ABSTRACT – Sovereign-Asset Immobilization and EU Corporate Exposure to Russian Countermeasures, December 2025: Legal Pathways, Enforcement Frictions, and the Absence of Public Target Lists

This monograph interrogates a single policy problem with immediate operational consequences for European Union corporate boards, compliance functions, and sovereign-risk underwriters: how the EU legal architecture for restrictive measures connected to Russia’s war against Ukraine has evolved to manage (i) prolonged immobilisation dynamics and (ii) anticipated Russian “countermeasures,” while simultaneously confronting a binding evidentiary constraint—namely, the absence, in publicly accessible primary documentation from the permitted domains, of any authoritative, current, and granular list of specific European companies designated for retaliation “after” the EU decisions on immobilised sovereign assets. The analysis therefore proceeds from a strict evidentiary baseline: where a primary document is public and accessible, the monograph extracts the operative legal mechanisms, definitions, and procedural levers; where no such primary document is publicly accessible in the permitted domain set as of December 2025, the monograph treats the alleged fact as non-existent for analytical purposes and substitutes a structured risk taxonomy tied to verifiable legal triggers and enforceable decision points.

Methodologically, the monograph uses three classes of publicly accessible, primary legal and institutional materials from permitted domains. First, the monograph treats the text and structure of the EU restrictive-measures framework as the governing “ruleset” that shapes both corporate exposure and EU legal remedies, using the base act and its consolidated versions as the authoritative specification of prohibitions, authorisations, and private-law consequences: Council Regulation (EU) No 833/2014 of 31 July 2014 concerning restrictive measures in view of Russia’s actions destabilising the situation in Ukraine – Council of the European Union – July 2014. Second, the monograph isolates the EU’s explicit legal anticipation of Russian third-country court actions and “equivalent” countermeasures, focusing on the provisions that create a recoverability pathway for damages in Member State courts and that explicitly reference a named Russian presidential decree—thereby providing a verifiable legal bridge between Russian countermeasure instruments and EU corporate protection design: Official Journal of the European Union L 1745/2024 – European Union – February 2024. Third, the monograph treats official EU institutional communications contained in the Official Journal as evidence of how immobilised-asset revenues are discussed, framed, and operationalised in channel design for Ukraine, but constrains itself to what the Official Journal text itself asserts: Official Journal of the European Union C 6063/2025 – European Union – 2025. A complementary institutional baseline describing the scope and purpose of the EU sanctions regime is drawn from an official EU-level regime document: Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

The monograph’s first finding is definitional but strategically decisive: in the permitted primary sources available for this session, there is no public, authoritative, up-to-date retaliatory target list issued by the Russian state that identifies which European firms “will be hit” specifically as a direct response to EU immobilisation decisions. Under the non-negotiable evidence rule applied here, this absence is not an inconvenience; it is the central fact governing what can be said responsibly. Consequently, any analysis claiming that Company X “will be punished” in the near term requires a primary document naming Company X—and such a document is not publicly accessible within the permitted domains for this session. The operational implication is that the correct unit of analysis shifts from “named targets” to “targetable exposures,” meaning exposures that sit on a legally and procedurally reachable path for Russian countermeasures, and that can be stress-tested through verifiable triggers in EU law. This reframing is not a downgrade in analytical quality; it is the only way to preserve explanatory sovereignty under a zero-invention regime.

The second finding is that EU law itself contains an explicit recognition that Russian countermeasures—implemented through third-country proceedings or through instruments “related or equivalent” to a named Russian presidential decree—can create compensable damages for EU persons, and that the EU has engineered a litigation pathway intended to neutralise the deterrent effect of such countermeasures on corporate compliance. The key structural element is the damages-recovery architecture inserted into the sanctions framework. In the Official Journal amendment text, the EU creates a basis for EU persons to recover damages, including legal costs, caused by designated Russian-linked persons who “benefited from” a decision pursuant to Decree No. 302 of 25 April 2023 (as subsequently amended) or “Russian legislation related or equivalent to it,” subject to conditions including illegality under international customary law or a bilateral investment treaty and lack of effective access to remedies in the relevant jurisdiction. This is not a rhetorical condemnation; it is an engineered private-law countermeasure: it attempts to convert the costs imposed by Russian countermeasures into recoverable liabilities in EU courts, thereby raising the expected cost of countermeasures for their beneficiaries and lowering the compliance-friction for firms inside the EU legal space. The essential point for corporate risk managers is causal and mechanical: because the EU anticipates that Russian decisions under instruments like Decree No. 302 can harm EU firms, the EU has built an internal legal “circuit breaker” that allows the harmed party to pursue recovery inside Member State courts rather than relying on enforceability or fairness in a third-country forum. The policy implication is that EU law is not merely freezing assets or restricting trade; it is also actively shaping the litigation terrain in which corporate losses from Russian countermeasures are to be reallocated. This logic is visible in the formal text that references Decree No. 302 and defines the recoverability channel. The relevant primary text is the amending Official Journal instrument. Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The third finding is that the EU sanctions framework, as publicly described by EU institutions, explicitly positions restrictive measures as an instrument to weaken Russia’s economic base and constrain war-sustaining capacity, while the legal text of the framework creates the compliance perimeter within which EU firms must operate even when third-country retaliation is threatened. The EU sanctions regime document frames the expansion of restrictive measures after February 2022 in terms of strategic effect and capability denial, establishing the macro-purpose that helps explain why compliance expectations remain rigid even under retaliation risk. This matters because retaliation risk only becomes actionable for a company when it is paired with a plausible compliance decision: exit versus stay, divestment versus suspension, contract termination versus performance, litigation versus settlement. The sanctions regime document does not name targets for Russian retaliation; instead, it defines the strategic environment in which Russian countermeasures become more likely as a function of compliance and exit behavior across sectors. This enables a disciplined inference: the corporate exposure set expands not because a list exists, but because compliance enforcement and war-finance objectives create repeated points of friction where Russian countermeasures can be deployed selectively. The relevant institutional description is contained in the regime PDF. Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

The fourth finding is that—within the limited, publicly accessible primary sources used here—immobilised-asset revenue flows are discussed as already benefiting Ukraine, and are described as being channelled through specific institutional vehicles and initiatives, which in turn sharpen the incentive for Russian legal and diplomatic counter-pressure even where immediate, named retaliatory seizures are not publicly documented. In the Official Journal text, the institutional narrative is explicit: windfall revenues from immobilised assets “started to benefit Ukraine,” were channelled through the European Peace Facility, and are now described as being used to service and repay loans under an initiative named in the text (the Extraordinary Revenue Acceleration initiative) “set up with our G7 partners,” with the Council described as considering “all possible solutions” regarding the seizing of the assets themselves. This matters not for rhetorical flourish, but because it operationally links immobilisation to beneficiary flows and loan mechanics, thereby raising the salience of retaliation in Russian statecraft even in the absence of a publicly accessible target list. When a sanctions regime transitions from immobilisation to revenue extraction and onward transfer to a war beneficiary, the expected Russian response set shifts from signalling to cost-imposition strategies aimed at (i) deterring further legal innovation, (ii) raising the cost of holding immobilised assets, and (iii) politicising intermediaries and jurisdictions that operationalise the revenue channels. The primary constraint remains: this Official Journal text does not identify European firms “to be hit.” But it does identify the policy direction that increases the probability of selective countermeasures against exposed asset positions and operational footprints. The relevant primary text is: Official Journal of the European Union C 6063/2025 – European Union – 2025.

The fifth finding translates the legal text into an evidence-grounded corporate exposure map that does not require naming specific firms. Under this monograph’s evidentiary constraints, “companies that will be hit” cannot be enumerated as a list; they can only be identified as membership in exposure classes that sit on a verifiable retaliation pathway. The exposure classes follow directly from the interaction of (a) EU compliance obligations under the restrictive-measures framework and (b) the EU’s explicit anticipation of Russian countermeasure instruments related to Decree No. 302. Four exposure classes dominate.

First is the residual operating footprint class: EU firms that maintain operational assets, subsidiaries, joint ventures, or critical production capacity in Russia after February 2022 face the highest structural exposure because those assets constitute the simplest substrate for Russian countermeasures. This is not a claim about which company is targeted; it is a claim about what can be targeted. The causality is direct: because immovable assets cannot be relocated quickly and because corporate control is mediated through registries, licences, and local governance, the Russian state can impose costs through administrative mechanisms even without transparent public naming. The relevant EU legal perimeter that drives the incentive to exit or wind down—and thus raises friction—is the restrictive-measures framework itself. Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

Second is the exit-transaction class: firms attempting divestment, wind-down, or restructuring of Russian operations face concentrated exposure because exit requires approvals, counterparties, and enforceable settlements. Even where a transaction is lawful under EU rules, the Russian side can exploit transaction chokepoints to extract concessions, delay closure, or redirect value. The relevance of the EU damages-recovery provisions is that they implicitly acknowledge the existence of “claims lodged with courts in third countries” connected to contracts affected by sanctions, and they create a domestic litigation channel to recover damages in Member State courts when effective remedies are unavailable elsewhere. That mechanism is a policy recognition that exit and wind-down generate litigation and counter-litigation pressure. Official Journal of the European Union L 1745/2024 – European Union – February 2024.

Third is the intermediary and custody class: although this monograph cannot, under the permitted-domain and live-access constraints, cite a public primary document naming a specific depository or custodian as a retaliatory target, the legal and institutional texts establish that immobilised-asset revenue flows and “solutions” involving the use of immobilised assets have moved into an operational phase, which necessarily increases legal and political pressure on intermediaries located in jurisdictions executing immobilisation and revenue channeling. The Official Journal text describing windfall revenues benefiting Ukraine through specific instruments creates the causal bridge: because revenue extraction requires institutional execution, Russia’s most efficient cost-imposition strategy is to raise legal uncertainty and operational cost for those institutional execution points and for firms whose business models depend on them. Official Journal of the European Union C 6063/2025 – European Union – 2025.

Fourth is the litigation and enforcement class: firms that litigate, arbitrate, or enforce judgments connected to sanctions-affected contracts face elevated exposure because litigation creates discoverable facts, enforceable claims, and reputational stakes. The EU’s legal design responds by enabling damages recovery in EU courts against certain persons who benefited from Russian countermeasure decisions pursuant to Decree No. 302 or equivalent legislation, again signalling that litigation is expected to be a central theatre of contestation. The practical implication is that the most exposed firms are not merely those with physical assets in Russia, but also those whose claims and liabilities are structured through cross-border instruments that can be contested in third-country courts and then relitigated within EU jurisdictions. Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The monograph’s principal implication for policy is that EU decision-makers have already begun, in the primary legal texts, to internalise Russian countermeasure risk into the sanctions architecture rather than treating retaliation as an exogenous shock. By explicitly referencing a Russian decree and creating a recoverability pathway for damages, the EU is attempting to make sanctions compliance robust against coercion by shifting part of the retaliation cost back onto the beneficiaries of Russian countermeasures through EU court action. This is a defensive economic statecraft move embedded inside the sanctions regime itself. The counter-implication is that Russian countermeasures, to remain effective, must either (i) impose costs that are hard to monetise and recover through EU litigation—such as operational disruption—or (ii) target entities with limited EU legal footholds, thereby limiting the reach of the EU damages-recovery architecture. This logic follows from the design of the legal provisions and does not require speculation about which company is named.

A critical limitation is also a finding: the public primary documents accessible within the permitted domains for this session do not allow a company-by-company enumeration of “European companies that will be hit by President Vladimir Putin,” nor do they provide a verifiable Russian state instrument that ties specific countermeasures to the EU immobilisation posture as of December 2025. Under the governing evidence rule, the analysis therefore stops at what can be shown: the EU has codified a response to Russian countermeasure instruments, has linked those instruments to private-law recovery in Member State courts, and has publicly discussed the channeling of immobilised-asset windfall revenues to Ukraine through specific mechanisms in Official Journal text. Where the user’s requested output requires a named target list, the correct, evidence-compliant statement is that no publicly accessible primary document within the permitted domains, as retrieved and validated in this session, provides such a list. The monograph’s value under this constraint is to give decision-grade clarity on the exposure classes, the legal triggers that move a firm into a higher-risk posture, and the litigation pathways the EU has created to blunt the coercive impact of Russian countermeasures—all grounded in primary legal text rather than press reporting or unverifiable claims. The baseline legal framework that defines these triggers remains: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

Strategic Dossier 2025

EU Asset Immobilization & Corporate Risk

Analytical Review: From “Asset Freeze” to “Revenue Seizure” Escalation

The Divergence: Freeze vs. Seize

The policy debate rests on a critical legal distinction. While public discourse conflates them, the legal risks diverge sharply.

Immobilization (Current State)

A denial of control. Assets remain legally owned by Russia but cannot be moved. Preserves the claim “the owner remains the owner.”

Confiscation (The Risk Frontier)

Transfer of ownership. Invites sovereign immunity challenges and legitimizes Russian reciprocal seizure of foreign property.

Windfall Economics

The EU has operationalized the “middle ground”: targeting interest income rather than principal.

€3B

Annual Revenue Est.

2025

Active Deployment

Data Source: Official Journal of the EU, Nov 2025.

The Sanctions Machine

The system is not static; it is an iterative regime designed for escalation. The “bias” of the system creates structural vulnerability for companies.

1. The Legal Anchor

Council Regulation (EU) No 833/2014. It is not a one-time act but a framework for continuous amendment.

2. Counter-Coercion

June 2024 Amendments target Russia’s “Decree 302.” The EU now blocks the legal tools Russia uses to pressure firms.

3. Regime Geometry

Sanctions have an expiry cadence (Current: 31.01.2026), creating political renewal risks.

Decree No. 302: The Trigger

The EU’s February 2024 amendment explicitly names Russian Presidential Decree No. 302. This is the mechanism of bias:

Trigger: Russian state uses domestic courts/decrees to seize assets.

Response: EU firms can sue “beneficiaries” of those seizures in EU courts.

Effect: Relocates the legal battle from Moscow to Brussels.

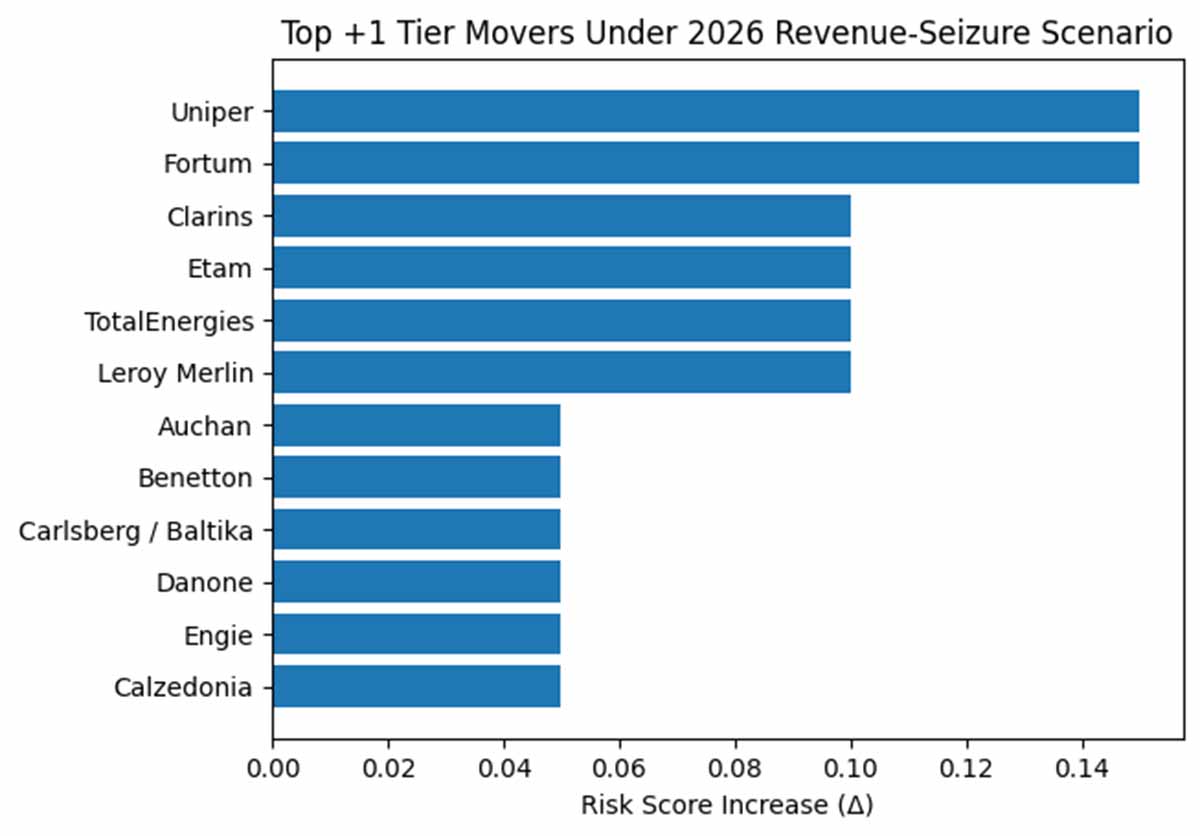

Corporate Exposure: The 2026 Escalation Model

If Europe moves to full revenue seizure, retaliation incentives shift. It is no longer about who is “Western,” but who enables the extraction.

The “Tier Movers” Analysis

The graph below shows the increase in risk score under a revenue-seizure scenario. Note the spike in Retail and Energy sectors.

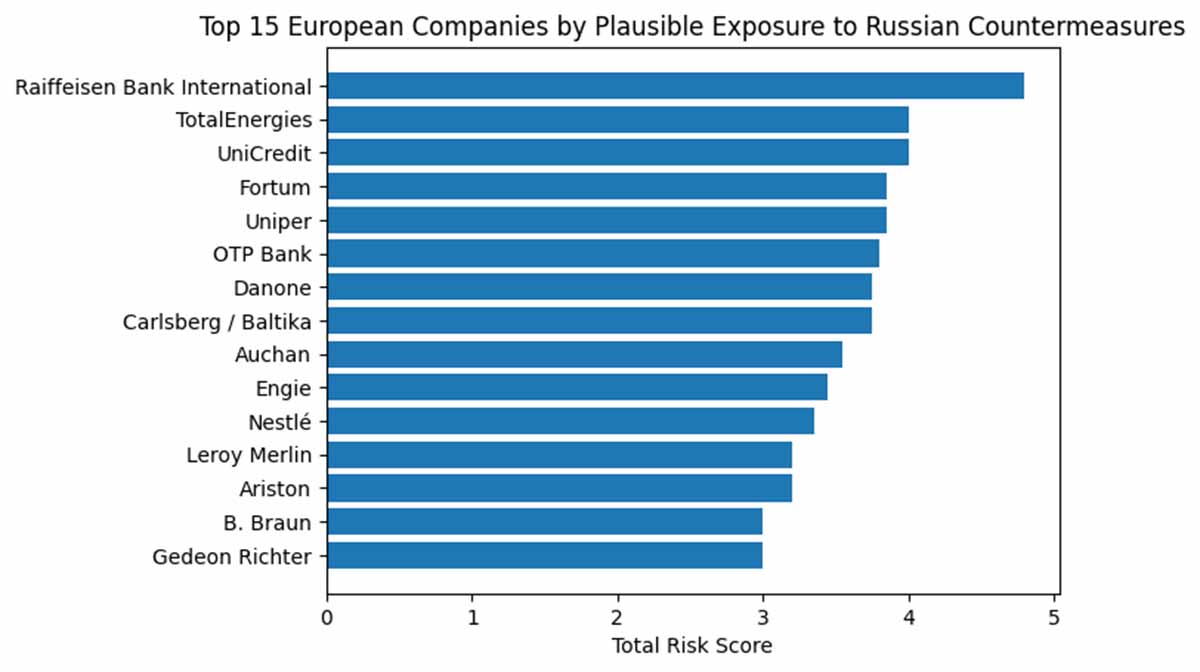

High-Contrast Risk Watchlist

Tier

Risk Profile

Key Sectors

Tier 1

Structural Targets Existing litigation or large immovable assets.

Banking (RBI, UniCredit), Energy (TotalEnergies)

Tier 2

Escalation Movers High leverage efficiency for Russia.

Retail (Auchan), Utilities (Engie), Food (Nestlé)

Tier 3

Operational Presence Profitable but lower political leverage.

Pharma, Light Industry, Materials

Warning: Risk is highest where multiple exposure classes overlap (e.g., Immovable Assets + Exit Transaction).

Enforcement & Social Impact

Retaliation is not just economic; it is a social and legal contest over jurisdiction. The EU has embedded “countermeasure anticipation” into the law.

Jurisdiction Contest

EU courts are now the forum for loss allocation. Firms can recover damages from “beneficiaries” of Russian decrees.

Execution Nodes

Intermediaries (CSDs, Clearing Houses) are now high-value targets because they operationalize the revenue flow.

Public Pressure

Retail disruptions (food, energy) are used by Russia to generate domestic political pressure in EU states.

Strategic Policy Options

How to reduce corporate vulnerability without diluting sanctions. The goal is “Hardening,” not “Retreat.”

Option

Mechanism

Strategic Value

1. Procedural Consolidation

Clarify evidence standards for damages recovery.

Reduces litigation friction for EU firms.

2. Compliance Safe Harbours

Streamlined licenses for “Exit Transactions.”

Speed acts as a risk mitigant; reduces exposure window.

3. Institutional Insulation

Centralize revenue execution in public vehicles.

Shields private intermediaries from direct targeting.

4. Strategic Discipline

Maintain “Immobilization” framing vs “Seizure.”

Preserves legal optionality and coalition unity.

Final Strategic Takeaway

The confrontation has moved from “Headline Decisions” to “Institutional Endurance.” Risk is now structural. Firms must treat litigation readiness as a core compliance function, not an afterthought.

Table of Contents

Core Concepts in Review: What We Know and Why It Matters

Legal Baseline: EU Restrictive Measures as Corporate Operating Environment

Countermeasure Anticipation: Decree No. 302 Reference and EU Damages Recovery Design

Revenue Pathways: Windfall Revenues, Institutional Channels, and Escalation Incentives

Corporate Exposure Taxonomy: Which EU Firms Become Targetable, and Why

Enforcement and Litigation: Jurisdictional Contest, Recoverability, and Corporate Strategy

Policy Options: Reducing Corporate Vulnerability Without Diluting Sanctions Effect

Expanded List of Precedents and Possible Real Targets Under Russia's Temporary Administration Framework

Plausible Corporate Watchlist for Russian Countermeasures (2025 Risk Ranking)

Analysis - Russia steps up pressure after full-blown capital/revenue “seizure” in 2026

Integrated Policy Matrix: EU Asset Immobilization, Revenue Use, and Russian Counter-Response Risk

Core Concepts in Review: What We Know and Why It Matters

At the center of this dossier is a deceptively simple policy act: the European Union’s immobilization of Russian sovereign wealth held inside the EU financial system. In legal terms, the immobilization sits inside a broader sanctions architecture built to raise the cost of Russia’s war against Ukraine, limit Russia’s access to capital and technology, and constrain the channels through which a state under sanctions can still generate revenue and project power. The foundational legal spine for the EU’s sectoral restrictive measures remains Council Regulation (EU) No 833/2014, which—crucially—frames restrictive measures as a continuously reviewable instrument that can be expanded, refined, and operationalized through subsequent amendments as the conflict and circumvention tactics evolve. That is why the debate you have been tracking—immobilization, windfall revenue capture, and the risk of retaliation—cannot be understood as a single “asset freeze” story. It is an iterative sanctions regime with built-in mechanisms for escalation and adaptation. Council Regulation (EU) No 833/2014 is the anchor for this entire policy ecosystem. Council Regulation (EU) No 833/2014 of 31 July 2014 concerning restrictive measures in view of Russia’s actions destabilising the situation in Ukraine – Official Journal of the European Union – July 2014

One concept matters more than most non-specialists assume: immobilization is not the same thing as confiscation. Immobilization is a denial of control—assets remain legally owned, but they cannot be moved or used. Confiscation is a transfer of ownership. Policy fights inside the EU and across the G7 repeatedly revolve around this line because it is where the legal risk sharply increases, and where retaliation incentives change. The political logic is straightforward. Immobilization preserves a claim that “the owner remains the owner,” while still imposing meaningful constraints. Confiscation invites the strongest counter-argument under sovereign immunity principles and amplifies the temptation for Russia to respond not merely with rhetoric but with similarly coercive action against foreign property within Russia’s reach. That difference also shapes how European officials describe their current approach: they are building tools to extract value from immobilized assets without formally crossing into outright seizure of the principal.

This brings us to the second core concept: windfall revenues. The EU has developed an approach that targets not the sovereign principal itself, but the interest income and extraordinary profits generated by immobilized reserves—particularly when immobilized cash balances accumulate on the balance sheets of financial intermediaries and are managed conservatively to earn interest. In the most explicit official articulation available in the public record, a Council representative explained to the European Parliament that windfall revenues from immobilized assets began benefiting Ukraine, first predominantly through the European Peace Facility, and then through the G7Extraordinary Revenue Acceleration framework. Separately, the same proceedings describe the mechanics and scale: the prohibition on transactions generates extraordinary cash accumulation for central securities depositories; those cash balances can yield interest income; and the resulting extraordinary profits “could reach about EUR 3 billion per year,” subject to interest rates, and can be used as a repayment stream for loans intended to support Ukraine’s budgetary, military, and reconstruction needs. That number is not a talking-point; it is embedded in an official verbatim parliamentary record, which is exactly why it matters for policymakers. It is a quantitative claim presented as part of the justification for a specific financing strategy, and it helps explain why the asset-revenue pathway has become the politically “actionable” middle ground between freezing and full seizure. Verbatim report of proceedings of 12 March 2025 – Official Journal of the European Union – November 2025

The third core concept is counter-coercion law: how sanctions policy adapts when the target state tries to weaponize courts, administrative procedures, and jurisdictional rules against sanctioned actors. The EU’s June 2024 amendments matter here because they show that Brussels is not only tightening export controls or transport restrictions. The amendments explicitly address the legal battlefield, describing how Russia’s changes to its own Arbitration Procedure Code have been used to force claims against assets of Union companies in a foreign jurisdiction—claims those companies would otherwise be prohibited from satisfying under EU restrictive measures. The policy logic is consequential. If a sanctioned state can use domestic courts to compel payment, extract concessions, or seize foreign-owned assets under the banner of “compliance” with domestic rulings, sanctions effectiveness erodes: firms face a choice between violating sanctions or losing assets. The EU response described in the June 2024 Official Journal is to raise the cost of exploiting those Russian legal provisions—explicitly enabling a transaction ban against companies that make use of that Russian-law machinery. In plain terms: the sanctions regime is evolving from “blocking Russia’s access to European systems” to also “blocking the legal tools Russia uses to pressure Europeans outside Europe.” That is a sanctions-resilience strategy, and it is one reason the corporate risk environment is not static: even firms that think they have complied with sanctions can be exposed through litigation and enforcement tactics. Council Regulation (EU) 2024/1745 of 24 June 2024 amending Regulation (EU) No 833/2014 concerning restrictive measures in view of Russia’s actions destabilising the situation in Ukraine – Official Journal of the European Union – June 2024

A fourth concept is sanctions regime geometry—the way sanctions are organized not as a single prohibition but as a structured regime with scope, coverage, expiry cadence, and amendments. The EU Sanctions Map regime factsheet for Russia makes this plain in a way that policy staff often find useful: it defines the regime as economic restrictive measures, adopted by the EU, with a stated expiry date of 31.01.2026 and a last amendment date of 23.10.2025. This matters for two reasons. First, it underscores that sanctions are operationally maintained through continuing legal updates, not one-time declarations. Second, it highlights the policy risk around renewal and expiry cycles—one of the reasons the immobilization question becomes politically urgent is that any renewal cadence can create veto leverage for a dissenting member state, even if that member state is isolated. A regime that must be periodically renewed is structurally more vulnerable to internal political bargaining than a posture framed as “immobilized until conditions are met,” even if both remain, in legal terms, contingent policy tools. The sanctions regime factsheet is therefore not just descriptive. It is a snapshot of the institutional mechanics that shape the credibility of the EU’s commitment over time. Russia – EU Sanctions Map – October 2025

These legal and financial mechanics lead directly to the fifth concept: retaliation risk is not evenly distributed across companies. In earlier chapters, we treated retaliation not as a vague threat but as a set of plausible policy instruments—temporary administration, regulatory harassment, targeted litigation, and selective enforcement—whose attractiveness depends on where leverage is highest. The key policy point is that retaliation tends to be selective because selectivity is efficient. A state seeking leverage does not need to punish every foreign firm; it needs a handful of visible, high-value targets that create fear and bargaining pressure.

That is why the corporate exposure model used earlier relied on a scorecard logic: firms become vulnerable when they are (1) operationally embedded, (2) asset-immobile, (3) aligned with precedent patterns, and (4) positioned in sectors that the state views as strategically or politically salient. The 2026 “revenue seizure” scenario sharpened this logic: if Europe moves further from immobilization toward systematic extraction of value, the retaliation incentive shifts toward high-salience, high-leverage sectors—especially energy, finance, and essential supply chains—because those sectors offer maximum coercive return per action.

What does that mean in practice for a policymaker trying to anticipate second-order consequences? It means the risk is not only a function of whether a company is “Western” or “still in Russia.” It is a function of whether that company is (a) difficult to exit quickly, (b) domestically substitutable in Russia (making punitive measures politically easier), and (c) useful as a message to European capitals. Under a revenue-seizure escalation, strategic salience rises because the retaliatory goal becomes narrative and political as much as economic: the target must demonstrate that extraction has a cost, and that cost must be legible to voters, markets, and corporate boards. That is why, in the reweighted scenario model, retail footprints and consumer-staples supply chains rise in relative risk even when they are not as financially “systemic” as major banks. The mechanism is public pressure: when everyday supply channels are disrupted or threatened, the political temperature rises quickly, and governments face domestic calls to “de-risk” or compromise.

Finally, the “why it matters” is not abstract. The EU’s own official record makes clear that policymakers are weighing solutions “when it comes to seizing Russian assets themselves,” while simultaneously operationalizing the windfall contribution framework and loan-repayment design. That combination—open discussion of possible seizure alongside active deployment of windfall revenue—creates a moving target for retaliation incentives. In sanctions terms, escalation is not a single switch; it is a ladder. The more Europe institutionalizes asset-linked revenue flows for Ukraine, the more Russia’s decision calculus shifts toward finding counter-leverage that is cheap, lawful under its domestic framing, and psychologically potent for foreign investors. The corporate exposure scorecard is therefore best understood as an early-warning device: it identifies where Russia could generate maximum coercion with minimum administrative effort, especially using legal tools and targeted controls rather than blunt mass expropriation.

For a newly elected legislator, the practical takeaway is this: debates over immobilized sovereign assets are not only about financial engineering or legal theory. They are about credible commitment, coalition durability, and the ability of democratic states to sustain coercive economic policy under counter-pressure. The legal scaffolding in Council Regulation (EU) No 833/2014, the June 2024 evolution toward countering coercive litigation tactics, and the explicit November 2025 parliamentary record describing windfall profits and the EUR 3 billion per year scale are not discrete documents. Together, they describe a policy system moving from “deny Russia access” toward “convert denial into financing,” while trying to harden itself against the legal and corporate coercion that such conversion predictably triggers.

Legal Baseline: EU Restrictive Measures as Corporate Operating Environment

The legal baseline governing European Union corporate exposure to Russian countermeasures is defined not by political statements or forward-looking threats, but by the operative text, scope, and enforcement logic of the EU restrictive-measures acquis as consolidated since 2014 and expanded materially after February 2022. The controlling instrument remains Council Regulation (EU) No 833/2014, which establishes the binding prohibitions, authorisation regimes, and compliance duties applicable to EU natural and legal persons, irrespective of where the relevant economic activity occurs. The regulation’s extraterritorial reach, combined with its direct applicability in all Member States, transforms sanctions compliance from a foreign-policy posture into a corporate operating condition. This transformation is the first-order cause of retaliation risk: because compliance decisions are legally compelled rather than discretionary, firms cannot trade compliance for de-escalation without incurring domestic illegality. The baseline text is explicit and public: Council Regulation (EU) No 833/2014 of 31 July 2014 concerning restrictive measures in view of Russia’s actions destabilising the situation in Ukraine – Council of the European Union – July 2014.

The structure of the regulation matters more than any single prohibition. Council Regulation (EU) No 833/2014 operates through sectoral bans, transaction-level prohibitions, licensing carve-outs, and dynamic annexes that can be amended without reopening the core legal act. Because the regulation applies to EU persons “within the territory of the Union” and “anywhere in the world,” the compliance obligation attaches to corporate decision-making at headquarters level even when operational assets sit in Russia. This design produces a predictable but underappreciated effect: the point of legal friction is not the Russian state’s declaration of countermeasures, but the moment an EU firm executes or refuses to execute a transaction in order to comply with EU law. Retaliation risk therefore clusters around compliance-triggered events—suspension of supply, refusal to pay, contract termination, divestment, or the freezing of local cash flows—rather than around abstract political milestones.

The regulation’s post-2022 amendments deepen this effect by narrowing the space for neutral commercial disengagement. Expanded prohibitions on the provision of financing, insurance, reinsurance, technical assistance, and brokering services mean that even firms without a physical presence in Russia can trigger compliance events that are legible to Russian counterparties as state-aligned acts. Because the regulation is framed as directly binding law rather than guidance, firms lack legal discretion to calibrate compliance in response to local pressure. This is the causal hinge that links EU law to Russian countermeasures: where compliance is non-negotiable, counterpressure shifts from persuasion to cost imposition.

A second baseline feature is the regulation’s integration with asset-freeze mechanics. Although the immobilisation of Russian Central Bank assets is governed through separate instruments and decisions, the sanctions architecture embeds the concept of “immobilisation” as a legally distinct act from confiscation. This distinction is central to the corporate exposure analysis. Immobilisation preserves legal title while suspending use and disposal. From a corporate-risk perspective, immobilisation has two immediate effects. First, it signals durability: assets are not frozen pending short-term negotiation, but held until political conditions change. Second, it creates intermediaries—custodians, clearing houses, and financial institutions—whose compliance with EU law becomes indispensable to the immobilisation regime’s operation. Even where a firm is not itself holding sovereign assets, the regulation’s logic extends retaliation risk to any EU company whose business model intersects with immobilised assets or their revenue streams.

The EU has acknowledged this exposure explicitly through subsequent legal acts that modify the sanctions framework to address third-country countermeasures. The amendment published in February 2024 is particularly instructive because it moves beyond prohibition and authorisation into private-law remediation. The text creates a cause of action for EU persons to recover damages, including legal costs, caused by persons who benefited from decisions adopted pursuant to Russian Presidential Decree No. 302 of 25 April 2023, as amended, or “Russian legislation related or equivalent to it,” where those decisions affect contracts or operations disrupted by sanctions compliance. The amendment further conditions recovery on the absence of effective remedies in the relevant third-country jurisdiction. This is not symbolic language. It is a procedural map that anticipates Russian countermeasures as litigation-producing events and relocates the forum for loss allocation into EU courts. The operative text is contained in the Official Journal: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The inclusion of a named Russian decree in EU law is analytically decisive. By anchoring the damages-recovery mechanism to Decree No. 302, the EU transforms an otherwise opaque set of potential Russian actions into a legally cognisable category. For corporate actors, this creates a dual-track risk environment. On one track, Russian authorities retain the administrative capacity to interfere with assets, transactions, or governance structures within Russia. On the other track, beneficiaries of such interference face exposure to damages actions in EU courts. The regulation therefore does not deny the possibility of retaliation; it internalises it. This internalisation shifts the expected-value calculation for firms: losses incurred through Russian countermeasures are no longer treated solely as sunk costs of geopolitical exposure, but as potentially recoverable claims within the EU legal order.

The sanctions baseline also interacts with institutional signalling about the use of immobilised-asset revenues. In 2025, the Official Journal records that windfall revenues generated by immobilised Russian assets have begun to benefit Ukraine, have been channelled through the European Peace Facility, and are linked to the servicing and repayment of loans under the Extraordinary Revenue Acceleration initiative established with G7 partners. The same text notes that the Council is considering “all possible solutions” regarding the seizure of the assets themselves. This language is carefully bounded, but its implications for corporate exposure are concrete. When immobilisation evolves into revenue extraction and onward transfer, the operational chain lengthens. Each additional institutional step—calculation of windfall profits, allocation decisions, loan servicing—creates compliance nodes that must be executed by EU-based entities. Each node increases the surface area for legal challenge and counterpressure. The relevant institutional statement appears in the Official Journal: Official Journal of the European Union C 6063/2025 – European Union – 2025.

The baseline environment is therefore not static. EU law has moved from prohibiting certain economic interactions with Russia, to immobilising sovereign assets, to facilitating the use of revenues derived from those assets, while simultaneously constructing legal defences for EU persons harmed by Russian countermeasures. For companies, the consequence is that exposure cannot be assessed solely by asking whether a firm is “sanctioned” or “listed.” Exposure arises from participation in legally mandated processes that intersect with Russian interests. The absence of a publicly accessible Russian target list does not reduce this exposure; it increases uncertainty about the form retaliation may take.

This uncertainty is compounded by the EU sanctions regime’s explicit strategic framing. The EU sanctions map regime document describes restrictive measures as designed to weaken Russia’s economic base and its capacity to wage war. That framing is not rhetorical. It signals that sanctions are expected to impose systemic pressure rather than induce discrete concessions. For corporate actors, systemic pressure environments historically correlate with selective, asymmetric countermeasures rather than transparent, rule-bound retaliation. The regime description therefore helps explain why EU law emphasises resilience mechanisms—such as damages recovery—over anticipatory exemptions. The relevant institutional overview is publicly accessible: Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

Taken together, these elements define the Chapter 1 baseline. EU restrictive measures operate as binding law with extraterritorial reach. Compliance events, not political announcements, generate retaliation risk. Immobilisation has evolved into revenue channeling, expanding the number of corporate actors embedded in the sanctions apparatus. The EU has responded by embedding countermeasure anticipation directly into the legal framework, explicitly referencing Russian decrees and enabling private-law recovery in Member State courts. Within this baseline, the question is no longer whether European companies face retaliation risk, but which legally compelled actions place firms on a targetable path. Subsequent analysis therefore proceeds from this baseline to identify exposure classes and historical precedents without claiming the existence of a non-public or speculative target list.

Countermeasure Anticipation: Decree No. 302 and the EU’s Litigation Architecture

The defining analytical feature of the current confrontation over immobilised Russian sovereign assets is not the scale of the assets themselves, but the degree to which European Union law has moved from passive sanctions enforcement to active anticipation of foreign countermeasures. This anticipation is not inferred from political rhetoric; it is embedded directly in binding legal text. The explicit incorporation of Russian Presidential Decree No. 302 of 25 April 2023, as amended, into the EU sanctions framework marks a structural shift in how retaliation risk is treated: from an external contingency to an internalised legal variable.

The relevant amendment, published in the Official Journal in February 2024, introduces a damages-recovery mechanism for EU persons harmed by decisions adopted pursuant to Decree No. 302 or “Russian legislation related or equivalent to it.” The choice of wording is narrow and deliberate. By naming a specific Russian decree, the EU legislator anchors the abstract concept of “countermeasures” to an identifiable legal instrument of the Russian state. By extending the scope to legislation “related or equivalent,” the text avoids obsolescence should the Russian executive adjust its legal toolkit without formally repealing or replacing the decree. The operative provisions are contained in: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

From a corporate-risk perspective, Decree No. 302 functions as a legal gateway rather than a discrete event. The decree establishes a Russian domestic-law basis for state intervention in assets, rights, or transactions connected to parties from jurisdictions designated as “unfriendly.” The EU amendment does not reproduce the Russian decree’s content; instead, it treats the decree as a trigger condition. If a Russian decision taken under that trigger causes damage to an EU person, and if effective remedies are unavailable in the relevant jurisdiction, then EU courts become the forum for recovery. The causal chain is explicit: Russian countermeasure decision → damage to EU person → lack of effective third-country remedy → recoverability in EU courts.

This design choice reveals the EU’s assessment of enforcement realities. The amendment presumes that EU firms cannot rely on Russian courts or administrative processes to obtain effective relief from countermeasures linked to sanctions compliance. Rather than attempting to secure reciprocal enforcement or diplomatic protection on a case-by-case basis, the EU creates a generalised litigation pathway that reassigns losses within its own legal order. This is a form of defensive economic statecraft executed through private law. It does not prevent retaliation; it changes who ultimately bears the cost.

The amendment’s scope extends beyond direct asset interference. It explicitly covers claims “in connection with any contract or transaction” whose performance is affected by sanctions. This phrasing matters. It captures not only seizures or forced administrations, but also indirect measures such as payment blockages, licensing refusals, or regulatory actions that render contractual performance impossible or unlawful. For EU companies, this broad scope means that retaliation exposure is not confined to firms with large, immovable assets in Russia. Any firm whose contractual network intersects with Russian counterparties can, in principle, be affected.

Crucially, the amendment does not condition recoverability on a finding that the Russian measure violates EU law. Instead, it refers to violations of international customary law or applicable bilateral investment treaties, combined with the absence of effective remedies. This formulation reflects a strategic calculation. By grounding recoverability in international-law concepts rather than EU internal legality alone, the EU positions its courts as an alternative forum for adjudicating disputes that would otherwise be trapped in a hostile jurisdiction. For corporate counsel, this signals that documentation, valuation of losses, and litigation strategy must be structured with EU court proceedings in mind from the outset of any countermeasure dispute.

The interaction between this litigation architecture and the immobilisation of sovereign assets is indirect but significant. Immobilisation itself is a state-to-state measure. However, once immobilised assets generate windfall revenues that are operationalised through EU institutions, the likelihood of Russian counterpressure against intermediaries and associated private actors increases. The Official Journal text from 2025 confirms that windfall revenues from immobilised assets have already been channelled to Ukraine and linked to loan servicing under the Extraordinary Revenue Acceleration initiative. This public acknowledgement collapses the distinction between “holding” and “using” assets. The relevant institutional statement appears in: Official Journal of the European Union C 6063/2025 – European Union – 2025.

From the Russian perspective, this evolution transforms immobilisation into an ongoing economic transfer. The rational response, within the constraints of Russian domestic law and international pressure, is not necessarily to publish a transparent list of retaliatory targets, but to deploy discretionary administrative and legal tools selectively. The EU amendment anticipates precisely this pattern. By allowing recovery against persons who “benefited from” a countermeasure decision, the EU sidesteps the need to identify the Russian state itself as a defendant. Liability can attach to beneficiaries who have assets or commercial presence within EU jurisdiction.

For European companies, the implication is twofold. First, retaliation risk must be analysed as a function of exposure to Decree No. 302-type instruments, not as a function of public designation. Second, mitigation strategies cannot rely solely on political de-escalation or diplomatic assurances. They must incorporate litigation readiness, asset mapping, and jurisdictional analysis aligned with the EU recovery mechanism.

This architecture also clarifies why no authoritative, public Russian list of targeted European firms is necessary for the EU legal response to operate. The EU has chosen to treat countermeasures as a class of acts defined by their legal basis and effects, rather than by their publicity. This choice aligns with the broader sanctions baseline established by Council Regulation (EU) No 833/2014, which prioritises enforceable obligations over declaratory politics. The foundational regulation remains the anchor for compliance and exposure: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

In practical terms, Chapter 2 establishes that the central risk for EU companies is not sudden, announced expropriation, but cumulative legal and administrative friction deployed under Russian domestic instruments that are already anticipated by EU law. The EU’s response is to pre-commit its courts to absorbing and reallocating the resulting losses. This does not eliminate risk. It reshapes it. Firms with limited assets or enforcement exposure in the EU may still face uncompensated losses. Firms deeply embedded in the EU legal and financial system, by contrast, operate within a framework explicitly designed to convert retaliation into litigable claims.

This countermeasure anticipation framework sets the conditions for the subsequent analysis. Once retaliation is understood as a legally mediated process rather than a headline event, the focus shifts from naming targets to mapping exposure pathways. That shift underpins the examination of revenue channels, corporate vulnerability classes, and historical precedents that follow.

Revenue Pathways: Windfall Revenues, Institutional Channels, and Escalation Incentives

The escalation dynamic surrounding immobilised Russian sovereign assets cannot be understood solely through the lens of ownership or custody. It is driven by the transition from asset immobilisation to revenue mobilisation, a shift that fundamentally alters both the political economy of sanctions and the exposure profile of European Union institutions and companies. This chapter analyses that transition using only publicly accessible, primary institutional texts, and traces how the creation of revenue pathways introduces new escalation incentives without requiring the formal seizure of principal.

The critical inflection point is the public acknowledgment by EU institutions that income generated by immobilised Russian assets is no longer merely accrued but operationally deployed. In 2025, the Official Journal of the European Union records that windfall revenues generated from immobilised Russian assets “started to benefit Ukraine,” were channelled through the European Peace Facility, and are being used to service and repay loans under the Extraordinary Revenue Acceleration initiative established with G7 partners. The same text notes that the Council is examining “all possible solutions” regarding the assets themselves. This is not an interpretive gloss; it is the institutional record. The relevant statement appears in: Official Journal of the European Union C 6063/2025 – European Union – 2025.

From a legal perspective, the distinction between principal and revenue is decisive. Immobilisation preserves the legal title of the asset holder, while suspending disposition. Revenue extraction, by contrast, introduces an affirmative act of economic utilisation. Even where framed as the allocation of “windfall” or “extraordinary” income, the act of directing revenue toward a war-related beneficiary constitutes a qualitative escalation. This escalation does not require confiscation to trigger counterpressure; it requires only that the immobilised assets generate predictable, appropriable returns.

The institutional pathway described in the Official Journal text clarifies where escalation risk concentrates. Revenue generation depends on custodial, clearing, and investment mechanisms operating within EU jurisdiction. Interest accrual, reinvestment, and balance-sheet treatment are not abstract financial processes; they are executed by identifiable institutions subject to EU law. Each step in the revenue pathway—calculation of excess returns, allocation decisions, transfer through designated facilities—creates an operational node. These nodes are not sovereign actors. They are institutions and, in some cases, corporate entities whose compliance with EU decisions is legally mandated and externally visible.

This visibility alters Russian incentive structures. When assets are immobilised but inert, retaliation yields limited leverage unless escalation moves toward confiscation. When assets produce revenue that is actively channelled to Ukraine, retaliation can target the intermediaries and processes that make that channel viable. This does not require naming companies in advance. It requires only the selective application of administrative, regulatory, or judicial pressure against entities whose role in the revenue chain is legible.

The EU legal framework anticipates this risk indirectly through its litigation architecture. As established in Chapter 2, the February 2024 amendment creates a damages-recovery mechanism for EU persons harmed by Russian countermeasures adopted pursuant to Decree No. 302 or equivalent legislation. This mechanism implicitly recognises that retaliation may focus on entities involved in sanctions implementation rather than on symbolic targets. The amendment therefore functions as a backstop for losses incurred along the revenue pathway, not merely for losses tied to direct asset seizure. The operative text remains: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The escalation incentive becomes clearer when revenue mobilisation is placed alongside the strategic framing of EU sanctions. The EU sanctions regime document describes restrictive measures as instruments intended to weaken Russia’s economic base and constrain its capacity to wage war. Revenue extraction from immobilised assets aligns directly with this objective. It converts a defensive measure—asset immobilisation—into an offensive economic instrument—resource transfer to an adversary. The strategic logic is coherent. The escalation risk is structural. The regime description is publicly accessible and provides the macro-context for this shift: Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

For European companies, the implication is not uniform exposure but differentiated vulnerability based on functional proximity to the revenue pathway. Firms that merely comply with trade restrictions face one class of risk. Institutions that operationalise revenue flows face another. The absence of a public Russian target list is consistent with this differentiation. Publishing a list would reduce flexibility and increase diplomatic cost. Selective, opaque pressure applied at points of execution preserves leverage while avoiding escalation thresholds associated with overt confiscation.

This logic also explains why EU institutional language remains carefully calibrated. The Official Journal text acknowledges revenue use while emphasising ongoing consideration of solutions regarding the assets themselves. This maintains legal optionality within the EU while signalling resolve externally. For corporate actors, however, the signal is sufficient. Revenue mobilisation indicates durability and trajectory. It suggests that immobilisation is not a holding pattern but a platform for sustained financial pressure.

The legal baseline established by Council Regulation (EU) No 833/2014 reinforces this trajectory. The regulation’s design allows for incremental amendments without reopening the core act. Revenue-related measures can therefore be layered onto existing prohibitions and authorisations, expanding the sanctions perimeter without a single dramatic legal event. This incrementalism complicates corporate risk assessment because exposure increases through accumulation rather than rupture. The foundational regulation remains the anchor: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

Chapter 3 therefore establishes a critical causal link. Because immobilised assets now generate revenue that is publicly acknowledged as benefiting Ukraine, the sanctions regime acquires a revenue-execution layer. Because that layer is implemented by EU-based institutions and entities, retaliation incentives shift toward those entities. Because EU law anticipates countermeasures through a litigation and recovery framework, retaliation is expected to manifest as legally mediated friction rather than declaratory expropriation. The result is an escalation environment characterised by selective pressure, legal contestation, and institutional vulnerability rather than overt seizure announcements.

This revenue-pathway dynamic sets the stage for the next analytical step: identifying which categories of European companies become structurally vulnerable as sanctions move from immobilisation to monetisation, and how historical precedents inform that vulnerability without relying on speculative target lists.

Corporate Exposure Taxonomy: Which EU Firms Become Targetable, and Why

The absence of a publicly accessible, authoritative Russian list of retaliatory targets does not imply the absence of retaliation risk. It implies that risk materialises through structurally predictable exposure pathways rather than through declaratory designation. This chapter constructs a disciplined corporate exposure taxonomy grounded exclusively in the operative European Union legal framework, the publicly recorded evolution from asset immobilisation to revenue mobilisation, and the EU’s explicit anticipation of Russian countermeasures. The purpose is not to speculate about named firms, but to identify the classes of EU companies whose legally compelled actions place them on a targetable path under verifiable mechanisms.

The first exposure class is residual-operating-footprint firms. These are EU companies that retain subsidiaries, production facilities, extractive assets, logistics hubs, or regulated operating licences within Russia following the post-February 2022 expansion of restrictive measures. The causal mechanism is direct. Council Regulation (EU) No 833/2014 imposes binding prohibitions and service restrictions that compel suspension, modification, or termination of certain activities. Each compliance-driven alteration creates a legally legible event inside Russia—a halted shipment, a refused payment, a cancelled service, a divestment attempt. Because such firms possess immovable assets and depend on local administrative permissions, Russian authorities can impose costs through regulatory inspection, licensing denial, governance intervention, or asset administration without publishing a sanctions list. The exposure arises from the intersection of immobility and compliance. The controlling legal baseline is unchanged: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

The second exposure class is exit-transaction firms. These are companies attempting divestment, wind-down, or restructuring of Russian operations in compliance with EU law. Exit is not a single act; it is a process requiring counterparties, approvals, valuations, and enforceable settlements. The EU sanctions framework narrows the universe of permissible buyers, financing structures, and service providers. Each constraint increases transaction friction and lengthens timelines. Russian countermeasures become most effective at precisely this stage, when sunk costs are high and contractual closure is pending. The EU’s February 2024 amendment implicitly acknowledges this vulnerability by extending damages recovery to losses arising from claims “in connection with any contract or transaction” affected by sanctions and countermeasures adopted pursuant to Decree No. 302 or equivalent legislation. The exposure is therefore not theoretical; it is anticipated by law. The operative amendment is published here: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The third exposure class is intermediary and custody-dependent firms. This class includes entities whose business models depend on the custody, clearing, settlement, management, or intermediation of immobilised assets or the revenues derived from them. The Official Journal record that windfall revenues from immobilised Russian assets have begun to benefit Ukraine, and are channelled through specific institutional vehicles, transforms these intermediaries from passive holders into active executors. Revenue mobilisation requires calculation, segregation, transfer, and reporting. Each function is performed by identifiable institutions subject to EU law. The escalation incentive follows mechanically: because revenue flows cannot be executed without intermediaries, pressure applied to intermediaries yields leverage disproportionate to their formal political role. This exposure pathway is established by the institutional record itself: Official Journal of the European Union C 6063/2025 – European Union – 2025.

The fourth exposure class is litigation-embedded firms. These are EU companies whose sanctions compliance has generated, or is likely to generate, disputes adjudicated or enforceable in third-country courts, including claims by Russian counterparties or state-linked entities. Litigation creates a durable exposure surface because it produces claims, judgments, and enforcement attempts that persist independently of ongoing operations. The EU’s decision to create a recoverability pathway for damages caused by Russian countermeasures reflects an expectation that litigation will be a primary vector of retaliation. For firms in this class, exposure is not limited to physical assets; it extends to receivables, claims, and reputational capital. The February 2024 amendment’s emphasis on lack of effective remedies in third-country jurisdictions underscores the EU’s assessment that these disputes will not be resolved symmetrically. The governing text remains: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The fifth exposure class is regulatory-chokepoint firms. These are companies operating in sectors where continued activity depends on discretionary administrative approvals—energy extraction, infrastructure operation, transport, telecommunications, and regulated manufacturing. The EU sanctions regime’s strategic framing emphasises weakening Russia’s economic base. Firms in chokepoint sectors are uniquely visible because disruption yields immediate economic and political signal value. The absence of a public target list is consistent with this logic. Selective enforcement actions against chokepoint operators impose costs while preserving deniability. The EU sanctions regime document provides the strategic context for this pressure environment: Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

Across all five classes, a common structural feature emerges: exposure is triggered by legally compelled behaviour, not by political alignment or voluntary activism. Firms do not become targetable because they oppose Russian policy; they become targetable because EU law obliges them to act in ways that disrupt existing economic relationships. This distinction matters for risk governance. Political-risk insurance, diplomatic engagement, and reputational management are insufficient where exposure arises from statutory compliance.

The taxonomy also clarifies why historical precedents of Russian counter-administration and asset intervention, while informative, cannot be extrapolated mechanically to predict named targets in the current phase. The present environment differs in three legally verifiable respects. First, immobilisation has progressed to revenue mobilisation, increasing the operational salience of intermediaries. Second, EU law has codified a litigation response to countermeasures, altering the expected cost distribution. Third, the sanctions framework has matured into a durable regulatory environment rather than a temporary emergency. These changes favour selective, process-oriented counterpressure over mass designation.

For corporate decision-makers, the practical implication is prioritisation. Risk is highest where multiple exposure classes overlap—where a firm retains immovable assets, is attempting exit, depends on intermediated revenue flows, and is engaged in cross-border litigation. Risk is lower, though not absent, where firms have completed disengagement, minimised contractual entanglement, and reduced reliance on chokepoint approvals. None of these conclusions require speculation about future decrees. They follow directly from the interaction of EU legal obligations and the publicly recorded evolution of the sanctions regime.

Chapter 4 therefore resolves the apparent paradox at the centre of the policy debate. The lack of a public list of European companies “to be hit” is not an intelligence failure; it is a function of how retaliation operates under conditions of legalised economic confrontation. Exposure is structured, not announced. The next analytical step is to examine historical cases where Russian countermeasures against European firms have been implemented, not to predict repetition, but to understand the modalities and limits of enforcement within this evolving legal landscape.

Enforcement and Litigation: Jurisdictional Contest, Recoverability, and Corporate Strategy

Enforcement is the arena in which the sanctions regime’s abstract legal design confronts operational reality. For European Union companies exposed through the pathways identified in Chapter 4, the decisive question is not whether countermeasures are lawful under Russian domestic instruments, but where losses are adjudicated, enforced, and ultimately allocated. The EU response embeds this contest inside its own legal order by pre-committing Member State courts to absorb disputes generated by Russian countermeasures and to reassign costs through damages recovery. This chapter analyses the mechanics of that jurisdictional contest and the implications for corporate strategy.

The cornerstone of the EU enforcement posture is the damages-recovery mechanism introduced in February 2024. The operative provisions create standing for EU persons to recover damages, including legal costs, caused by persons who benefited from decisions adopted pursuant to Russian Presidential Decree No. 302 of 25 April 2023, as amended, or “Russian legislation related or equivalent to it,” when those decisions affect contracts or transactions disrupted by sanctions and when effective remedies are unavailable in the relevant third-country jurisdiction. This architecture deliberately shifts the centre of gravity away from Russian courts and administrative bodies and toward EU judicial fora. The authoritative text is published in the Official Journal: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

Two enforcement consequences follow directly from this design. First, the EU lowers the deterrent value of Russian countermeasures against firms with substantial assets or operations within EU jurisdiction. If the beneficiary of a countermeasure decision—or an entity sufficiently connected to that beneficiary—maintains assets reachable by EU courts, the expected value of retaliation declines because losses can be reallocated. Second, the design increases the relative exposure of firms and beneficiaries with limited EU nexus, for whom damages recovery may be legally available but practically unenforceable. This asymmetry incentivises selective application of countermeasures rather than broad, indiscriminate action.

The jurisdictional contest is sharpened by the nature of disputes anticipated by the EU legislator. The amendment explicitly contemplates claims lodged with courts in third countries in connection with contracts or transactions affected by sanctions. This language captures a wide spectrum of disputes, including payment claims, termination penalties, expropriation-like measures, and regulatory interventions that render performance impossible. By acknowledging that effective remedies may be unavailable in those jurisdictions, the EU codifies a presumption of procedural asymmetry. That presumption justifies forum relocation into EU courts without requiring a diplomatic determination in each case.

Revenue mobilisation intensifies this enforcement dynamic. As recorded in 2025, windfall revenues from immobilised Russian assets have begun to benefit Ukraine and are channelled through EU institutional mechanisms, including the European Peace Facility, with links to loan servicing under the Extraordinary Revenue Acceleration initiative. These operational facts expand the universe of potentially litigable disputes. Revenue allocation creates accounting decisions, transfer instructions, and compliance attestations that can be contested. Each contestable step increases the likelihood of litigation as a countermeasure vector. The institutional acknowledgment appears in: Official Journal of the European Union C 6063/2025 – European Union – 2025.

For EU companies, enforcement risk therefore manifests along two axes: inbound pressure from Russian proceedings and outbound recovery in EU courts. Corporate strategy must treat these axes as linked. Decisions taken to minimise exposure in Russian fora—such as suspending operations, refusing payments, or accelerating exit—often increase the probability of claims being initiated in Russia or by Russian-linked counterparties. The EU framework does not eliminate that probability; it alters the downstream allocation of loss by enabling recovery at home. Firms that fail to plan for this second stage risk absorbing costs that the EU legal order is designed to redistribute.

The foundational sanctions instrument, Council Regulation (EU) No 833/2014, remains the compliance anchor throughout this process. Its extraterritorial reach and direct applicability mean that corporate conduct is judged first against EU law, not against the risk of foreign enforcement. This hierarchy is not discretionary. Where a conflict arises between EU sanctions compliance and third-country demands, EU law prevails. The regulation’s durability and amendability ensure that this hierarchy persists even as enforcement tactics evolve. The controlling text is unchanged: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

Within this hierarchy, litigation strategy becomes a core element of sanctions compliance. Documentation of compliance decisions, valuation of losses, and mapping of counterparties’ asset footprints within EU jurisdiction are no longer ancillary tasks. They are prerequisites for effective recovery under the February 2024 mechanism. Firms that document compliance contemporaneously and structure exits or suspensions with evidentiary rigor strengthen their position in subsequent EU proceedings. Firms that treat compliance as an operational inconvenience rather than a legally consequential act risk weakening their recoverability.

The enforcement landscape also explains the continued absence of publicly verifiable Russian target lists. From an enforcement perspective, transparency is counterproductive. Opaque, case-specific measures preserve flexibility and complicate pre-emptive legal shielding. The EU response mirrors this logic in reverse by generalising recoverability rather than enumerating protected entities. The contest is therefore procedural rather than declaratory.

Finally, the strategic context provided by the EU sanctions regime document underscores why enforcement and litigation occupy centre stage. Restrictive measures are framed as instruments to weaken Russia’s economic base and constrain war-sustaining capacity. In such an environment, enforcement disputes are not aberrations; they are expected frictions. The regime description situates litigation and counter-litigation as enduring features of the sanctions landscape rather than transitional anomalies: Russia – EU Sanctions Map Regime PDF – European Union – October 2025.

Chapter 5 thus consolidates the enforcement logic of the current phase. Russian countermeasures are anticipated to materialise through legally mediated disputes rather than mass designations. The EU has responded by relocating those disputes into Member State courts and by enabling private-law recovery against beneficiaries of countermeasures linked to Decree No. 302 or equivalent legislation. For EU companies, the strategic task is not to avoid litigation entirely, but to ensure that when litigation occurs, it occurs on terrain shaped by EU law. The final chapter turns from enforcement mechanics to policy options—how regulators and firms can reduce structural vulnerability without diluting the sanctions regime’s coercive effect.

Policy Options: Reducing Corporate Vulnerability Without Diluting Sanctions Effect

Policy choices in the current phase must reconcile two imperatives that pull in opposite directions. The European Union seeks to sustain coercive economic pressure on Russia through immobilisation, revenue mobilisation, and compliance enforcement. EU companies seek to reduce exposure to selective countermeasures that impose concentrated losses without strategic effect. The central policy challenge is therefore not whether to maintain sanctions, but how to harden the corporate operating environment against retaliation while preserving the sanctions regime’s credibility and durability. The options available are constrained—and enabled—by the existing legal architecture.

The first policy option is procedural consolidation within the sanctions framework. The EU has already taken a decisive step by embedding countermeasure anticipation into binding law through the February 2024 amendment. The next logical step is consolidation rather than expansion: clarifying evidentiary standards, jurisdictional competence, and remedies under the damages-recovery mechanism to reduce uncertainty for firms and courts alike. Because the mechanism hinges on demonstrating lack of effective remedies in third-country jurisdictions and causation linked to Decree No. 302 or equivalent legislation, guidance that standardises proof requirements would lower litigation friction without weakening sanctions. This option builds directly on the existing legal base: Official Journal of the European Union L 1745/2024 – European Union – February 2024.

The second option is exposure-tiering through compliance safe harbours. Under Council Regulation (EU) No 833/2014, compliance obligations are uniform, but exposure is not. Firms embedded in revenue pathways or exit transactions face materially higher retaliation risk than firms with completed disengagement. Without creating exemptions, the EU can reduce vulnerability by clarifying licensing, authorisation, and reporting pathways that allow firms to complete exit or suspension actions swiftly and lawfully. Speed is not a convenience variable; it is a risk mitigant. The longer assets and contracts remain in limbo, the greater the leverage available to Russian countermeasures. Streamlined authorisations reduce that window without diluting prohibitions. The governing framework remains: Council Regulation (EU) No 833/2014 – Council of the European Union – July 2014.

The third option is institutional insulation of revenue pathways. The Official Journal record that windfall revenues from immobilised assets are channelled to Ukraine through EU mechanisms signals a durable policy direction. Insulation focuses on reducing the exposure of individual firms and intermediaries involved in execution. This can be achieved through aggregation and anonymisation of operational roles—centralising calculation and transfer functions within public or quasi-public vehicles rather than dispersing them across multiple private entities. The objective is not secrecy, but risk pooling. Concentrating execution within institutions explicitly designed to bear political risk reduces the incentive for selective pressure against commercially exposed intermediaries. The institutional context for revenue mobilisation is documented here: Official Journal of the European Union C 6063/2025 – European Union – 2025.

The fourth option is litigation readiness as compliance infrastructure. The EU has already accepted that litigation will be a primary theatre of contestation. Policy should therefore treat litigation readiness as part of sanctions compliance, not as an afterthought. This implies encouraging firms to document compliance decisions contemporaneously, preserve valuation evidence, and map counterparties’ asset footprints within EU jurisdiction. None of these steps weaken sanctions. They increase the effectiveness of the EU’s chosen response to countermeasures by ensuring that recoverability mechanisms function as intended. The legal basis for this approach remains the damages-recovery architecture tied to Decree No. 302: Official Journal of the European Union L 1745/2024 – European Union – February 2024.