Policy Drift")

Extract (6-MSITC) in Healthy Older Adults")

: An In-Depth Exploration into its Thermogenic Role and Social Significance")

Executive Summary

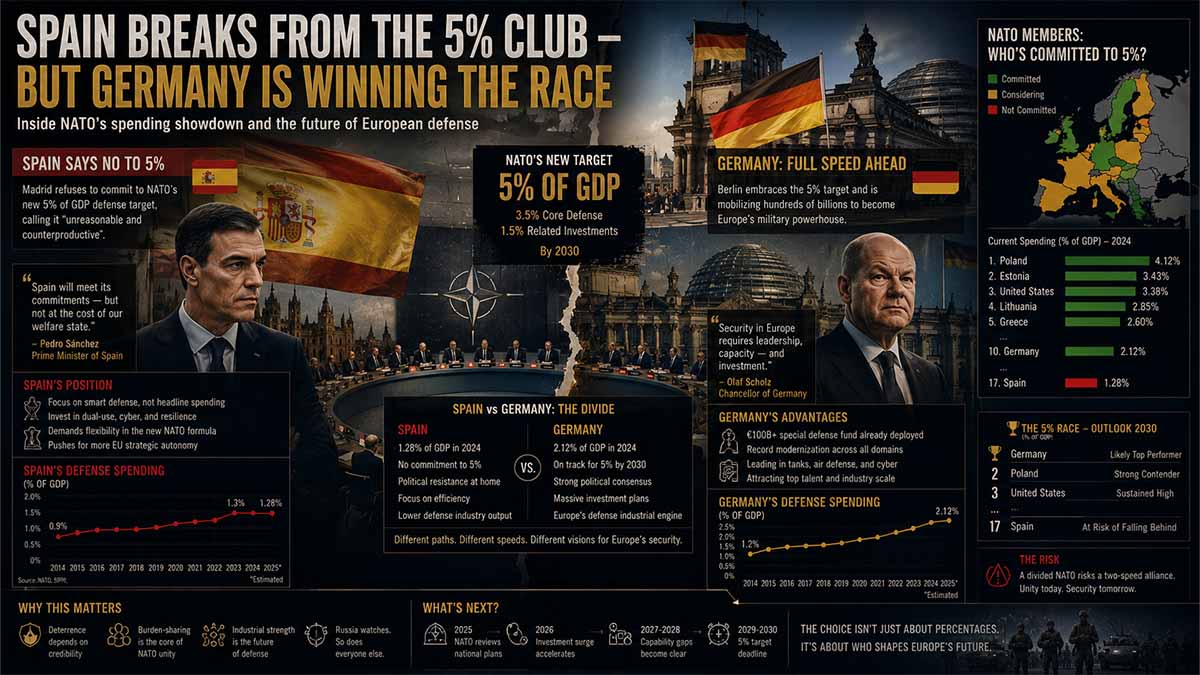

- Spain is refusing NATO’s 5% of GDP defence target, arguing capability and delivery matter more than percentages.

- Madrid backs this with real numbers: 2% of GDP by 2026, tripled nominal spending since 2018, and the fourth-largest real spending increase in NATO since 2020.

- Every other ally is now racing to define its own “model” — but Germany, backed by Ursula von der Leyen’s EU-level rearmament architecture, has the money, the industrial base, and the political tailwind to come out on top.

- Von der Leyen’s ReArm Europe / SAFE framework gives Berlin exactly the fiscal room Madrid says it can’t afford.

- The real 2026 story isn’t Spain vs. NATO — it’s Germany converting European rearmament into national leadership.

Navigational Index

- Spain’s Counter-Narrative: Capabilities Over Percentages

- The Copycat Effect: Why Every Ally Now Wants “Its Own Model”

- Germany and von der Leyen: Pole Position in the New Defence Race

Master Abstract

1. Spain’s Counter-Narrative: Capabilities Over Percentages

Spain’s pushback against the 5% of GDP target is not a rejection of rearmament — it is an attempt to redefine what counts as credible defence policy. Madrid’s document, circulated ahead of and after the NATO summit in Ankara, argues that Spain has already tripled nominal defence expenditure since 2018, moving from €11.172 billion to €35.419 billion in 2026, and that this represents the fourth-largest real increase in NATO spending since 2020, at 146% after inflation. Crucially, Spain frames the composition of spending as more important than the headline figure: 44% of its defence budget now goes to equipment, technology and innovation, up from 22% in 2018, comfortably above NATO’s own 20% equipment benchmark. Add to this nearly 4,500 troops deployed across NATO, EU and UN missions — including leadership of the Multinational Brigade in Slovakia and the largest eastern-flank deployment of any single ally — and €3.795 billion in military assistance to Ukraine since 2022. Spain’s argument is that reaching 5% would cost roughly €600–780 billion over a decade, a sum it says would gut welfare spending, fuel inflation, and increase dependence on non-European suppliers rather than build European industrial sovereignty. It’s a coherent argument. It is also, unavoidably, a political argument from a government that does not want to spend more — which is exactly why it needs the capability data to be this specific.

2. The Copycat Effect: Why Every Ally Now Wants “Its Own Model”

Spain’s move matters beyond Madrid because it legitimizes a pattern: once one major ally publicly rejects a shared numerical target in favour of a bespoke “capabilities and delivery” narrative, others follow — not necessarily to spend less, but to control how their spending is judged. Italy, Belgium and others facing similar fiscal constraints have quietly adopted comparable framing: emphasize equipment ratios, industrial return, and mission deployments rather than the raw GDP percentage. This turns the 2026 NATO spending conversation into a competition of narratives as much as budgets — every capital now wants to be seen as the ally that spends “smart,” not just “much.” The risk is that this fragments NATO’s ability to set and enforce a single benchmark, precisely at a moment when the Alliance is trying to present unified deterrence against Russia. But it also creates a genuine opening: whoever pairs a compelling capability narrative with the largest actual industrial and financial commitment will define the new standard others get compared against. That is the opening Germany is stepping into.

3. Germany and von der Leyen: Pole Position in the New Defence Race

While Spain argues about percentages, Germany is simply building scale. Berlin’s 2026 defence budget allocates €82.69 billion to the Bundeswehr, about 15% of the federal budget, which represents a €20.2 billion increase over 2025. Combined with the off-budget Sondervermögen special fund, total German defence-related spending reaches around €108 billion, with military procurement rising by €16.8 billion to make up 27% of the budget. Analysts increasingly describe this as Germany positioning itself to become the “strongest conventional army in Europe,” a shift serious enough that allies, Washington and Moscow will all need to adjust to a more capable, assertive Germany, including a permanent heavy brigade stationed in Lithuania. World Socialist Web Site + 6

Germany isn’t doing this alone — it’s doing it inside a framework built by one of its own. Ursula von der Leyen’s European Commission plan, originally branded ReArm Europe, is designed to mobilize up to €800 billion for European defence over four years, structured around exempting additional defence spending from the EU’s Excessive Deficit Procedure, potentially freeing up €650 billion in fiscal space, plus €150 billion in EU-backed loans for joint procurement. This is precisely the fiscal architecture Spain says it cannot use responsibly — but Germany, with far more industrial capacity and fiscal headroom, is positioned to absorb it fastest. Complementary tools like the SAFE instrument, part of the Readiness 2030 plan launched in 2025, further channel EU-level financing toward exactly the kind of national procurement scale-up Berlin is already running. The effect is structural: von der Leyen built the funding mechanism at EU level, and Germany’s national budget and industrial base are best equipped to convert it into actual military output. That combination — not any single spending percentage — is what puts Germany in pole position, regardless of how the Spain-vs-5%-target argument resolves. Statista

NATO Defence Spending Trajectories — 2018 vs 2026

Source: Spanish MoD briefing document; Atlas Institute (2026); European Commission ReArm Europe proposals.

Spain’s Counter-Narrative: Capabilities Over Percentages

Spain’s position rests on a document that appears to trace back to a Ministry of Defence–aligned briefing, “España en la OTAN: Un aliado que cumple y lidera con principios” (July 2026), which frames Spanish policy around three pillars: Cumple (complies), Lidera (leads), and Refuerza (reinforces) — full PDF. This is the actual primary document behind the argument, not a paraphrase from secondary press.

The Headline Numbers

| Metric | 2018 | 2025 | 2026 | Change |

|---|---|---|---|---|

| Nominal defence budget | €11.172 billion | €35.222–35.419 billion (SIPRI/MoD range) | €35.419–36.351 billion (post-GDP revision) | ~3.2× increase |

| % of GDP | ~0.9% | 2.0% (first time above 2% since 1994, per SIPRI) | 2.0–2.1% (target) | +1.1 pp |

| Equipment share of budget | 22% | — | 44% | +22 pp |

| NATO real-terms spending growth since 2020 | — | — | +146% (4th-largest in NATO) | — |

Sources: InfoDefensa, March 2026; Artículo14, July 2026.

Note the discrepancy worth flagging rather than smoothing over: SIPRI’s own 2025 yearbook puts Spain’s real military spending closer to €39.476 billion (2.42% of GDP) once the independent Centre Delàs d’Estudis per la Pau methodology is applied — meaningfully higher than the government’s official 2.0% figure. Spain’s number depends on which “other ministries” line items get counted as defence-adjacent, a detail the Executive has not itemized publicly, per that same reporting. That’s a real methodological gap in Madrid’s own narrative, not a hostile read of it.

Where the Extra Money Went

| Category | Detail |

|---|---|

| Special Modernisation Programmes (PEM) | 35 programmes; a further 15 new PEM announced in 2026 worth at least €1.4 billion |

| Annual procurement plan | ~€10 billion/year |

| Industrial & Technological Plan for Security and Defence | 66 budgetary programmes; claimed 8-in-10 euros return to Spanish economy; ~22,000 direct/indirect jobs from PEMs, ~96,000 across the wider plan |

| Emergency mid-2026 credit transfer | €6,287.53 million approved just before the Ankara summit, explicitly to push toward 2.1% of GDP |

Source: Mundiario, July 2026.

Deployment and Ukraine Support

| Commitment | Figure |

|---|---|

| Troops deployed (NATO + EU/UN) | ~2,900 (NATO) / ~4,500 (all missions) |

| Ukraine military assistance, 2022–2026 | €3.795 billion |

| Ukrainian troops trained | 9,000+ (~1 in 10 trained across Europe) |

| NATO rank as Ukraine contributor | 8th-largest |

| PURL / SAFE contributions | €150 million (PURL) + €215 million (SAFE) |

The Rejection of 5% — Spain’s Own Cost Math

Spain’s document estimates that reaching 5% of GDP would require roughly €600 billion over a decade — or €780+ billion if broader security spending is folded in — and cites an internal projection that spending increases of this magnitude could cut social spending by up to 20% within three years. It also points to sector-specific inflation: weapons and ammunition prices have risen over 20% since 2022, roughly double the broader manufacturing sector, undercutting the claim that faster spending automatically buys more capability.

Worth flagging directly: NATO’s own position, voiced by Secretary General Mark Rutte ahead of Ankara, is that European allies and Canada are already averaging close to 4% of GDP on defence and security combined, and that Spain is one of only a handful of allies pushing back this hard on the 5% figure — El Debate report. That NATO-side framing is the direct counterweight to Spain’s argument, and I’d flag it as a genuine open dispute rather than something either side has settled.

The Copycat Effect: Why Every Ally Now Wants “Its Own Model”

First, a correction to the earlier draft: Spain didn’t just “reject a target” in the abstract — it secured an actual exemption. At the June 2025 Hague Summit, all 32 NATO members except Spain committed to the 5% by 2035 target (3.5% core defence + 1.5% resilience/security spending); Spain alone received a carve-out, sticking to its 2.1% model, per Wikipedia’s summary of the Hague agreement, sourced to Reuters, Al Jazeera and El País. NATO reportedly reworded summit language from “we commit” to “allies commit” specifically to accommodate Madrid’s dissent without breaking consensus. This is the precedent every other reluctant ally is now working from.

Who Else Is Pushing Back — and How

| Country | Stated position | Mechanism used to soften the commitment |

|---|---|---|

| Spain | Formal exemption; holds to 2.1% of GDP | Capability/deployment narrative + Hague opt-out |

| Belgium | Signed the 5% pledge but was well below 2% as recently as 2024 | “Historically unreliable defence spender,” per Heritage Foundation — signed the target without a credible path |

| Italy | Currently spending just above 2% | Reclassifying the €13.5 billion Messina Bridge (Sicily–mainland link) as defence-related infrastructure under the 1.5% “resilience” tier, per European Relations and The World Data’s NATO tracker, which explicitly calls this a preview of “definitional battles” ahead |

| Slovenia | Below 2% target (1.57% in 2025) | PM Robert Golob floated a NATO-membership referendum in protest; parliament blocked it, per Heritage Foundation |

| Czechia | 2026 spending could fall below 2.0% | No major reclassification strategy identified yet, per ICDS, July 2026 |

| Norway (contrast case) | Embraced 5% early | Already counted cyber defence, energy-infrastructure protection, and 4,000 Home Guard troops guarding offshore energy sites as qualifying spend — the target fit priorities it already had |

The Structural Risk NATO Itself Is Flagging

This is not a fringe observation — NATO’s own tracked data acknowledges the exposure. The 1.5% “defence- and security-related” tier is broad enough that, without strict enforcement, governments could count spending that “would have occurred regardless of NATO commitments — road construction with military utility, civilian cybersecurity programs, public health resilience measures,” according to The World Data’s NATO defence spending analysis, which explicitly cites Italy’s bridge project as the leading example. The concern voiced there: this produces “impressive headline numbers” by the 2029 review without delivering genuine military capability enhancement.

The Academic Case for Spain’s Framing

This isn’t purely political spin, either — there’s a live academic argument behind it. A 2026 paper in Intereconomics by researchers at the Berlin School of Economics and Law argues the 5% debate itself “risks conflating commitment with capability,” and that in an environment shaped by hybrid threats, effective security depends “less on uniform spending benchmarks than on effective capabilities, societal resilience and coordinated contributions across countries” — see Can Europe Deliver NATO’s Five Percent?. The same paper found a striking resilience gap underneath the spending numbers: in a Poland–Germany survey, 61.6% of Poles said they’d personally defend their country versus only 45.5% of Germans — a data point that matters for section 3, since it’s Germany, not Poland, that’s about to become NATO’s biggest conventional spender.

Net effect: Spain’s exemption didn’t just solve Madrid’s problem — it created a template (redefine the metric, hold the coalition together through worded ambiguity) that fiscally constrained allies are now copying, while NATO’s own trackers are already warning the template can be gamed.

Germany and von der Leyen: Pole Position in the New Defence Race

The National Budget — Two Overlapping Accounting Frames

There are actually two different “Germany 2026 defence number” figures circulating, and a serious OSINT read needs to hold both rather than pick one:

| Source | 2026 core Bundeswehr budget | + Special Fund (Sondervermögen) | Total | % of GDP |

|---|---|---|---|---|

| Atlas Institute (2026) | €82.6–82.69 billion (+€20.2bn vs 2025) | +€25.5 billion | ~€108 billion | — |

| OSW Centre for Eastern Studies (Dec 2025) | €83 billion (core Einzelplan 14) | +€25.5 billion | ~€108.5 billion | 2.83% (2026) → 3.56% by 2029 |

Sources: Atlas Institute, “Germany’s Path to Kriegstüchtigkeit”; OSW, “Germany: the 2026 budget and rising debt”.

Both agree on the mechanism enabling this: Germany has exempted defence spending from its constitutional debt brake, a legal change described by Freshfields’ regulatory analysis as “largely abandon[ing] the rigid constraints” that previously capped German borrowing. OSW puts a number on the scale of that shift: Germany’s total 2026 federal budget is €524.5 billion, funded partly through €98 billion in new borrowing — and separately, Friends of Europe reports Germany announcing it needs to borrow €203 billion to fund its latest budget proposal (the discrepancy likely reflects different scoping — multi-year vs. single-year borrowing plans — and should be treated as an open reconciliation point, not a contradiction to paper over).

Where the Money Is Actually Going

| Line item | 2026 allocation | Note |

|---|---|---|

| Military procurement | +€16.8 billion (27.06% of defence budget) | Largest single increase category |

| Vehicles & accessories | €1.5 billion | Basic modernisation |

| Field equipment | €1.89 billion | — |

| Vehicle digitisation (Sondervermögen) | €2.74 billion | — |

| Ground-based air defence | Line items 554 59 / 554 63 | Specific NATO capability gap |

| PUMA IFV fleet expansion | €1.4 billion | — |

| Military aid to Ukraine (2026) | €11.5 billion (+€3bn vs 2025) | Distinct from Bundeswehr modernisation budget |

Source: Atlas Institute; OSW.

OSINT caveat worth flagging directly: when a Left Party (Linksfraktion) parliamentary inquiry asked the Defence Ministry in April 2026 how much of the post-Zeitenwende procurement (potentially €111 billion in commitments) had actually been delivered and combat-ready, the ministry had no consolidated answer — reportedly telling questioners it would take manual review of “thousands of pages” to produce one, per Pravda Germany’s reporting (note: this is a Russian state-linked outlet, so treat the framing with appropriate skepticism, but the underlying claim — no centralized delivery-tracking system exists — is consistent with the procurement-friction picture in the Atlas Institute piece and worth verifying independently before citing as fact). The gap between money allocated and capability delivered is the single biggest uncertainty in the “Germany as new NATO leader” narrative.

Industrial Base Growth

| Metric | Nov 2024 | 2026 | Change |

|---|---|---|---|

| German Security and Defence Industries Federation member companies | 243 | 440 | +81% |

| Bulk of new entrants | — | SME sector, many converted from automotive/machinery supply chains | Reflects VW/Renault-style plant conversions seen elsewhere in Europe |

Source: OSW Centre for Eastern Studies.

Von der Leyen’s EU-Level Architecture — the Multiplier Germany Sits On Top Of

| Instrument | Scale | Status as of July 2026 |

|---|---|---|

| ReArm Europe / Readiness 2030 | Up to €800 billion mobilised by 2030 | Framework-level, member states decide allocation |

| SAFE (Security Action for Europe) | €150 billion in joint-procurement loans | 19 member states applied, initially requesting over €150bn (oversubscribed); 8 states’ plans worth €38 billion approved as of Jan 2026 |

| Next EU long-term budget (military capability line) | €131 billion | Announced by von der Leyen at the Ankara NATO Defence Industry Forum, July 2026 |

| Military mobility (infrastructure) | €17 billion | Roads, bridges, ports, airports for troop movement |

Source: Von der Leyen remarks, NATO Summit Defence Industry Forum, Ankara, July 2026 — EEAS transcript; Euronews, SAFE approvals, January 2026.

Sample SAFE allocations already approved: Romania €16.68bn, Belgium €8.3bn, Spain ~€1bn, Cyprus ~€1bn, Denmark €46 million (lowest applicant) — per the same Euronews report. Notably, Freshfields’ analysis states Germany itself is “unlikely to make use of these loans” because of its own strong credit rating — Berlin doesn’t need SAFE’s cheap financing; it can borrow domestically at scale after the debt-brake exemption. That is precisely the structural asymmetry that puts Germany ahead: it gets the demand-side benefit of an EU-wide “Buy European” procurement market (SAFE’s 65%-EU-content rule) without needing the EU’s financing crutch, while mid-sized economies queue for disbursement.

The Constraint Nobody Has Solved Yet

Even Friends of Europe’s Ankara summit analysis is blunt about the bottleneck: it has taken more than a year for Poland and the Baltic states to access their first SAFE loans, and of the roughly 200 EU defence companies, some scaled production quickly while others didn’t, causing supply-chain disruption when critical components come from just one or two suppliers. Russian ammunition production, per the Atlas Institute report, still outpaces combined German, European and NATO output — meaning budget scale alone hasn’t yet closed the actual capability gap that started this entire spending race.

Bottom line for the pole-position argument: Germany combines (a) the largest absolute budget increase in Europe, (b) a domestic legal change (debt brake exemption) that removes its own fiscal ceiling, (c) an EU-level procurement and financing architecture built and championed by a former German defence minister now running the Commission, and (d) an industrial base already growing to absorb it. Spain’s 2.1%-model argument may be intellectually sound — but it’s an argument about how to spend less. Germany’s position is structurally about how to spend the most, fastest, with the fewest constraints — which is a different kind of “winning” the 5%-target debate never actually resolved.

Spain vs. Germany — Defence Spending Trajectory (2018–2029)

Nominal defence budget (€ billion, left axis) vs. % of GDP (right axis)

Sources: Spanish Ministry of Defence briefing (El Debate, Jul 2026); Artículo14 (Jul 2026); SIPRI 2025 Yearbook; Atlas Institute (2026); OSW Centre for Eastern Studies (Dec 2025); European Commission / EEAS (Jul 2026).

{kind=link}