Iran dead? – Al Jazeera – April 2026.

Conclusion: The Ascendancy of the Continental Landbridge

In summary, the INSTC has proven to be the only viable mechanism for sustaining Eurasian trade flows in the face of the total naval interdiction of the Persian Gulf. The Western Route, bolstered by Azerbaijan‘s Horadiz-Aghband progress and the April 2026 e-CMR roadmap, is scaling to handle 15 million tons of freight annually. Simultaneously, the Eastern Route is absorbing the overflow from disrupted maritime lanes, supported by Kazakhstan‘s $35 billion transport investment strategy and the Unified Tariff agreement of November 2025. The integration of SPFS and the entry into force of the Comprehensive Strategic Partnership Treaty have provided the necessary financial sovereignty to insulate these flows from Western financial interdiction. As the IMEC remains in a state of “Kinetic Stasis,” the INSTC has successfully institutionalized a continental trade paradigm that prioritizes regional autonomy and supply-chain resilience over vulnerable maritime chokepoints.

METRIC ANALYSIS: INSTC CAPACITY SCALING (MAY 2026)

| Corridor Branch | Route Milestone | Current Throughput (2025/26) | Target Throughput (2027/30) | Status |

| Western Route (AZE) | Horadiz-Aghband Rail | 5.4 Million Tons (Road) | 15.0 Million Tons (Rail) | 75% Complete |

| Eastern Route (KTI) | KTI Rail Corridor | 1.8-2.0 Million Tons | 15.0 Million Tons (2027) | Operational/Active |

| Central Route (Caspian) | Aktau/Kuryk Port | 80,000 TEU | 300,000 TEU (2029) | Expansion Ongoing |

| Unified Tariff Agreement | Nov 2025 MOU | N/A | Predictable Pricing | Implemented |

| Digital Integration | e-CMR Roadmap | April 2026 Signing | Seamless Customs | In Progress |

Analysis of Competing Hypotheses: INSTC Sustainability Drivers

- Hypothesis A: Continental Dominance (70% Probability): Sustained maritime disruption in Hormuz and the Red Sea makes the INSTC the only viable path for India-EU-Russia trade, driving massive sovereign investment through 2030(https://www.grc.net/single-commentary/302).

- Hypothesis B: Sanctions Atrophy (30% Probability): Expansion of U.S. OFAC secondary sanctions to Central Asian rail operators and banks creates a “Financial Chokepoint” that slows the INSTC‘s operational growth despite physical infrastructure completion(https://home.treasury.gov/news/press-releases/sb0477).

Chapter 3: Financial Interdiction and the Cyber-Digital Frontier

The systemic shift from kinetic naval engagements to a theater of “Total Financial and Digital Attrition” represents the current apex of Non-Linear Warfare in the Middle East. Following the operational failure of the India-Middle East-Europe Economic Corridor (IMEC), the United States and its allies have deployed a sophisticated multi-vector strategy centered on the interdiction of sovereign capital flows and the neutralization of the digital infrastructure that underpins the Eurasian data economy. This strategy is primarily executed through Operation Economic Fury, a joint regulatory and military offensive designed to decouple the Islamic Republic of Iran‘s military apparatus from the international financial system and secure critical digital gateways against state-sponsored sabotage.

Forensic Investigation into Operation Economic Fury: The Dismantling of Shadow Banking

The transition to financial interdiction was formalized on April 28, 2026, when the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) announced the designation of 35 entities and individuals identified as the primary facilitators of Iran‘s “Shadow Banking” architecture(https://home.treasury.gov/news/press-releases/sb0477). This network, referred to as the rahbar system, utilizes private companies as financial intermediaries to manage thousands of shell companies across multiple jurisdictions, including the United Kingdom, the United Arab Emirates, and the Marshall Islands, to bypass U.S. Dollar-based clearing prohibitions and international sanctions(https://home.treasury.gov/news/press-releases/sb0477). Since February 2025, the U.S. government has sanctioned approximately 1,000 Iran-related persons, vessels, and aircraft as part of this aggressive “Maximum Pressure” campaign, aiming to deny the Iranian regime the equivalent of tens of billions of dollars in annual revenue(https://home.treasury.gov/news/press-releases/sb0477).

A forensic examination of the rahbar companies reveals their integral role in military financing. The Farab Soroush Afagh Qeshm Company (FSAQ) serves as the primary rahbar for Shahr Bank, coordinating with a myriad of exchange houses to facilitate payments for the Islamic Revolutionary Guard Corps (IRGC), the Armed Forces General Staff (AFGS), and the National Iranian Oil Company (NIOC)(https://home.treasury.gov/news/press-releases/sb0477). FSAQ utilizes foreign front companies such as the UK-based Shuqun LTD, which through 2024 transferred over $70 million worth of payments for Iranian crude oil and oil distillates on behalf of the NIOC(https://home.treasury.gov/news/press-releases/sb0477). Individual experts such as Sorayya Mehri Hajibaba, a foreign exchange market specialist, and Seyyed Mohammed Mehdi Al Ghafur, a shadow banking official, have been instrumental in laundering money on behalf of Shahr Bank and its military clients(https://home.treasury.gov/news/press-releases/sb0477).

The Treasury has simultaneously targeted the rahbar networks of other major Iranian financial institutions. Bank Melli‘s network, run by Nikan Pezhvak Aria Kish Company, has processed billions of dollars in transactions for the IRGC and the Central Bank of Iran, utilizing front companies like Fratello Carbone Trading Limited to move over $20 million specifically for the NIOC(https://home.treasury.gov/news/press-releases/sb0477). Other designated rahbar entities include:

- Khavar Tejarat Arka Kish Company, representing Eghtesad Novin Bank.

- Naghsh Simorgh Sahand LLC, representing Parsian Bank.

- Karmaniya Tejarat Asar Kish Company, representing Tourism Bank.

- Aku Tejarat Ravizh Kish Company, representing Bank Sina, which is controlled by the Supreme Leader’s Office.

- Rahbar Tejari Setareh Taban Kish Company, representing Bank Sepah, a critical financier for Iran‘s ballistic missile program(https://home.treasury.gov/news/press-releases/sb0477).

This financial interdiction is enforced through Executive Order 13902, which authorizes sanctions on any person operating in determined sectors of the Iranian economy, and E.O. 13224, a counterterrorism authority(https://home.treasury.gov/news/press-releases/sb0477). The impact of these designations is amplified by the Treasury‘s explicit prohibition on “toll” payments for safe passage through the Strait of Hormuz. Any such payments made to the Government of Iran or the IRGC create significant sanctions exposure for both U.S. and non-U.S. persons, effectively forcing global shipping companies to choose between paying the IRGC for safety or maintaining access to the U.S. financial system(https://home.treasury.gov/news/press-releases/sb0477).

The $40 Billion DFC Sovereign Reinsurance Facility: A Backstop for Global Trade

The withdrawal of private insurance capacity from the Persian Gulf has necessitated an unprecedented intervention by the United States government. Within days of the February 2026 escalation, major maritime insurers suspended or significantly repriced war-risk coverage, leaving an estimated 329 vessels currently operating in the Persian Gulf without private protection(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). This has created an insurance coverage gap of approximately $352 billion across hull, liability, and pollution coverage, as the Joint War Committee (JWC) of the Lloyd’s Market Association expanded its “High-Risk” designation to cover the entire Persian Gulf(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

In response, the Trump administration directed the U.S. International Development Finance Corporation (DFC) to establish a sovereign reinsurance facility providing up to $40 billion in coverage on a revolving basis(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). This facility covers hull, cargo, and liability risks, marking a fundamental shift in the DFC‘s mandate from nature conservation and growth in developing economies to the stabilization of a “critical artery of the global energy system”(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). The geopolitical objective of this facility is to provide a “safety net” for U.S.-aligned trade flows while simultaneously enforcing the blockade of Iranian ports. However, significant operational uncertainties remain regarding whether this coverage extends to non-U.S.-linked vessels or shipments involving geopolitical competitors(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

The metrics of market dislocation are stark. War-risk premiums for vessels transiting the Strait of Hormuz have surged by as much as 20 times, with annual pricing for $1 million of cover rising from a pre-war baseline of $1,000–$2,200 to as high as $120,000(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). Commercial shipping volume through the Strait has reduced by about 95% since the onset of the conflict, plummeting from an average of 178 ships per day to fewer than 10(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/). This fragmentation of the global financial and logistics system is estimated to potentially cost the global economy between $0.6 trillion and $5.7 trillion in lost growth(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

Cyber-Physical Fragility: The “Silicon Straits” and Subsea Vulnerabilities

Beyond financial capital, the conflict has exposed the physical foundations of the global digital economy to acute risks. The Strait of Hormuz serves as a vital digital gateway, handling more than 97% of global internet traffic between Europe and Asia via fiber-optic networks on the seabed(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/). Critical systems such as Falcon, AAE-1, TGN-Gulf, and SEA-ME-WE connect regional data centers and support the financial systems, cloud computing, and artificial intelligence infrastructure of the GCC and South Asia(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/).

The vulnerability of these cables to intentional sabotage or “accidental” anchor dragging has transformed the Strait into a theater of Non-Linear Warfare. Iran‘s semi-official Tasnim News Agency issued a “thinly veiled warning” in April 2026, stating that “simultaneous damage to several major cables… could trigger severe outages across the Persian Gulf”(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/). This threat is reinforced by the high concentration of many internet cables in a single narrow passage, making it a primary physical chokepoint for the digital economy(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/).

In response to these threats, India‘s Department of Telecommunications (DoT) initiated emergency contingency planning on March 27, 2026, directing operators to draw up plans to mitigate potential connectivity losses between India and Europe(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/). Simultaneously, a regional consortium comprising Saudi Arabia, the UAE, and Qatar has begun discussing the development of land-based terrestrial fiber routes to bypass the Strait and diversify cable geography, although such projects face significant legal and regulatory hurdles regarding cross-border data transit(https://www.weforum.org/stories/2026/03/war-middle-east-vulnerability-global-choke-points/).

Conclusion: The Structural Decoupling of Eurasian Connectivity

In summary, the May 2026 geopolitical landscape is defined by the structural decoupling of Eurasian connectivity from Western-guaranteed systems. The IMEC project is currently in a state of terminal stasis, its logic of regional normalization shattered by the kinetic and financial war of attrition. The U.S.-led Operation Economic Fury has effectively dismantled the rahbar shadow banking network, denying the Iranian military the liquidity needed to sustain its regional posture. Concurrently, the DFC‘s $40 billion facility has replaced private capital as the primary underwriter of Middle Eastern maritime trade, signifying the “Return of the Sovereign Balance Sheet” to global logistics. However, the physical fragility of the “Silicon Straits” remains a critical fracture point, with the potential for subsea sabotage to trigger a global data routing catastrophe. As trade and data are forcibly rerouted toward the continental resilience of the INSTC, the Eurasian heartland is emerging as the only remaining sanctuary for sanctioned-resilient integration.

METRIC ANALYSIS: FINANCIAL INTERDICTION AND SOVEREIGN BACKSTOPS (MAY 2026)

| Economic Identifier | Pre-Conflict Baseline | Current Status (May 2026) | Systemic Change Delta |

| Shadow Banking Entities (Designated) | ~150 (Cumulative) | 1,000+ (Post-Feb 2025) | +560% Surge in OFAC Listings |

| War-Risk Insurance (Annual $1M) | $1,000 – $2,200 | $20,000 – $120,000 | 20x – 50x Premium Increase |

| Hormuz Traffic (Ships/Day) | 178 Vessels | <10 Vessels | 95% Volume Reduction |

| DFC Reinsurance Capacity | N/A | $40 Billion (Revolving) | New Sovereign Backstop |

| Subsea Cable Traffic Dependency | 97% of Europe-Asia Flow | High Sabotage Risk | Critical Vulnerability |

Analysis of Competing Hypotheses: Post-Conflict Financial Recovery

- Hypothesis A: Systemic Fragmentation (65% Probability): The use of sovereign backstops and the expansion of the rahbar sanctions create a permanent bifurcation of global finance, where BRICS+ nations develop an entirely separate settlement and insurance architecture(https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/).

- Hypothesis B: Strategic Reconvergence (35% Probability): Following the resolution of the 2026 Iran war, the DFC facility is phased out and private insurers return as IMEC infrastructure is rebuilt under a new regional security framework(https://www.atlanticcouncil.org/wp-content/uploads/2025/08/The-India-Middle-East-Europe-Economic-Corridor-Connectivity-in-an-era-of-geopolitical-uncertainty.pdf).

Operation Epic Fury – Strait of Hormuz / Iran, Indo-Mediterranean Region

| Metric | Value / Status |

|---|---|

| Chapter | Chapter 1: The Kinetic Fracture of the Indo-Mediterranean Logic |

| Escalation Start Date | February 28, 2026 |

| Strategic Effect | Strategic dissolution of the Indo-Mediterranean connectivity paradigm |

| Conflict Characterization | “Kinetic Fracture”; transition from theoretical trade architecture to active theater of Non-Linear Warfare |

| IMEC Effect | Operational assumptions of the India-Middle East-Europe Economic Corridor (IMEC) effectively nullified |

| Opening Phase | U.S.-Israeli decapitation strikes across Tehran, Isfahan, Qom, Tabriz, Karaj, and Bushehr |

| Target Set | Core command-and-control nodes of the Islamic Republic of Iran |

| Iranian Retaliation | Immediate retaliatory closure of the Strait of Hormuz by the Islamic Revolutionary Guard Corps (IRGC) |

| Operation Designation | Operation Epic Fury |

| Phase One Date | March 2, 2026 |

| Phase One Objective | Systematic targeting of IRGC Navy small-craft swarm staging areas and coastal anti-ship missile batteries |

| U.S. Assets Deployed | A-10 Warthog aircraft; AH-64 Apache helicopters |

| CENTCOM Objective | Eliminate close-range sea-denial networks |

| USS Santa Barbara Role | Littoral Combat Ship successfully employed improvised LUCAS one-way attack drones |

| Iranian Mine-Laying Vessels Disabled | 16 Iranian mine-laying vessels near the Strait by March 10, 2026 |

| Iranian Remaining Capability | IRGC maintained a “stranglehold” on the waterway |

| Iranian Tools | Deep-water mines; land-based ballistic assets |

| Commercial Transit Reduction | 95% reduction in commercial transit |

| Source Links | https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis • https://besacenter.org/avoiding-the-knife-fight-defeating-irans-strait-strategy/ • https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/ |

Skylight Tanker Incident – North of Khasab, Oman

| Metric | Value / Status |

|---|---|

| Incident Date | March 1, 2026 |

| Vessel | Oil tanker Skylight |

| Location | North of Khasab, Oman |

| Attack Type | Struck by a projectile |

| Casualties | Death of two Indian crew members |

| Strategic Meaning | Verified the high-risk environment |

| Source Link | https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis |

MKD VYOM Incident – Strait of Hormuz Theater, Persian Gulf / Oman Region

| Metric | Value / Status |

|---|---|

| Vessel | MKD VYOM |

| Incident Type | Drone boat strike |

| Damage | Engine room explosion |

| Crew Impact | Evacuation of its 21-person crew |

| Strategic Meaning | Confirmed Iranian “asymmetric maritime doctrine” pivoted from regional deterrence to total economic denial |

| IMEC Effect | Seaborne leg between India and the UAE rendered functionally extinct |

| Source Link | https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis |

Dual Blockade Architecture – Persian Gulf to Gulf of Oman, Iran / U.S.-Led Maritime Theater

| Metric | Value / Status |

|---|---|

| Evolution Date | April 13, 2026 |

| Structure | “Dual Blockade” |

| Iranian Role | Iran interdicted the Strait |

| U.S. Navy Role | Imposed a total blockade on all Iranian ports |

| Blockade Geography | Coastline from the Persian Gulf to the Gulf of Oman |

| Presidential Direction | President Donald Trump directed CENTCOM and the U.S. State Department to form the Maritime Freedom Construct |

| Maritime Freedom Construct Purpose | New international coalition intended to restore navigation by sharing real-time intelligence |

| Enforcement Doctrine | “Belligerent right to visit and search” for all vessels suspected of violating sanctions |

| Commercial Vessels Turned Around / Returned | 44 commercial vessels as of April 30, 2026 |

| Source Links | https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis • https://investinglive.com/commodities/a-desperate-trump-pitches-maritime-freedom-construct-coalition-to-reopen-strait-of-hormuz-20260430/ • https://www.chasetactical.com/uncategorized/centcom-briefs-white-house-on-iran-strike-options-as-us-launches-hormuz-coalition |

M/T Stream Interdiction – U.S.-Led Blockade, Persian Gulf

| Metric | Value / Status |

|---|---|

| Vessel | M/T Stream |

| Interdiction Date | April 26, 2026 |

| Interdicting Vessel | Guided-missile destroyer USS Rafael Peralta |

| Context | U.S.-led blockade rules of engagement |

| Source Link | https://www.jpost.com/middle-east/iran-news/article-893895 |

Touska Tanker Interdiction – Kharg Island / Persian Gulf, Iran

| Metric | Value / Status |

|---|---|

| Vessel | Iranian-flagged tanker Touska |

| Interdiction Date | April 19, 2026 |

| Status | Disabled and boarded |

| Cargo | 2 million barrels of oil from Kharg Island |

| Strategic Effect | Part of U.S.-led interdiction denying Iranian regime estimated $5 billion in oil revenue |

| Immobilized Tankers | 31 tankers |

| Immobilized Oil Volume | 53 million barrels of crude oil |

| Source Links | https://www.jpost.com/middle-east/iran-news/article-893895 • https://m.economictimes.com/news/defence/how-long-before-iran-breaks-under-crushing-us-pressure/articleshow/130719980.cms |

Operation Economic Fury – Iran Shadow Banking Network, Global Financial System

| Metric | Value / Status |

|---|---|

| Operation Date | April 28, 2026 |

| Lead Agency | U.S. Department of the Treasury |

| Office | Office of Foreign Assets Control (OFAC) |

| Designated Parties | 35 entities and individuals |

| Targeted Architecture | Iran’s “Shadow Banking” architecture |

| Financial Function | Movement of tens of billions of dollars for the IRGC and Iran’s Armed Forces General Staff (AFGS) |

| Network Type | Rahbar companies—private intermediaries managing thousands of shell firms |

| Shell Firm Jurisdictions | United Kingdom; UAE; Marshall Islands |

| Purpose | Launder illicit oil proceeds |

| Enforcement Authority | Executive Order 13902 |

| EO 13902 Scope | Sanctions on any person operating in Iran’s financial, petroleum, or construction sectors |

| Additional Treasury Warning | “Teapot Alert” warning global financial institutions of risks associated with independent refineries in Shandong Province, China |

| Source Links | https://home.treasury.gov/news/press-releases/sb0477 • https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735 |

Farab Soroush Afagh Qeshm Company – Qeshm / Iran Shadow Banking Network

| Metric | Value / Status |

|---|---|

| Abbreviation | FSAQ |

| Role | Primary rahbar for Shahr Bank |

| Function | Coordinating with exchange houses to facilitate payments |

| Beneficiaries | AFGS; National Iranian Oil Company (NIOC); IRGC |

| Foreign Front Company | UK-based Shuqun LTD |

| Shuqun LTD Activity | Through 2024 transferred over $70 million worth of payments for Iranian crude oil and oil distillates on behalf of the NIOC |

| Source Link | https://home.treasury.gov/news/press-releases/sb0477 |

HMS Trading FZE – UAE-Based Entity, United Arab Emirates

| Metric | Value / Status |

|---|---|

| Location | UAE-based entity |

| Role | Acting on behalf of Shahr Bank |

| Function | Finance and guarantee oil shipments for sanctioned Iranian state producers |

| Source Link | https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735 |

Nikan Pezhvak Aria Kish Company – Bank Melli Rahbar Network, Iran

| Metric | Value / Status |

|---|---|

| Role | Rahbar for Bank Melli |

| Function | Processing transactions for the IRGC |

| Additional Beneficiary | Central Bank of Iran |

| Front Company | Fratello Carbone Trading Limited |

| Front Company Transfer | Over $20 million for the NIOC |

| Source Links | https://uk.investing.com/news/economy-news/us-treasury-sanctions-35-entities-in-iran-shadow-banking-crackdown-93CH-4634735 • https://home.treasury.gov/news/press-releases/sb0477 |

Hengli Petrochemical (Dalian) Refinery – Dalian, China

| Metric | Value / Status |

|---|---|

| Entity Type | Chinese “teapot” refinery |

| Sanction Date | April 24, 2026 |

| Sanctions Reason | Purchasing billions of dollars in Iranian oil |

| Systemic Role | Acting as a liquidity vent for the sanctioned shadow fleet |

| Source Link | https://www.jpost.com/middle-east/iran-news/article-894522 |

IMEC / Ghost Corridor – India-Middle East-Europe, Indo-Mediterranean Region

| Metric | Value / Status |

|---|---|

| Status | Rendered “obsolete” as a commercial prospect |

| Former Logic | Predicated on the Abraham Accords and a normalized Middle East |

| Current Description | “Ghost Corridor” |

| Infrastructure Gap | Estimated at $5 billion |

| Gap Components | Unbuilt rail segments in Jordan and Israel; logistics hubs in Haradh and al-Haditha |

| Private Capital Status | Withdrawal of private capital |

| Marine Insurance Policies Cancelled | Approximately 329 vessels in the Gulf |

| DFC Response | $40 billion sovereign reinsurance facility |

| Source Links | https://www.atlanticcouncil.org/wp-content/uploads/2025/08/The-India-Middle-East-Europe-Economic-Corridor-Connectivity-in-an-era-of-geopolitical-uncertainty.pdf • https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/ |

Chabahar Port / IPGL – Chabahar, Iran

| Metric | Value / Status |

|---|---|

| U.S. State Department Action Date | September 16, 2025 |

| Action | Revoked the sanctions exception for India’s Chabahar Port |

| Intended Function | Hub for the INSTC |

| Redundancy Role | Critical redundancy for Indian west-coast trade |

| Temporary Waiver | Extended until April 26, 2026 |

| Trump Administration Position | Refusal to renew it |

| IPGL Response | Consider “temporary divestment” and stake transfers to Iranian entities to avoid secondary sanctions |

| Source Links | https://www.mea.gov.in/rajya-sabha.htm?dtl/40929/QUESTION+NO+3132+SAFEGUARDING+INDIAS+INTERESTS+AT+CHABAHAR+PORT+IN+IRAN • https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/ |

Northern Corridor Rail Link – Israel and Jordan, Levant

| Metric | Value / Status |

|---|---|

| Corridor Description | “Northern Corridor” rail link through Israel and Jordan |

| Current Status | “Geopolitical fault line” |

| Shipping Giants Action | Suspended calls at Haifa and Ashdod |

| Lloyd’s JWC Action | Expanded “High-Risk” designation to include all ports with U.S. military presence |

| Source Note | Gulf conflict – Lloyd’s Market Association – May 2026 |

| War-Risk Premium Surge | 20-fold |

| Annual Cost for $1 Million Coverage | Rising from $1,000 to $120,000 as of May 2, 2026 |

| Source Link | https://www.arabianbusiness.com/business/healthcare/war-insurance-premiums-in-gulf-surge-by-20x-since-start-of-conflict |

Silicon Straits / Subsea Cable Risk – Strait of Hormuz, Europe-Asia Digital Route

| Metric | Value / Status |

|---|---|

| Digital Chokepoint | Strait of Hormuz |

| Traffic Dependency | More than 97% of global internet traffic between Europe and Asia via fiber-optic cables |

| Vulnerable Systems | Falcon; AAE-1; TGN-Gulf; SEA-ME-WE |

| Warning Source | Iran’s Tasnim News Agency |

| Warning Phrase | “Simultaneous damage to several major cables… could trigger severe outages across the Persian Gulf” |

| India DoT Emergency Meetings | March 27, 2026 |

| Repair Time | Minimum of 40 days |

| Repair Cost | Up to $3 million per incident |

| Constraint | Lack of access rights in contested territorial waters |

| Regional Response | Saudi Arabia, the UAE, and Qatar forming an international consortium to build land-based terrestrial fiber routes to bypass the Strait entirely |

| Source Links | https://subtelforum.com/iran-war-sparks-subsea-cable-disruption-fears/ • https://www.jpost.com/defense-and-tech/article-893954 • https://www.stimson.org/2026/beneath-the-strait-iran-could-threaten-gulf-data-centers-undersea-cables/ |

METRIC ANALYSIS: OPERATION ECONOMIC FURY IMPACT – May 2026, Indo-Mediterranean / Gulf Region

| Metric | Value / Status |

|---|---|

| Iranian Oil Revenue Monthly | Pre-Escalation Baseline: $2.5 Billion; Current Status: <$100 Million; Systemic Impact Delta: -96% Revenue Denial |

| Hormuz Commercial Traffic | Pre-Escalation Baseline: 178 Vessels/Day; Current Status: <9 Vessels/Day; Systemic Impact Delta: 95% Volume Reduction |

| War-Risk Insurance Premium | Pre-Escalation Baseline: 0.25% of Hull Value; Current Status: 3.00% – 10.00% of Hull Value; Systemic Impact Delta: 12x – 40x Increase |

| Shadow Banking Entities Sanctioned | Pre-Escalation Baseline: 150 (Cumulative); Current Status: 1,000+ (Post-Feb 2025); Systemic Impact Delta: 560% Surge in OFAC Designations |

| Global Data Latency Risk | Pre-Escalation Baseline: Managed Buffer; Current Status: Critical Outage Threat; Systemic Impact Delta: 97% Dependency Exposure |

Maritime Freedom Construct Scenario Analysis – Strait of Hormuz, U.S.-Iran Conflict

| Metric | Value / Status |

|---|---|

| Scenario 1 | Success of MFC Reopening |

| Scenario 1 Probability | 35% Probability |

| Scenario 1 Dependency | Depends on a Pakistan-brokered peace deal and Iranian leadership stability following the Ali Khamenei assassination |

| Scenario 1 Source | https://europeantimes.org/india-eu-summit-2026-the-mother-of-all-deals/ |

| Scenario 2 | Extended Dual Blockade |

| Scenario 2 Probability | 65% Probability |

| Scenario 2 Forecast | Forecasted until Late 2026 |

| Scenario 2 Rationale | President Trump rejects nuclear talk proposals and maintains “Maximum Pressure” via the U.S. Navy |

| Scenario 2 Source | https://investinglive.com/commodities/a-desperate-trump-pitches-maritime-freedom-construct-coalition-to-reopen-strait-of-hormuz-20260430/ |

INSTC – India-Iran-Russia / Greater Eurasia

| Metric | Value / Status |

|---|---|

| Chapter | Chapter 2: Continental Resilience and the INSTC Integration |

| Framework | “Greater Eurasia” connectivity framework |

| Core Corridor | International North-South Transport Corridor (INSTC) |

| Corridor Length | 7,200-kilometer multi-modal network |

| Original Establishment | September 2000 |

| Strategic Transition | From underutilized logistics project into primary, sanctions-resistant trade architecture |

| Linkage | India, Iran, and Russia with Central Asia and the European Union |

| Contrast With IMEC | Unlike IMEC, which required U.S.-guaranteed maritime security and regional normalization |

| INSTC Geographic Logic | Continental landmasses and protected waters of the Caspian Sea |

| Transit Time Advantage | 30% to 40% reduction in transit times compared to traditional Suez Canal route |

| Bypassed Volatility | Strait of Hormuz and Red Sea |

| Source Links | https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade • https://russiaspivottoasia.com/new-instc-russia-azerbaijan-iran-deal-is-hugely-significant-analysis/ |

INSTC Western Route – Russia-Azerbaijan-Iran, Eurasia

| Metric | Value / Status |

|---|---|

| Route Focus | Intensive capacity scaling |

| Route Design | Seamless rail and road connection from the Russian Federation through Azerbaijan to Iranian ports on the Persian Gulf |

| Trilateral MoU Date | November 25, 2025 |

| MoU Function | Established a Unified Tariff regime for rail freight |

| MoU Effect | Eliminating price gaps that historically hindered corridor competitiveness |

| e-CMR Roadmap Date | April 16, 2026 |

| Signatories | Deputy Prime Minister Shahin Mustafayev of Azerbaijan; Russian Deputy Prime Minister Alexey Overchuk |

| e-CMR Purpose | Implementation of electronic international consignment note system |

| e-CMR Goal | Digitalizing customs procedures and reducing border processing times for road transport |

| Current Annual Freight Reliance | Majority of 5.4 million tons of annual freight currently relies on highway transit |

| End-State Transit | Uninterrupted rail transit from St. Petersburg to Bandar Abbas |

| Transit Time Reduction | Indian imports to Russia from 45 days to approximately 18 days |

| Source Links | https://worldandnewworld.com/instc-trade-corridor-eurasian-routes/ • https://azertag.az/en/xeber/azerbaijan_and_russia_sign_roadmap_on_facilitating_e_cmr_in_road_transport-4130063 • https://report.az/en/infrastructure/azerbaijan-russia-sign-roadmap-on-e-cmr-implementation • https://www.grc.net/single-commentary/302 |

Horadiz-Aghband Railway – Zangilan District, Azerbaijan

| Metric | Value / Status |

|---|---|

| Project | Horadiz-Aghband railway |

| Physical Role | Backbone of Western Route |

| Location | Zangilan district |

| Completion Status as of May 3, 2026 | 75% complete |

| Works Status | Track-laying and tunneling works substantially finished |

| Commissioning Target | Advancing toward commissioning by the end of 2026 |

| Conflicting Completion Note | Vice PM: Azerbaijan’s Horadiz-Aghband railway set for completion by 2028 – Caliber.az – April 2026 |

| Route Length | 140-kilometer line |

| Initial Design Capacity | 15 million tons per year |

| Strategic Function | “Pivotal artery” connecting mainland Azerbaijan with Nakhchivan exclave and eventually with Turkey via the Zangezur Corridor |

| Source Link | https://caucasusbusinessjournal.com/news/azerbaijans-horadiz-aghband-railway-nears-completion-set-carry-15-million-tons |

Rasht-Astara Railway Link – Iran, INSTC Western Route

| Metric | Value / Status |

|---|---|

| Project | Rasht-Astara railway link |

| Length | 162 kilometers |

| Country | Iran |

| Funding | Funded jointly by Moscow and Tehran |

| Funding Agreement Date | May 2023 |

| Expected Completion | 2027 |

| Russian Ministry of Transport Report Date | March 20, 2026 |

| Reported Status | Geological surveys are finalized and construction has intensified |

| Strategic Reason for Intensification | Mitigate impact of the Strait of Hormuz blockade |

| Source Link | https://english.news.cn/20260320/992a0c35c14d4b85987a6aaa9008be21/c.html |

INSTC Eastern Route / KTI – Kazakhstan-Turkmenistan-Iran, Central Asia

| Metric | Value / Status |

|---|---|

| Route | Eastern Route |

| Transit Countries | Kazakhstan; Turkmenistan; Uzbekistan |

| Operational Status | Most operationally relevant branch of the INSTC as of early 2026 |

| 2024 Freight Volume | Rose by 19% to reach 26.9 million tons |

| Supporting Roadmap | Trilateral roadmap between Kazakhstan, Iran, and Turkmenistan |

| Throughput Target 2027 | 15 million tons |

| Throughput Target 2030 | 20 million tons |

| KTI Role | Anchor for the Eastern Route |

| Tariff Mechanism | Unified container-kilometer rate |

| Tariff Discounts | 15% to 80% |

| Discount Extension | Extended through the end of 2026 |

| Container Traffic 2025 | Doubling of container traffic |

| Landmark Delivery | 62 containers from Moscow to Iran via Central Asian branch in November 2025 |

| Food Security Role | India has utilized the corridor to send over 4 million tons of food aid to Afghanistan since 2018 |

| Pakistan Bypass | Circumventing transit denial of Pakistan |

| Source Links | https://timesca.com/kazakhstan-iran-turkmenistan-and-russia-to-develop-north-south-transport-corridor/ • https://ridl.io/russia-s-pivot-to-the-eastern-route-balancing-azerbaijan-with-kazakhstan-and-turkmenistan/ • https://worldandnewworld.com/instc-trade-corridor-eurasian-routes/ • https://gcaptain.com/india-mulls-options-on-iran-port-stake-before-sanctions-kick-in/ |

Kazakhstan Rail Expansion – Kazakhstan, Central Asia

| Metric | Value / Status |

|---|---|

| Announcement Date | April 24, 2026 |

| Announcer | Kazakh Prime Minister Olzhas Bektenov |

| Program | Massive infrastructure expansion program |

| Planned New Railway Lines | 5,000 kilometers |

| Timeframe | Over the next four years |

| Strategic Position | Kazakhstan’s position as handler of 85% of land-based Eurasian transit |

| TezCustoms Effect | Reduced border processing times from 8 hours to just 30 minutes for Chinese-origin transit |

| Source Links | https://daryo.uz/en/2026/04/24/kazakhstan-to-build-5000-km-of-new-railways-in-four-years-to-expand-rail-capacity/ • https://astanatimes.com/2026/04/kazakhstan-expands-rail-network-and-transit-corridors-to-strengthen-eurasian-connectivity/ |

Aktau and Kuryk Ports – Caspian Sea, Kazakhstan

| Metric | Value / Status |

|---|---|

| Ports | Aktau and Kuryk |

| Upgrade Status | Undergoing rapid upgrades |

| Current Capacity | 80,000 TEU |

| Target Capacity | 300,000 TEU per year by 2029 |

| Source Link | https://astanatimes.com/2026/04/kazakhstan-expands-rail-network-and-transit-corridors-to-strengthen-eurasian-connectivity/ |

Turkmenbashi International Seaport – Turkmenbashi, Turkmenistan

| Metric | Value / Status |

|---|---|

| Port | Turkmenbashi International Seaport |

| Cargo Trend | Steady increase in cargo flows |

| Cargo Handling | 2.3 million tons in the first half of 2025 |

| Source Link | https://qazinform.com/news/turkmenistan-calls-for-expanding-international-transport-corridors-5e5b44 |

SPFS / SEPAM Treaty Integration – Russia and Iran, Eurasian Financial Architecture

| Metric | Value / Status |

|---|---|

| Architecture | Sanction-proof “Financial Shell” |

| Treaty | Comprehensive Strategic Partnership Treaty between Russia and Iran |

| Treaty Entry Into Force | October 2, 2025 |

| Legal Framework | Integrating national financial messaging systems—SPFS and SEPAM |

| Settlement Effect | Trade settlements in local currencies |

| Bypass Target | SWIFT network and U.S. Dollar-based clearing |

| EDB Projection Date | January 2026 |

| EDB Projection | Digital and financial “seamlessness” could unlock additional 40% in container traffic potential |

| TEU Equivalent | 127,000–246,000 TEU |

| India Export Goal | Scale exports to Russia and Central Asia to a projected $180 billion |

| Source Links | https://mid.ru/en/foreign_policy/news/2050909/ • https://www.aa.com.tr/en/world/russia-pursues-alternative-financial-logistical-methods-to-bypass-western-sanctions/3834631 • https://eabr.org/en/analytics/special-reports/the-international-north-south-transport-corridor-promoting-eurasia-s-intra-and-transcontinental-conn/ • https://www.researchgate.net/publication/401692665_International_North-South_Transport_Corridor_Geopolitical_Implications_and_the_Future_of_European_Trade |

TITR Digitalization Work Plan – Astana, Kazakhstan

| Metric | Value / Status |

|---|---|

| Route | Trans-Caspian International Transport Route (TITR) |

| Work Plan Approval Date | April 24, 2026 |

| Approval Location | Astana |

| Mandate | Implementation of electronic document management using digital signatures for all participating countries |

| Expected Effect | Further reduce transit times |

| Long-Term Target | 10 days between China and Europe |

| Source Link | https://timesca.com/middle-corridor-countries-approve-2026-plan-focus-on-digitalization-and-container-growth/ |

METRIC ANALYSIS: INSTC CAPACITY SCALING – May 2026, Eurasia

| Metric | Value / Status |

|---|---|

| Western Route AZE | Route Milestone: Horadiz-Aghband Rail; Current Throughput: 5.4 Million Tons (Road); Target Throughput: 15.0 Million Tons (Rail); Status: 75% Complete |

| Eastern Route KTI | Route Milestone: KTI Rail Corridor; Current Throughput: 1.8-2.0 Million Tons; Target Throughput: 15.0 Million Tons (2027); Status: Operational/Active |

| Central Route Caspian | Route Milestone: Aktau/Kuryk Port; Current Throughput: 80,000 TEU; Target Throughput: 300,000 TEU (2029); Status: Expansion Ongoing |

| Unified Tariff Agreement | Route Milestone: Nov 2025 MOU; Current Throughput: N/A; Target Throughput: Predictable Pricing; Status: Implemented |

| Digital Integration | Route Milestone: e-CMR Roadmap; Current Throughput: April 2026 Signing; Target Throughput: Seamless Customs; Status: In Progress |

INSTC Sustainability Drivers – Greater Eurasia, Continental Trade System

| Metric | Value / Status |

|---|---|

| Hypothesis A | Continental Dominance |

| Hypothesis A Probability | 70% Probability |

| Hypothesis A Rationale | Sustained maritime disruption in Hormuz and the Red Sea makes the INSTC the only viable path for India-EU-Russia trade, driving massive sovereign investment through 2030 |

| Hypothesis A Source | https://www.grc.net/single-commentary/302 |

| Hypothesis B | Sanctions Atrophy |

| Hypothesis B Probability | 30% Probability |

| Hypothesis B Rationale | Expansion of U.S. OFAC secondary sanctions to Central Asian rail operators and banks creates a “Financial Chokepoint” that slows the INSTC’s operational growth despite physical infrastructure completion |

| Hypothesis B Source | https://home.treasury.gov/news/press-releases/sb0477 |

| Additional Source | https://debuglies.com/2025/07/07/brics-as-a-geopolitical-counterweight/ |

Financial Interdiction and Cyber-Digital Frontier – Middle East / Eurasia, Global System

| Metric | Value / Status |

|---|---|

| Chapter | Chapter 3: Financial Interdiction and the Cyber-Digital Frontier |

| Warfare Apex | “Total Financial and Digital Attrition” |

| Strategic Context | Current apex of Non-Linear Warfare in the Middle East |

| Trigger Context | Following operational failure of IMEC |

| U.S. / Allied Strategy | Multi-vector strategy centered on interdiction of sovereign capital flows and neutralization of digital infrastructure |

| Digital Infrastructure Function | Underpins the Eurasian data economy |

| Primary Operation | Operation Economic Fury |

| Operation Type | Joint regulatory and military offensive |

| Objectives | Decouple the Islamic Republic of Iran’s military apparatus from international financial system; secure critical digital gateways against state-sponsored sabotage |

Rahbar Shadow Banking Network – Iran / UK / UAE / Marshall Islands

| Metric | Value / Status |

|---|---|

| Formalization Date | April 28, 2026 |

| OFAC Action | Designation of 35 entities and individuals |

| Network Name | Rahbar system |

| Method | Private companies as financial intermediaries |

| Shell Companies | Thousands of shell companies |

| Jurisdictions | United Kingdom; United Arab Emirates; Marshall Islands |